With a market cap of $16.4 billion, Essex Property Trust, Inc. (ESS) is a fully integrated REIT focused on acquiring, developing, redeveloping, and managing multifamily residential properties across select West Coast markets. The company holds ownership interests in 257 apartment communities totaling over 62,000 homes, with an additional property currently under active development.

Shares of the San Mateo, California-based company have underperformed the broader market over the past 52 weeks. ESS stock has decreased 12.9% over this time frame, while the broader S&P 500 Index ($SPX) has rallied 12.6%. Moreover, shares of the company are down 2% on a YTD basis, compared to SPX’s marginal gain.

Focusing more closely, shares of the REIT have lagged behind the State Street Real Estate Select Sector SPDR ETF’s (XLRE) 1.9% return over the past 52 weeks.

Essex Property Trust reported Q4 2025 results on Feb. 4 and issued 2026 guidance calling for 2.4% same-property revenue growth, driven by 2.5% blended lease rate growth, 85 basis points of earn-in from 2025, and expense growth slowing to 3%, the lowest level in several years. The outlook was further supported by expectations for cap rate compression in Northern California, where Essex has been the largest investor over the past two years amid a 20% projected decline in new housing supply. However, the stock fell marginally the next day.

For the fiscal year ending in December 2026, analysts expect Essex Property Trust’s core FFO to grow marginally year-over-year to $15.99 per share. The company’s earnings surprise history is mixed. It beat the consensus estimates in three of the last four quarters while missing on another occasion.

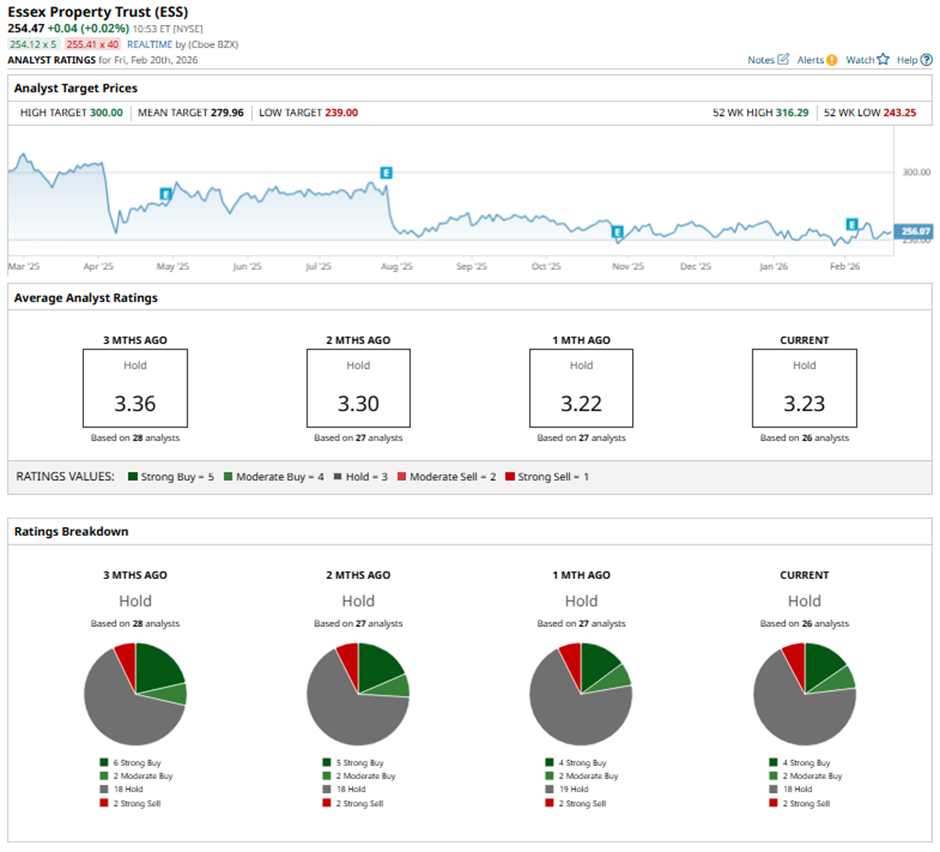

Among the 26 analysts covering the stock, the consensus rating is a “Hold.” That’s based on four “Strong Buy” ratings, two “Moderate Buys,” 18 “Holds,” and two “Strong Sells.”

On Feb. 11, UBS analyst Michael Goldsmith maintained a “Hold” rating on Essex Property Trust with a price target of $274.

The mean price target of $279.96 represents a premium of 10% to ESS’s current levels. The Street-high price target of $300 implies a potential upside of 17.9% from the current price.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.