/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)

Chip giant Advanced Micro Devices (AMD) has gained 160.5% this year as investors have rewarded its AI ambitions, particularly in its CPUs and accelerators. A notable factor in this rise has been analysts' faith in the chipmaker, which commands a “Strong Buy” rating. In fact, AMD was among the chip stocks that added $2 trillion in combined value during the second quarter. One major focal point in AMD’s growth story has been its partnership with Meta Platforms (META) and OpenAI, where the company locked in twin 6-gigawatt GPU supply deals.

About AMD Stock

Advanced Micro Devices is a global semiconductor company that develops processors and graphics solutions for data centers, personal computers, gaming, and embedded applications. Its business centers on designing high-performance, adaptive chips and managing the research, development, supply chain, and commercial operations required to deliver them worldwide. The company is based in Santa Clara, California and holds a market capitalization of $891.5 billion.

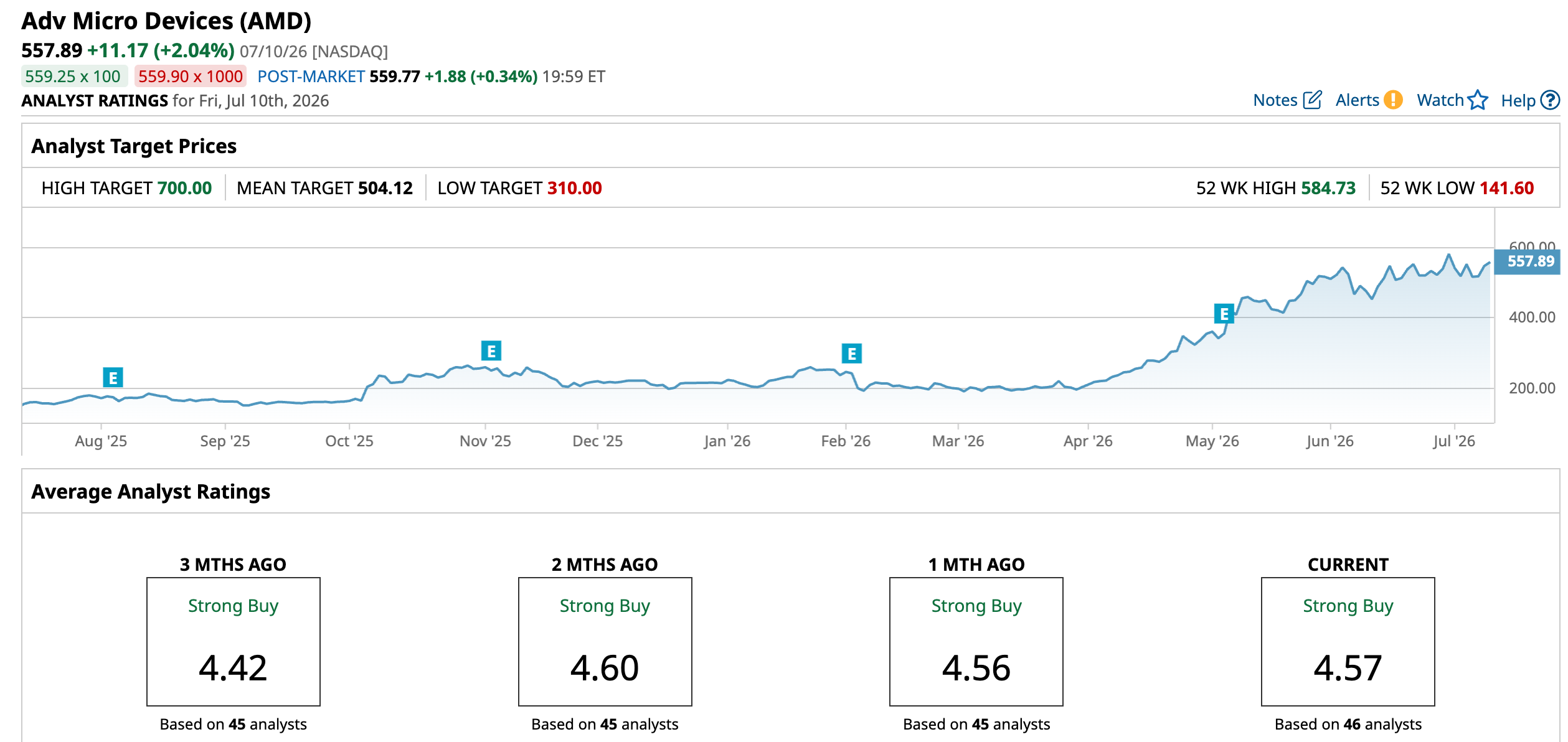

As investors price in a much stronger AI-driven growth story, especially in data center CPUs and accelerators, the stock has risen robustly over the past year. This growth has also been supported by major AI partnership news, improved earnings and revenue momentum, and upbeat guidance. Over the past 52 weeks, the stock has gained 287%, while it is up 160.5% year-to-date (YTD). The company’s shares reached a 52-week high of $584.73 on June 30, but are down 4.6% from that level.

AMD has a 14-day relative strength index (RSI) of 57.47, which is closer to the overbought territory than the oversold territory. On a forward-adjusted basis, AMD’s price-to-earnings (Non-GAAP) ratio of 73.85 times is higher than the industry average of 25.02 times.

AMD's Q1 Results: Data Center Growth and Strong AI Demand Lift Outlook

AMD reported strong first-quarter results driven by demand for AI infrastructure, with data centers as the primary growth driver. The company’s revenue increased by 38% year-over-year (YOY) to $10.25 billion, exceeding the $9.85 billion expected by Wall Street analysts. Data Center segment reported revenue of $5.80 billion, up 57% YOY, driven by strong demand for AMD EPYC processors and the continued ramp of AMD Instinct GPU shipments.

AMD’s non-GAAP gross margin climbed by one percentage point to 55%, while its non-GAAP operating income increased 43% YOY to $2.54 billion. The company’s non-GAAP EPS rose 43% from the prior-year period to $1.37, surpassing the $1.30 expected by Street analysts.

For the second quarter (to be reported on Aug. 4, after the market closes), AMD expects revenue of approximately $11.20 billion, plus or minus $300 million, representing about 46% YOY growth, with non-GAAP gross margin of approximately 56%.

Wall Street analysts are robustly optimistic about AMD’s future earnings. They expect the company’s EPS to climb by 400% YOY to $1.35 for Q2 2026. For fiscal 2026, EPS is projected to surge 88.1% annually to $6.15, followed by a 76.1% growth to $10.83 in fiscal 2027.

What Do Analysts Think About AMD’s Stock?

Goldman Sachs analyst James Schneider maintained a “Buy” rating on AMD’s stock and raised the price target from $450 to $640 at the start of July. The analyst cited surging demand for high-performance CPUs driven by the shift to agentic AI workloads. The reasoning is that while AI model training is GPU-intensive, AI inference in real-world applications requires a mix of CPUs and GPUs.

Wells Fargo analysts also raised the firm’s price target from $505 to $615, while keeping an “Overweight” rating on the stock. The firm said stronger demand for EPYC server CPUs, along with better pricing, is driving the higher forecast. It also said it still expects data center GPU revenue to come in above Street estimates, while its 2027 and 2028 EPS estimates rise to $13.40 and $18.75.

Citigroup analysts also upgraded the stock from “Neutral” to “Buy” and hiked the price target from $460 to $575. Analyst Atif Malik believes that AMD is “emerging as a legit second source” in the GPU market. Citi believes the company is well placed to secure the bulk of the opportunities at Meta.

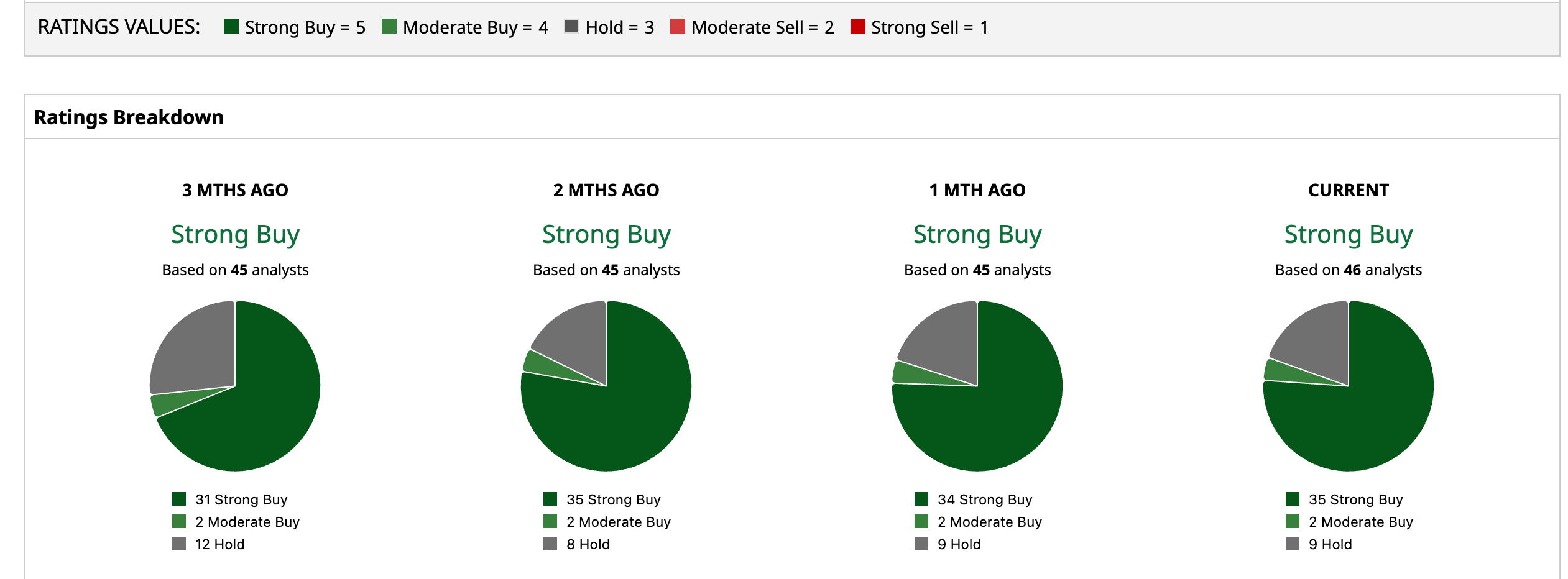

Chip giant AMD is an extremely popular name on Wall Street, with analysts awarding it a consensus “Strong Buy” rating overall. Of the 46 analysts rating the stock, a majority of 35 analysts have given it a “Strong Buy” rating, two analysts rated it “Moderate Buy,” while nine analysts are taking the middle-of-the-road approach with a “Hold” rating. The consensus price target of $504.12 represents a 9.64% downside from current levels. However, the Street-high price target of $700 reflects a 25.47% upside.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20corporate%20sign%20for%20SK%20Hynix%20by%20Tada%20Images%20via%20Adobe%20Stock.jpeg)

/Server%20racks%20by%20dotshock%20via%20Shutterstock.jpg)

/2d%20illustration%20of%20Cloud%20computing%20by%20Blackboard%20via%20Shutterstock.jpg)

/Alibaba%20by%20Photo%20Agency%20via%20Shutterstock.jpg)