/Trane%20Technologies%20plc%20logo%20and%20price%20data-by%20Piotr%20Swat%20via%20Shutterstock.jpg)

Valued at a market cap of $92.7 billion, Trane Technologies plc (TT) is a climate-innovation and industrial manufacturing company that designs, builds, and services energy-efficient Heating, Ventilation, Air-Conditioning (HVAC) systems and transport-refrigeration solutions. The Swords, Ireland-based company, focuses on sustainable, low-carbon technologies for buildings, homes, and cold-chain logistics, aiming to reduce customer emissions.

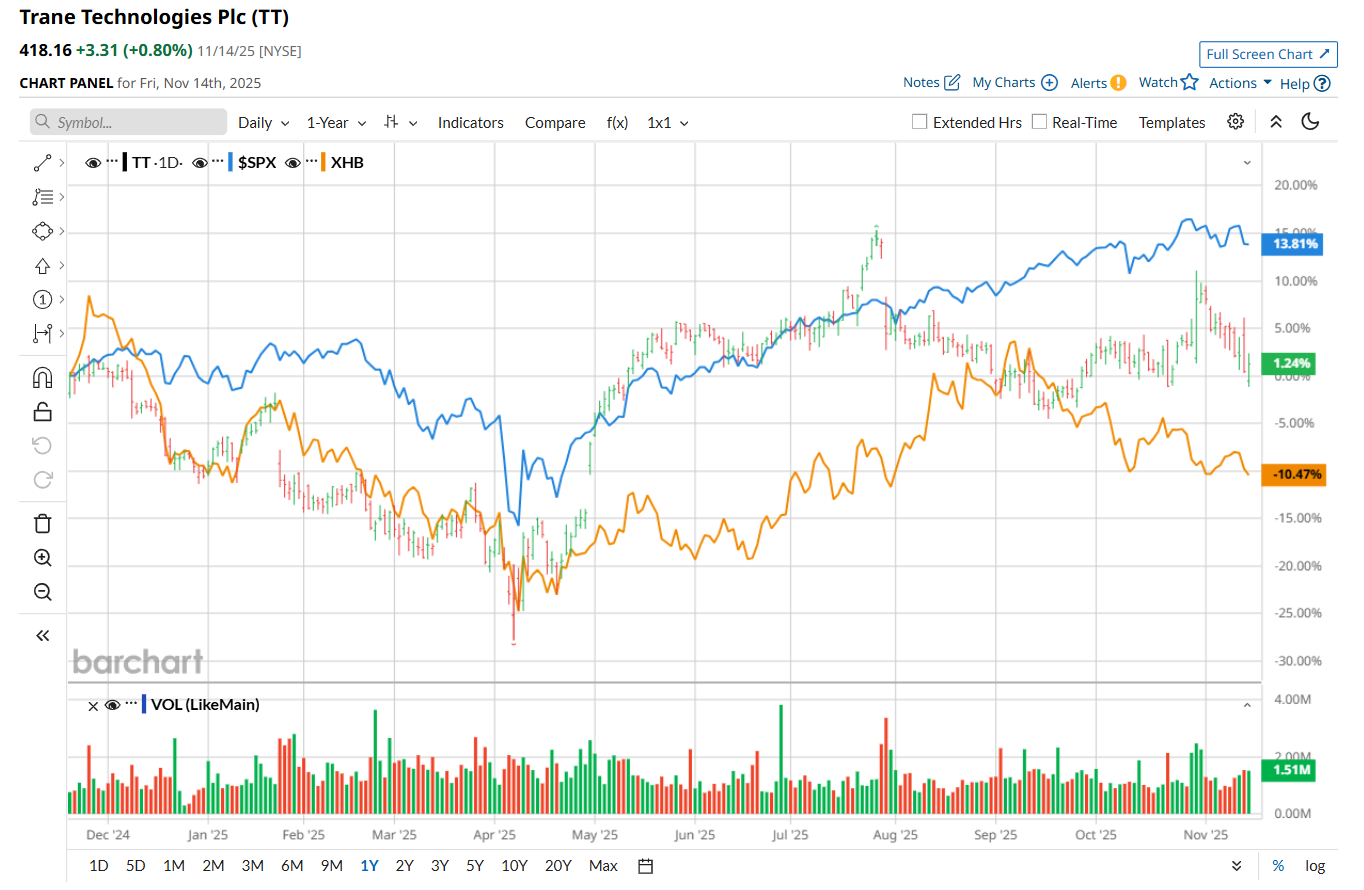

Shares of this industrial manufacturing company have lagged behind the broader market over the past 52 weeks. TT has gained 2% over this time frame, while the broader S&P 500 Index ($SPX) has soared 13.2%. Moreover, on a YTD basis, the stock is up 13.2%, compared to SPX’s 14.5% return.

However, zooming in further, TT has outperformed the SPDR S&P Homebuilders ETF (XHB), which has declined 11.5% over the past 52 weeks and 1.1% on a YTD basis.

On Oct. 30, shares of TT surged 4.4% after delivering its mixed Q3 earnings results. While the company's net revenue improved 5.6% year-over-year to $5.7 billion, it missed consensus estimates by a slight margin. Nonetheless, profitability remained strong, with its adjusted operating margin improving by a notable 170 basis points from the year-ago quarter and adjusted EPS of $3.88 climbing 15.1% and coming in 2.6% ahead of analyst expectations. Moreover, TT achieved all-time-high quarterly bookings of $6 billion, up 14.7% annually, driven by robust demand in its commercial HVAC segment, further bolstering investor confidence.

For the current fiscal year, ending in December, analysts expect TT’s EPS to grow 16% year over year to $13.02. The company’s earnings surprise history is promising. It exceeded the consensus estimates in each of the last four quarters.

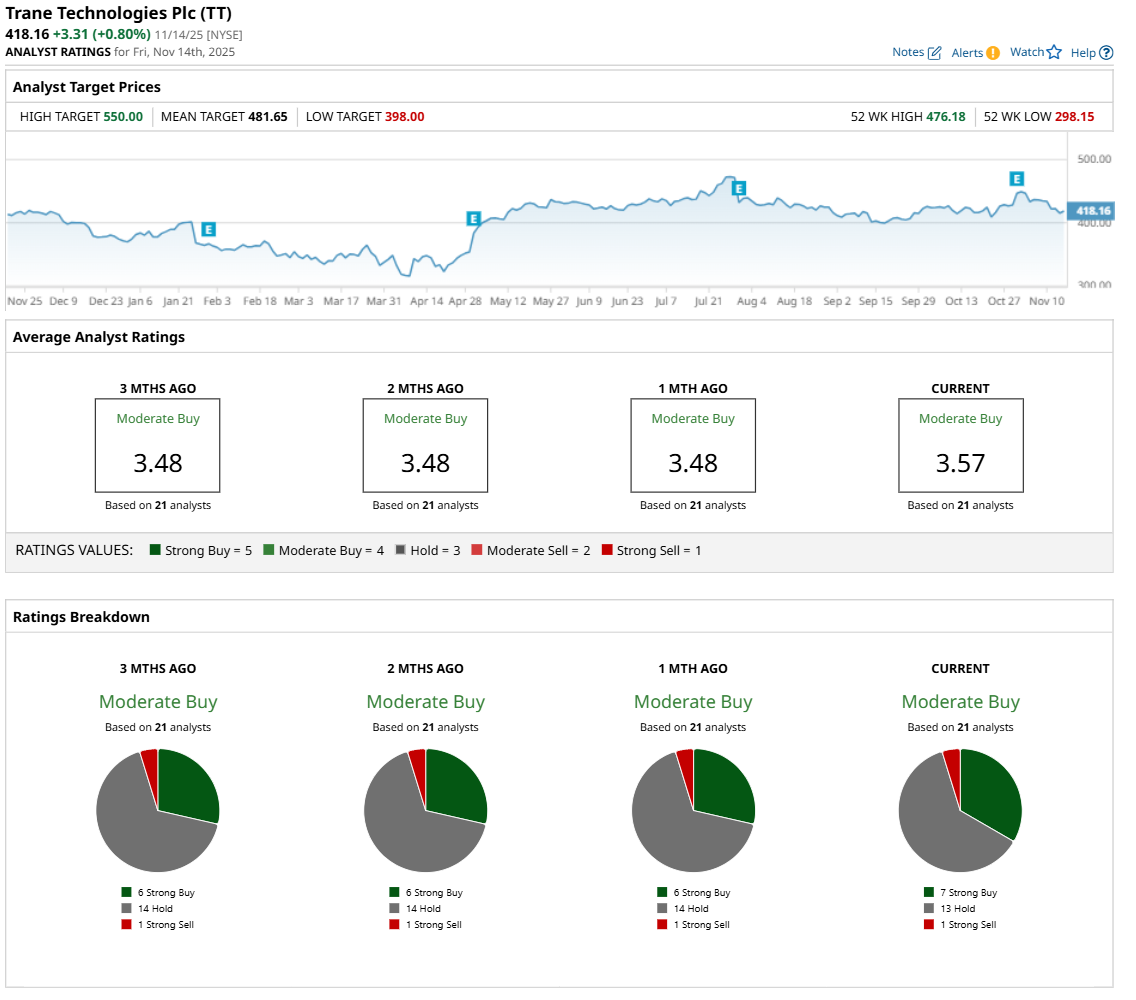

Among the 21 analysts covering the stock, the consensus rating is a "Moderate Buy,” which is based on seven “Strong Buy,” 13 "Hold,” and one "Strong Sell” rating.

This configuration is slightly more bullish than a month ago, with six analysts suggesting a “Strong Buy” rating.

On Nov. 13, Bank of America Corporation (BAC) analyst Andrew Obin upgraded TT to “Buy” and raised its price target to $550, the Street-high price target, indicating a 31.5% potential upside from the current levels.

The mean price target of $481.65 represents a 15.2% premium from TT’s current price levels.

On the date of publication, Neharika Jain did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Space/Planet%20earth%20with%20flying%20rocket%20by%20Sergey%20Mironov%20via%20Shutterstock.jpg)

/Robinhood%20app%20on%20phone%20by%20Andrew%20Neel%20via%20Unsplash.jpg)

/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)