/Amazon%20pickup%20%26%20returns%20building%20by%20Bryan%20Angelo%20via%20Unsplash.jpg)

Amazon (AMZN) is making another massive bet on artificial intelligence (AI). The e-commerce and cloud giant recently announced plans to raise $25 billion through an eight-part bond offering, with proceeds set to fund AI infrastructure, data centers, and other long-term capital needs. The move comes just months after Amazon sold $37 billion in bonds earlier this year, highlighting how aggressively the company is expanding its AI footprint.

Investor demand was anything but weak. According to reports, orders for the new debt offering peaked at roughly $62 billion, suggesting bond investors remain highly confident in Amazon's financial strength despite its enormous spending plans.

The announcement barely moved AMZN stock because Wall Street largely expected another round of financing. Instead, investors remain focused on one question: Will Amazon's huge AI investments eventually generate enough earnings to justify the spending?

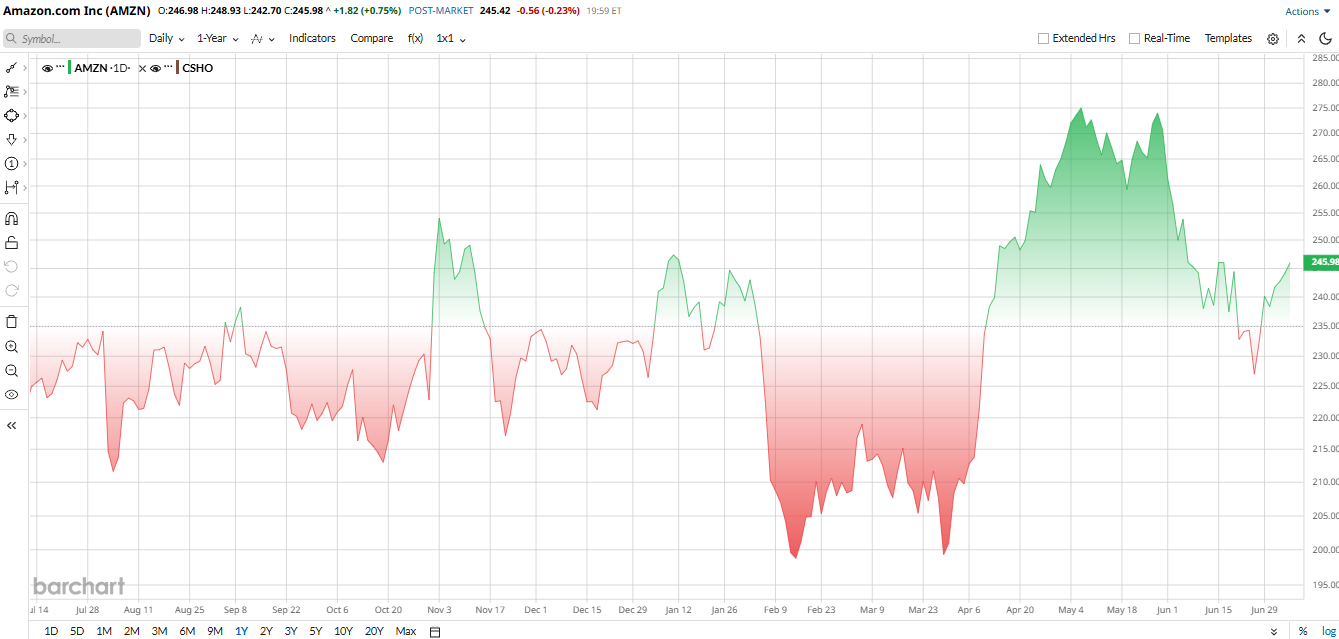

Amazon Stock Has Lagged in 2026

Amazon shares have delivered a surprisingly muted performance recently. AMZN stock gained only about 5% during 2025 and has struggled to build momentum in 2026. Shares are now up 7% year-to-date (YTD).

The weakness isn't being driven by slowing demand. Instead, investors have become increasingly cautious about Amazon's plans to spend nearly $200 billion this year on AI infrastructure, cloud expansion, and fulfillment upgrades. While many believe these investments will strengthen Amazon's competitive position, others worry that near-term profit margins could remain under pressure as spending accelerates.

Amazon continues to trade at a premium compared with much of the market. The stock changes hands at roughly 31.7 times forward earnings, slightly above the broader tech sector average of around 28 times and well ahead of the retail industry median near 19 times.

If Amazon continues delivering strong cloud growth and expanding AI services, today's valuation could prove justified. However, any slowdown in Amazon Web Services (AWS), weaker retail demand, or higher interest rates could put pressure on the stock because expectations remain exceptionally high.

Earnings Show Why Investors Remain Optimistic

Amazon's first-quarter 2026 results easily exceeded Wall Street's expectations. Revenue climbed 17% year-over-year (YOY) to $181.5 billion, driven by strength across nearly every business. The biggest standout was AWS, which saw revenue surge 28% YOY to $37.6 billion. AWS continues to benefit from accelerating enterprise demand for cloud computing and AI infrastructure.

Net income jumped to $30.3 billion, while EPS rose to $2.78, although those figures included a significant one-time gain tied to Amazon's investment in Anthropic. However, cash generation told a different story. Trailing 12-month free cash flow fell sharply to $1.2 billion from $25.9 billion as capital expenditures exploded YOY.

Even so, Amazon finished the quarter with approximately $90.1 billion in cash and equivalents, giving it plenty of financial flexibility to continue funding its AI expansion. Management also issued upbeat guidance for Q2, forecasting revenue between $194 billion and $199 billion alongside operating income of $20 billion to $24 billion.

Amazon Is Investing Far Beyond AI Data Centers

The bond sale is only one piece of Amazon's broader expansion strategy.

The company recently introduced Proteus, its next-generation AI-powered warehouse robot, as part of a roughly $12 billion investment aimed at modernizing European fulfillment operations. Amazon also plans to deploy its STARK robotic technology across multiple European facilities over the next several years.

Outside of logistics, the company continues expanding its grocery and same-day delivery network. More than 25 new ultra-fast delivery centers are scheduled to open across Europe, while same-day grocery delivery continues to expand throughout the U.S. and Japan.

Amazon is also preparing to introduce Alexa+ devices in additional international markets, further strengthening its consumer AI ecosystem.

Taken together, these projects explain why management expects capital spending to exceed $200 billion this year.

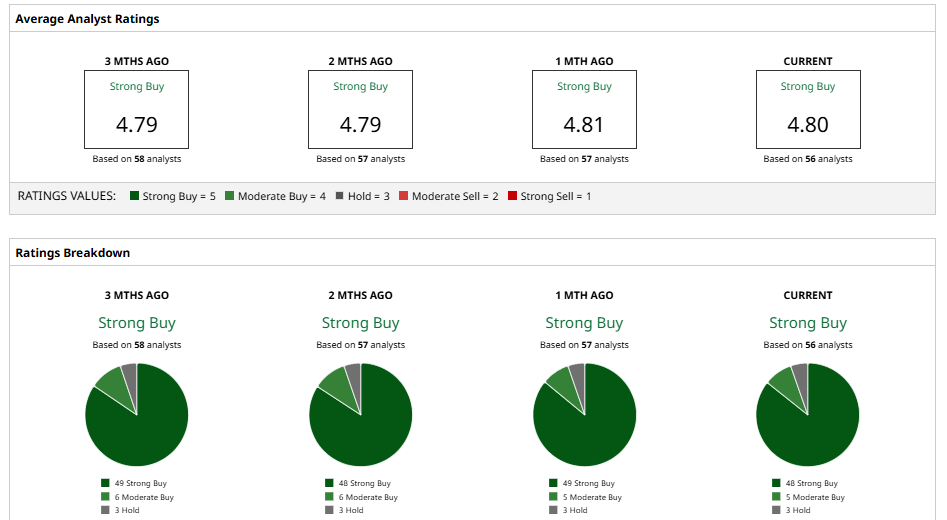

Analysts Still See Meaningful Upside for Amazon Stock

Despite Amazon's enormous spending plans, Wall Street remains overwhelmingly optimistic. The consensus rating among 56 analysts is a “Strong Buy,” with 53 of those analysts recommending buying the stock and virtually no sell ratings.

The average price target sits at $315.44, implying roughly 28% potential upside from current trading levels.

Several major firms have recently reiterated their bullish views on AMZN stock. Morgan Stanley continues to view Amazon as one of its favorite internet stocks, pointing to accelerating AWS growth and long-term AI demand. Goldman Sachs has also defended Amazon's elevated capital spending, arguing today's investments should strengthen future profitability rather than weaken the business.

The most contentious issue isn't how much Amazon is spending. It's whether those investments will profit stockholders rapidly enough to justify AMZN stock's premium valuation.

But to the long-view side of the fence, the bond offering communicates a single sentiment pretty clearly. Amazon is not just dead serious about being deep in next-gen AI infrastructure — it's willing to do what's necessary to get there, and that may involve some short-term pain.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/BlackRock's%20global%20headquarters%20By%20Tada%20Images.jpeg)

/The%20CoreWeave%20logo%20displayed%20on%20a%20smartphone%20screen_%20Image%20by%20Robert%20Way%20via%20Shutterstock_.jpg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)