/2d%20illustration%20of%20Cloud%20computing%20by%20Blackboard%20via%20Shutterstock.jpg)

Prominent neocloud company Nebius (NBIS) has inked a billion-dollar agreement with Reflection AI to provide AI compute through 2029. Under the terms of the deal, Reflection AI will gain access to Nebius's capacity of Nvidia's (NVDA) GB300 chips. Although not the latest generation of Nvidia chips (that distinction belongs to the Rubin GPU), the GB300 is a high-performance system built on Blackwell Ultra GPU technology.

The deal would represent annual revenues of about $290 million throughout its tenure if spread evenly. Notably, this would be close to 55% of the company's total revenues in 2025.

About Nebius

Founded in 2024 but tracing its origins to Yandex, one of Europe's largest technology companies, Nebius describes itself as a full-stack AI cloud company whose platform covers the AI journey from data and model training through production deployment. The company provides GPU-powered cloud infrastructure specifically built for artificial intelligence workloads and competes broadly with AI-focused cloud providers such as CoreWeave (CRWV).

Valued at a market cap of $53.3 billion, NBIS stock has been on a roll this year, gaining 136% on a year-to-date (YTD) basis.

But can Nebius sustain its run, or will it stumble? Let's find out.

Full-Stack Ability & Capital Intensity: The Dichotomy of Owning Nebius

Nebius has got some serious backers, whether through partnerships or in its ownership pattern.

Nvidia, its only GPU supplier, holds a stake of 8.3% in the company after it invested $2 billion. Further, multi-billion dollar agreements with Microsoft (MSFT) and Meta (META) point towards the fact that AI compute capacity remains constrained, and Nebius is a capable partner of choice for these hyperscalers to aid in that fulfilment.

Nebius AI Cloud is a key component of this trust, and the deeper edge is the relationship with Nvidia. In March 2026, Nvidia invested $2 billion in Nebius and granted it early access to the Rubin platform, Vera CPUs, and BlueField storage, plus fleet health monitoring. That means Nebius often runs the newest silicon before competitors, and its clusters stay healthier at scale.

However, Nebius AI Cloud is powered by a physical infrastructure that the company designs and operates itself, including gigawatt-scale AI factories in the United States and a plan to deploy more than 5 gigawatts of Nvidia systems by the end of 2030. Owning the data center layer is what separates a real neocloud from a reseller who simply leases capacity and marks it up.

On top of the raw compute sits a proper developer platform with built-in MLOps tooling, managed Kubernetes, and serverless inference, so teams can move from data to model training to production without stitching together outside tools. The clearest proof of the full-stack ambition is Nebius Token Factory, launched in November 2025 as the next evolution of the old AI Studio. It handles inference, post-training, and model lifecycle management, promising sub-second inference, 99.9% uptime, and autoscaling for production workloads.

Finally, beyond the cloud itself, Nebius carries adjacent businesses that widen the moat. TripleTen is an education arm that trains engineers, growing revenue to about $11.6 million in the first quarter of 2026. Avride builds autonomous vehicles and delivery robots and secured up to $375 million backed by Uber (UBER) and Nebius in October 2025. Additionally, Nebius made a significant move into the AI inference market through its recent acquisition of Eigen AI. As the focus in the industry shifts from model training toward increased inference activity, possessing dedicated capabilities in this area will prove vital for sustaining long-term competitive advantage and growth.

Having said that, the GPU rental operation demands substantial capital investment. NBIS has recently secured billions of dollars in debt financing and maintains a $25 billion at the market equity program. These large-scale infrastructure expansions require considerable upfront spending before associated contracts begin generating meaningful revenue, often several quarters down the line.

In addition, any setbacks in data center development timelines could delay the realization of income and complicate efforts to secure new business agreements. Meta’s potential move into offering compute resources also represents a possible competitive challenge for the company going forward.

Revenues Jump, Touches Profitability

Some would say that Nebius's Q1 numbers exceeded expectations. Revenues grew almost eightfold, and the company moved into the black.

Revenues for the quarter came in at $399 million, a considerable rise from the previous year's $50.9 million. Further, the company reported earnings of $2.11 per share compared to a loss of $0.44 per share in the year-ago period, exceeding the Street estimates of a loss of $0.71 per share.

Cash flow from operations also turned positive to $2.3 billion, which was an outflow of $184.1 million in the prior year. Overall, the company closed the quarter with a cash balance of $3.7 billion, much higher than its short-term debt levels of $24.5 million. However, the cash balance was much lower than the company's reported capex guidance for 2026, which was increased to $20 billion-$25 billion from the prior $16 billion-$20 billion.

Valuation metrics are portraying mixed signals. While the forward P/S at 14.64 is above the sector median of 3.31 by a wide margin, the P/CF of 8.77 is lower than the sector median of 19.20 by over 50%.

Analyst Opinion on NBIS Stock

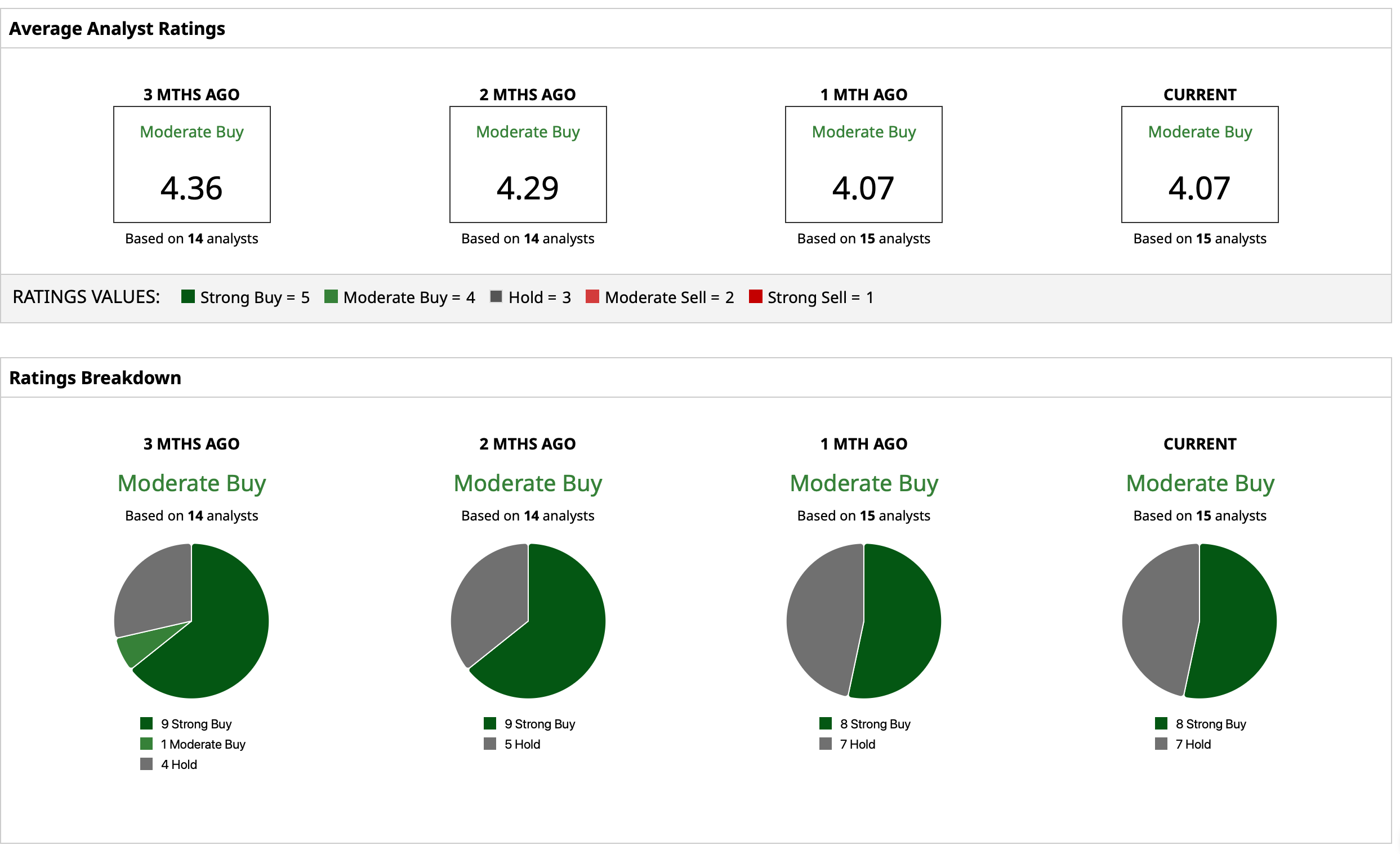

Considering all this, analysts remain cautiously optimistic about NBIS stock, with a mean target price of $236.83. This denotes an upside potential of about 20% from current levels. Out of 15 analysts covering the stock, eight have a “Strong Buy” rating, and seven have a “Hold” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Boeing%20Co_%20sign%20at%20airport-by%20sanfel%20via%20iStock.jpg)