/Alibaba%20by%20Photo%20Agency%20via%20Shutterstock.jpg)

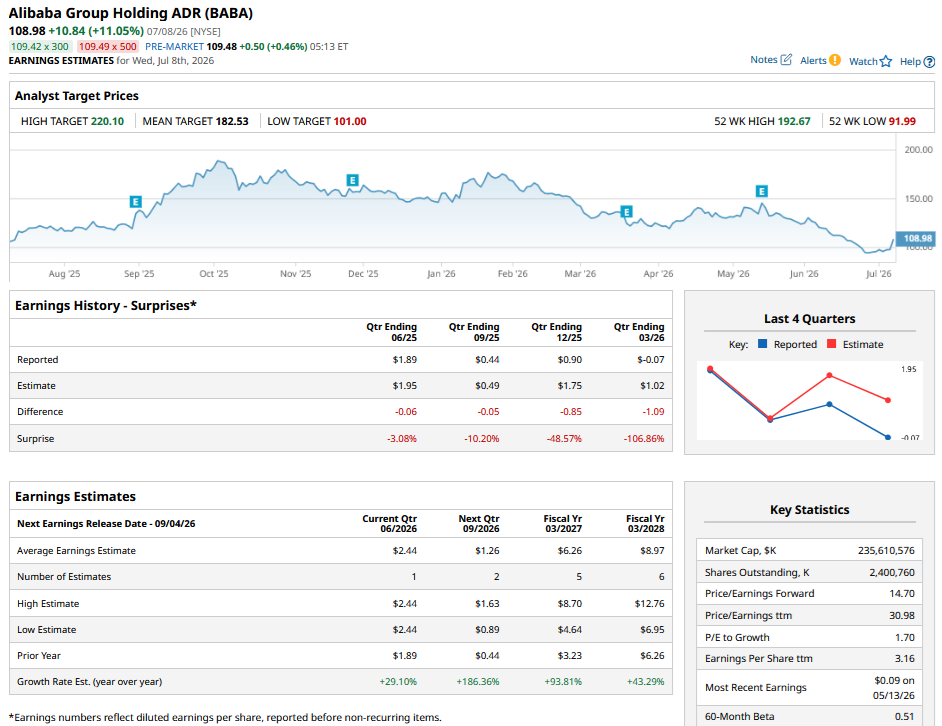

While Alibaba (BABA) stock has rebounded from its 2026 lows, shares are still down more than 22% for the year. In late June, I previously noted that BABA stock was a “buy” as it drifted toward its 52-week lows. BABA stock subsequently went on to hit a fresh 52-week low of $91.99 on June 26, but it has since recovered to levels higher than when I last reported on shares, climbing an exceptional 11% on July 8 alone.

Let's take a look at whether BABA stock can continue its rise in 2026 after its mammoth rally earlier this week.

Why Is BABA Stock Going Up?

The rise in Alibaba stock came amid a broad-based rally in Chinese artificial intelligence (AI) stocks. Notably, Alibaba is the leading AI player in China, and its Qwen app is among the most used AI apps in the country.

Alibaba has partnered with several companies, including BMW (BMWKY) and SAP (SAP), and is also collaborating with Apple (AAPL) to bring AI features to iPhones in China. Given China’s strict data policies, any foreign company looking to offer AI services in China may need to partner with domestic companies, which is an opportunity for firms like Alibaba.

Alibaba is the leader in China’s AI cloud market with a market share higher than the next three competitors. In the March quarter, the AI-related revenue of its cloud segment rose by the triple digits for the 11th consecutive quarter. The company has also developed AI chips that will not only help it lower its reliance on third parties but could become a significant source of revenue as the firm signs up third-party customers. Additionally, Alibaba has data centers in countries like France, Malaysia, Mexico, and Japan, which makes it a growing player in the global AI market.

Meanwhile, the BABA stock rally on July 8 was further bolstered by Chinese media reports that Alibaba told analysts its profits were steady in the June quarter. Incidentally, in recent quarters, the company's profits have been hammered by growing AI capex and losses in its instant commerce business.

Most recently, in the March quarter, Alibaba's adjusted EBITA plunged 84% year-over-year (YOY) to $740 million, while the firm barely reached break-even on the adjusted net profit level. The results were not much different from the previous few quarters, where Alibaba reported a sharp decline in profitability for the same reasons. Given the deterioration in Alibaba’s profitability in the last fiscal year, reports of profitability stabilizing and narrowing instant commerce losses came as a big relief to markets.

Alibaba Stock Should Continue to Rise

Alibaba’s profits are expected to rebound sharply over the next two years, and consensus estimates call for EPS of $8.97 in the fiscal 2028, implying a 2028 forward price-to-earnings (P/E) multiple of 12.5 times. To be sure, this multiple is based on analysts’ earnings estimates, which are not static and subject to change. If anything, over the last month, analysts have lowered Alibaba’s earnings estimates for the current fiscal year.

That said, I continue to find BABA stock attractive here. Alibaba outperformed by a big margin last year and was the market's favorite Chinese AI stock. However, the AI trade has shifted to Taiwan and South Korea this year. The two countries are home to some of the biggest chip and memory firms, which have been the flagbearers of the AI trade for the last few months.

Still, as I have noted previously, the rally in chip and memory companies has gone a bit too far, and sooner than later the market should rediscover its lost love for the likes of Alibaba in China and the "Magnificent Seven" in the United States. While China’s slowdown, a lack of fresh government stimulus, losses in the instant commerce business, and concerns over burgeoning AI capex are some risks investors should watch for, I believe the risk-reward equation is tilted favorably toward BABA stock at these levels. I expect to see Alibaba stock go higher from here.

On the date of publication, Mohit Oberoi had a position in: BABA . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Space/Rocket%20launching%20into%20space%20by%20BEST%20BACKGROUNDS%20via%20Shutterstock.jpg)

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/Close-up%20shot%20of%20Rivian%20R1T_%20Image%20by%20Trong%20Nguyen%20via%20%20Shutterstock_.jpg)