/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)

Advanced Micro Devices’ (AMD) recent gains have arrived on the back of AI inference-induced CPU demand. The market was already waiting for AMD stock to reach a $1 trillion valuation, but another variable has now added a new dimension to its prospects. On June 15, AMD announced the acquisition of MEXT, a memory technology company that will help AMD resolve the memory bottleneck through efficient resource utilization.

To understand what MEXT does, let's first understand how memory is used in AI workloads. Generally, we have two types of memory: flash and DRAM. Flash is cheap storage where vast amounts of data reside. DRAM is fast, expensive, and only used to store data that is currently being processed. MEXT bridges the fundamental trade-off when opting for either of these technologies. Here’s how.

When any processing unit requests data, it can take a lot of time to move that data from flash memory to DRAM. In modern AI workloads, even a fraction of a second where a GPU sits idle can cost the data center vast amounts of money over the long run. MEXT’s predictive tech anticipates upcoming memory access patterns, and before the GPU or CPU can ask for specific data, moves it from flash to DRAM. When the instructions to use the data arrive, it is already available in the DRAM. From the perspective of the GPU, the data was always available, and so it experiences low latency, masked perfectly by intelligent pre-fetching.

Some direct consequences of this include lower infrastructure costs, as eventually less DRAM is used and cheaper flash memory effectively acts as an extension only. Usable memory capacity, i.e. data that the GPU always needs quick access to, also increases. For AMD, getting into this technology early — especially at a time when memory is a severe constraint on AI development — bodes well for the future.

About AMD Stock

Advanced Micro Devices is a semiconductor company that designs high-performance CPUs, GPUs, and adaptive computing solutions. Its product portfolio includes Ryzen and EPYC processors, Radeon graphics cards, and Instinct accelerators for AI and high-performance computing. Founded in 1969, the firm is headquartered in Santa Clara, California, and led by CEO Lisa Su.

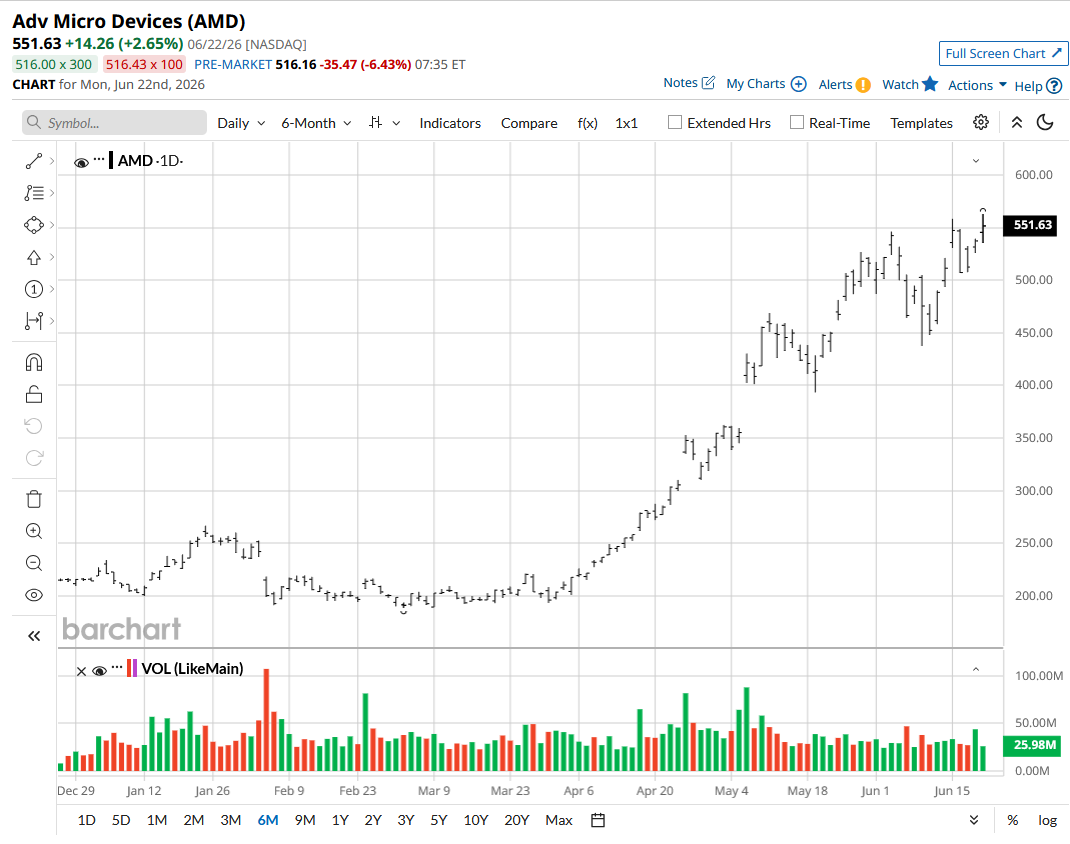

In the last 12 months, AMD stock has climbed 265%, massively outperforming the S&P 500's ($SPX) gained of 21% during the same period. The surge in AI infrastructure demand helped AMD stock recently hit an all-time high. Shares have nearly quadrupled in the past year, reflecting AMD’s strong performance in both CPUs and GPUs, driving strong investor confidence.

AMD Reports Another Stellar Quarter

AMD reported first-quarter fiscal 2026 earnings on May 5, beating analyst consensus estimates on both key metrics. Revenue came in at $10.25 billion compared to the expected $9.89 billion, up 38% year-over-year (YOY). Non-GAAP EPS was $1.37 compared to the expected $1.29, representing an increase of 43% YOY. The Data Center segment — described by Su as the primary driver of AMD’s revenue and earnings growth — reported sales of $5.8 billion, up 57% YOY. The Client and Gaming and Embedded segments reported revenue growth of 23% and 6% YOY, respectively. Free cash flow also jumped from $727 million in Q1 2025 to a record $2.57 billion in Q1 2026. Su noted that the company had an “outstanding” quarter, crediting rising demand for AI infrastructure.

For Q2, AMD expects revenue of approximately $11.2 billion, representing 46% YOY growth. Su said the company has strong and increasing confidence in its ability to earn tens of billions of dollars in data-center AI revenue next year. She believes server growth will increase substantially as AMD increases its supply to meet the high demand. AMD is also confident that it can grow its server CPU market share to more than 50%. The demand for AMD’s next-generation AI GPU, MI450, is higher than what the company anticipated for 2027 from OpenAI and Meta Platforms (META), and there are multiple other customers placing orders.

What Do Analysts Say About AMD Stock?

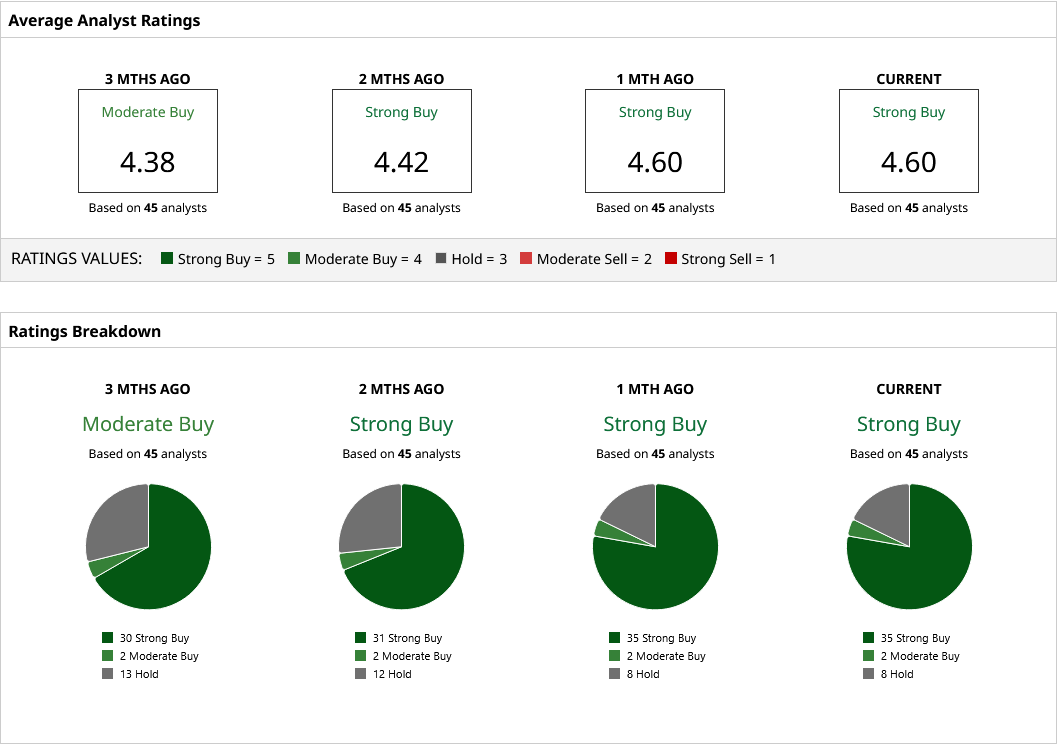

Citi analyst Atif Malik recently increased his price target for AMD from $460 to $575, while upgrading his rating from “Neutral” to “Buy.” Malik stated that while investors have continued to view AMD as a CPU company, the firm is positioning itself as a legitimate second source in the GPU market. The analyst believes AMD is likely to win the majority of Meta’s GPU orders, and that AMD's share price does not fully include its GPU potential. Bank of America analyst Vivek Arya also recently increased his price target from $500 to $560 while maintaining a “Buy” rating.

Based on 45 analysts with coverage, AMD stock holds a consensus “Strong Buy” rating. The mean price target of $477.12 indicates potential downside of 10% from current levels. This negative figure reflects how strongly the share price has risen compared to Wall Street's recent expectations.

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Boeing%20Co_%20sign%20at%20airport-by%20sanfel%20via%20iStock.jpg)