/Chipset%20held%20over%20rush%20hour%20traffic%20by%20Jae%20Young%20Ju%20via%20iStock.jpg)

Navitas Semiconductor (NVTS) shares ripped higher on April 21 amid heightened retail enthusiasm for artificial intelligence (AI) infrastructure.

As the rally forced short sellers to cover their positions, NVTS saw its relative strength index (RSI) climb into the early 80s, indicating potential for a near-term breather.

Versus the start of this month, Navitas Semiconductor stock is now up nearly 100%.

It’s Hard to Justify NVTS Shares’ Premium Multiple

While the AI narrative is compelling, the bear case for NVTS shares rests on a massive disconnect between the company’s market cap and its financials.

In 2025, the Nasdaq-listed firm saw its revenue decline by an alarming 45% year-over-year.

And while management pointed to a sales bottom in Q4, Navitas Semiconductor remains deeply unprofitable with a negative net margin exceeding 200%.

The AI infrastructure stock is unattractive because you pay a premium for “AI design wins” that executives admit are unlikely to materially affect P&L this year.

Trading at nearly 62x sales, NVTS has priced in a flawless multi-year execution, leaving no room for cyclical downturns or integration delays common in the semiconductor sector.

Insiders Have Been Unloading Navitas Semiconductor Stock

Investors are not advised to chase the momentum in Navitas Semiconductor shares due to the intense competition and execution risks inherent in gallium nitride (GaN) and silicon carbide (SiC) markets.

NVTS faces looming threats from much larger, better-capitalized incumbents, ON Semiconductor (ON) and Infineon (IFNNY) — both of which are aggressively defending their data center territories.

Moreover, the recent departure of its CFO and significant insider selling (worth nearly $5 million in the last 90 days) indicate that those closest to the business are choosing to de-risk at the current price.

In short, for bears, the ongoing rally isn’t a fundamental shift, but a retail-driven squeeze that ignores a high cash burn rate of $11 million per quarter.

What’s the Consensus Rating on Navitas Semiconductor?

Wall Street analysts also remain cautious on Navitas Semiconductor, especially since it doesn’t currently pay a dividend to offset some of the aforementioned risks.

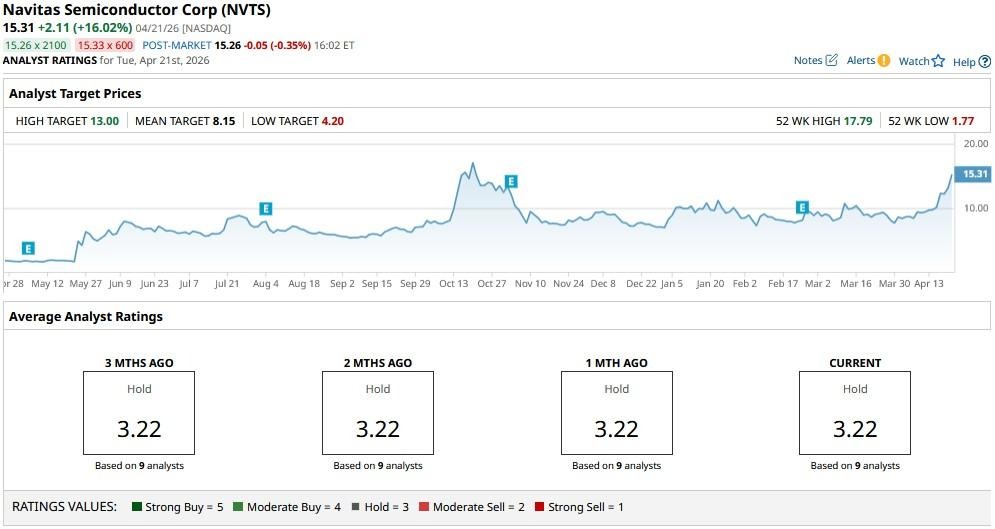

The consensus rating on NVTS stock sits at a “Hold” only, with the mean price target of just over $8 indicating potential downside of more than 45% from here.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Arista%20sing%20at%20headquarters%20of%20an%20American%20multinational%20technology%20company%20Arista%20Networks%20-%20Santa%20Clara%2C%20California%2C%20USA%20-%202020%20By%20MichaelVi.jpeg)

/AI%20(artificial%20intelligence)/AI%20Data%20Center%20by%20Gorodenkoff%20via%20Shutterstock.jpg)