/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)

Barely a week goes by without another megacap cloud provider pledging billions more to AI infrastructure, from data centers and hyperscalers to the server chips that power those systems. The wider market is bracing for that spending to transform the industry, with estimates putting AI’s growth trajectory from about $135 billion in 2023 to more than $20 trillion by 2040.

Over the past six months, Advanced Micro Device’s ((AMD) share price has jumped 147%. This places it firmly among the strongest large‑cap semiconductor names, showing investors’ support. Bank of America is leaning into that story, arguing that “exceptional” demand for AMD’s EPYC server chips and AI accelerators could set up yet another beat‑and‑raise quarter.

For anyone watching the stock, there is an obvious question. How much more room is there for upside if this server demand keeps building?

AMD’s Numbers Back Up BofA’s Beat‑and‑Raise Call

Advanced Micro Devices designs server CPUs, accelerators, and client chips that help big companies and cloud providers handle heavy computing tasks more efficiently. The company is based in Santa Clara, California and now has a market value of $871 billion.

AMD’s stock is up 158% so far this year and 277.8% over the past 52 weeks.

That kind of move has pushed its forward price‑to‑earnings multiple to 90.26 times versus a sector median of 24.75 times, and its price‑to‑sales ratio to 26.26 times compared with a median of 3.37 times, showing the amounts investors are willing to pay for its growth story.

In the first quarter of 2026, the company reported sales of $10.25 billion, with sales growth of -0.17%, which still reflects a very large revenue base. Net income was $13.83 billion and net income growth came in at -8.47%.

Earnings per share for the quarter ending March 2026 landed at $1.11 against a consensus estimate of $1.06, a positive earnings surprise of 4.72%. The balance sheet shows total assets of $79.6 billion, up 3.53%, and total liabilities near $15.2 billion, up 9.00%.

Operating cash flow came in at $2.96 billion, though that figure was down sharply, with operating cash flow growth at -61.67%. Net cash flow was $40 million for the period, representing a -97.71% change, which shows that cash generation tightened versus the prior quarter.

AMD’s AI Server Story

AMD has started ramping production of its next‑generation 6th Gen EPYC processor, called Venice, on TSMC’s 2nm process technology, marking a big step forward for its data center CPU roadmap. The chip is built for heavy compute jobs and AI‑style workloads, with up to 256 Zen 6 cores, a new SP7 socket, and more memory channels that aim for much higher bandwidth per socket.

MEXT adds an important piece to that plan. AMD’s acquisition brings in memory optimization software that helps ease data center bottlenecks by making NAND flash behave more like DRAM in enterprise and cloud environments. The technology uses predictive memory tiering to multiply effective capacity and cut costs linked to DRAM.

Rackspace Technology (RXT) is another part of the picture. Last month, AMD agreed to a 30‑megawatt compute deal that ties its CPUs and accelerators to a large, real‑world deployment. The setup centers on EPYC‑based infrastructure and turns demand for chips into multi‑megawatt contracted capacity.

Progress in autos came as AMD recently won a new autonomous driving customer as it goes after Nvidia Corporation's (NVDA) position in automotive compute, placing its chips inside another area that needs serious processing power.

These exact kinds of fundamental backdrops support expectations for robust earnings and raised guidance on server chip demand.

Street Expectations Set a High Bar

AMD is set to report results for the quarter ending June 2026 on August 4, after the market closes. For that quarter, analysts are looking for earnings of $1.34 per share versus $0.27 a year earlier, which works out to an expected EPS growth rate of 396.30%.

Wells Fargo’s Aaron Rakers has already moved his numbers higher. On June 30, he raised his price target on Advanced Micro Devices to $615 and kept an “Overweight” rating, pointing to stronger earnings potential from AMD’s data center roadmap and the ramp of its next‑generation EPYC chips.

UBS is even more bullish. Its analysts say AMD shares could reach $670 per share, based on the view that the next leg of growth will depend not only upon graphics chips but also on CPUs designed to handle more complex AI‑style workloads, an area where EPYC is expected to play a big role.

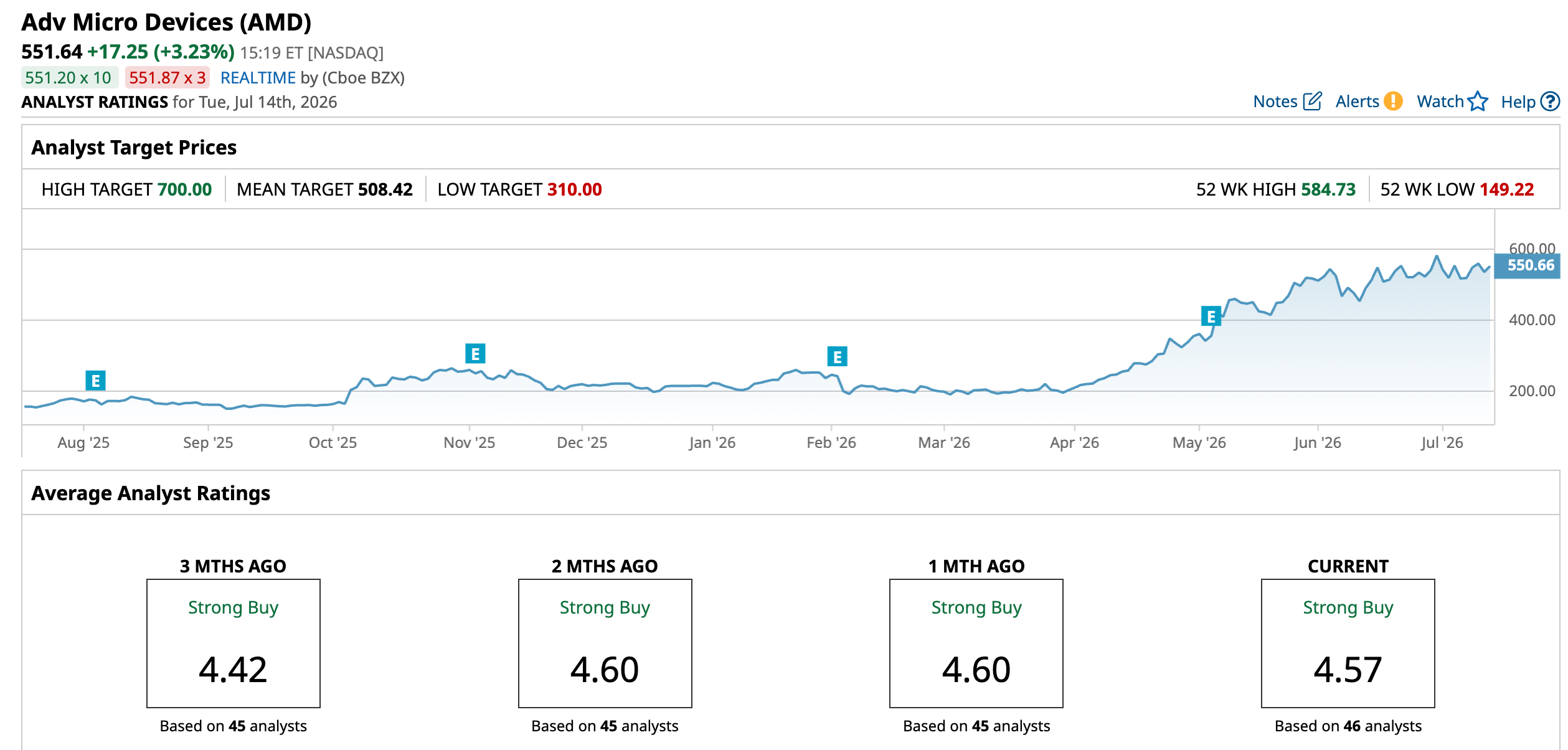

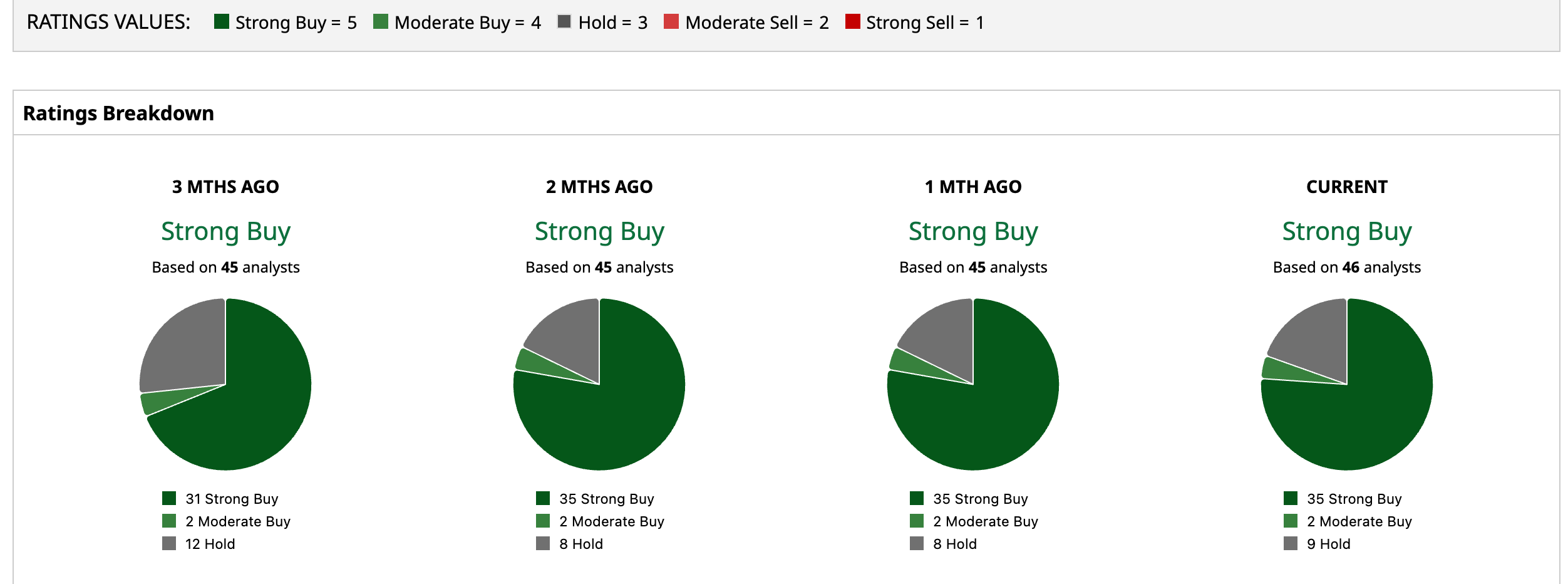

The latest consensus view on AMD is still very positive, with a “Strong Buy” rating based on input from 46 analysts. Their average 12‑month price target sits at $508.42, which actually points to a 7.8% downside. Meanwhile, the Street-high target price of $700 indicates a potential increase of 26.9% from here.

Conclusion

AMD’s story heading into August is pretty straightforward. AI server demand is hot, EPYC and Venice are lining up real workloads, and recent deals and acquisitions are all pointing toward a stronger data center franchise. That makes a beat and raise quarter entirely plausible, especially with consensus already calling for nearly 400% year-over-year (YOY) EPS growth. If the print shows that AI and server momentum is still building rather than flattening, the odds favor shares grinding higher over the next year.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/BlackRock's%20global%20headquarters%20By%20Tada%20Images.jpeg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/The%20CoreWeave%20logo%20displayed%20on%20a%20smartphone%20screen_%20Image%20by%20Robert%20Way%20via%20Shutterstock_.jpg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)