With a market cap of around $15 billion, Healthpeak Properties, Inc. (DOC) is a leading healthcare real estate investment trust (REIT), focused on owning, operating, and developing high-quality healthcare properties across the United States. It maintains a diversified portfolio spanning outpatient medical facilities, laboratory buildings, and continuing care retirement communities (CCRCs).

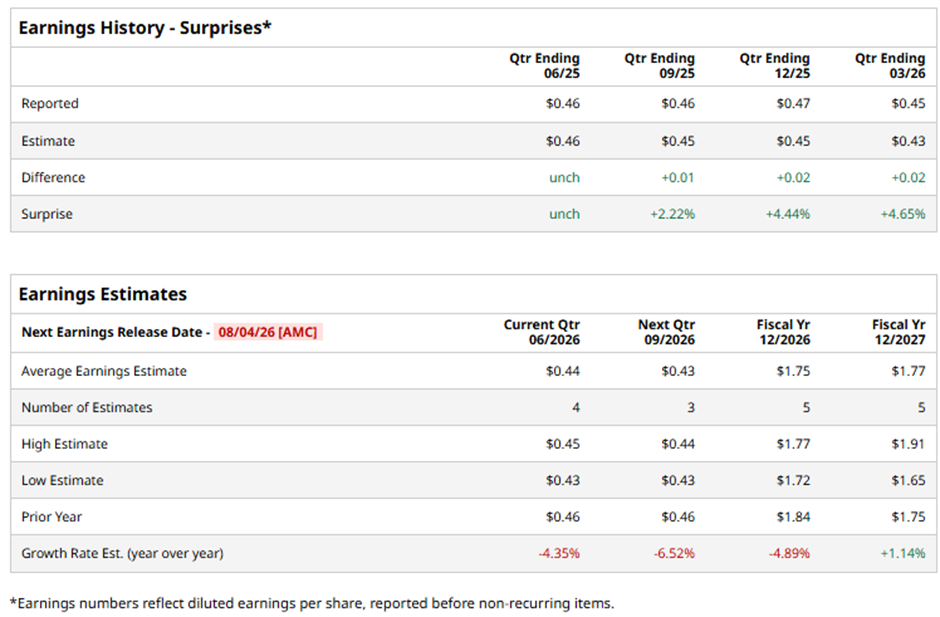

The Denver, Colorado-based company is expected to release its fiscal Q2 2026 results after the market closes on Tuesday, Aug. 4. Ahead of this event, analysts project DOC to report an FFO as Adjusted of $0.44 per share, a decline of 4.4% from $0.46 per share in the year-ago quarter. However, it has surpassed or met Wall Street's bottom-line estimates in the last four quarterly reports.

For fiscal 2026, analysts forecast Healthpeak Properties to report FFO as Adjusted of $1.75 per share, down 4.9% from $1.84 in fiscal 2025. However, FFO as Adjusted is anticipated to rise 1.1% year-over-year to $1.77 per share in fiscal 2027.

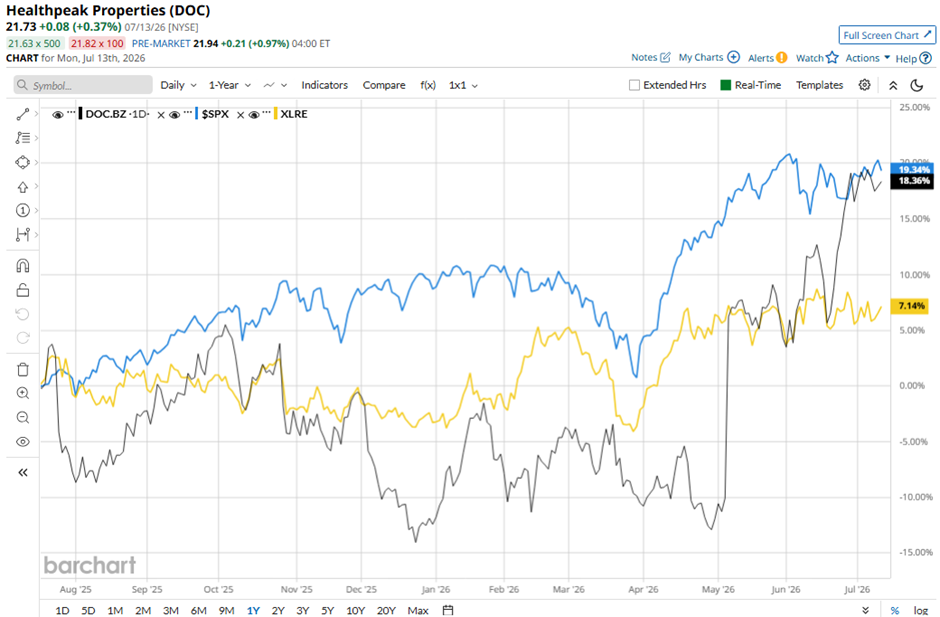

DOC stock has increased 17.8% over the past 52 weeks, lagging behind the broader S&P 500 Index's ($SPX) 20.1% gain. However, it has outpaced the State Street Real Estate Select Sector SPDR ETF's (XLRE) 7.5% return over the same time frame.

Shares of Healthpeak Properties surged 18.1% following its Q1 2026 results on May 5 as the company reported adjusted FFO of $0.45 per share and revenue rose to $753 million, beating analyst expectations. Investor sentiment was further boosted after the company slightly raised its full-year 2026 adjusted FFO guidance to $1.71 per share - $1.75 per share and highlighted strong leasing activity, including 1.2 million square feet of outpatient medical and lab lease executions with positive cash releasing spreads of +5.4% for outpatient renewals and +3.5% for lab renewals.

The successful IPO of Janus Living (JAN) at the high end of its valuation range, which generated approximately $880 million in net proceeds, also strengthened investor confidence despite higher quarterly operating expenses of $747.4 million.

Analysts' consensus view on DOC stock is cautiously optimistic, with an overall "Moderate Buy" rating. Among 22 analysts covering the stock, six suggest a "Strong Buy," one gives a "Moderate Buy," and 15 recommend a "Hold." As of writing, it is slightly trading above the average analyst price target of $21.71.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/BlackRock's%20global%20headquarters%20By%20Tada%20Images.jpeg)

/The%20CoreWeave%20logo%20displayed%20on%20a%20smartphone%20screen_%20Image%20by%20Robert%20Way%20via%20Shutterstock_.jpg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)