/Builders%20FirstSource%20Exterior%20and%20Trademark%20Logo%20By%20Wolterke.jpeg)

With a market cap of $8 billion, Builders FirstSource, Inc. (BLDR) is a leading supplier of building materials, manufactured components, and construction services for professional builders, remodelers, and contractors across the United States. The company offers a wide range of products and solutions, including engineered wood, modular homes, windows, doors, millwork, and installation services, while also providing design, estimating, and virtual homebuilding support.

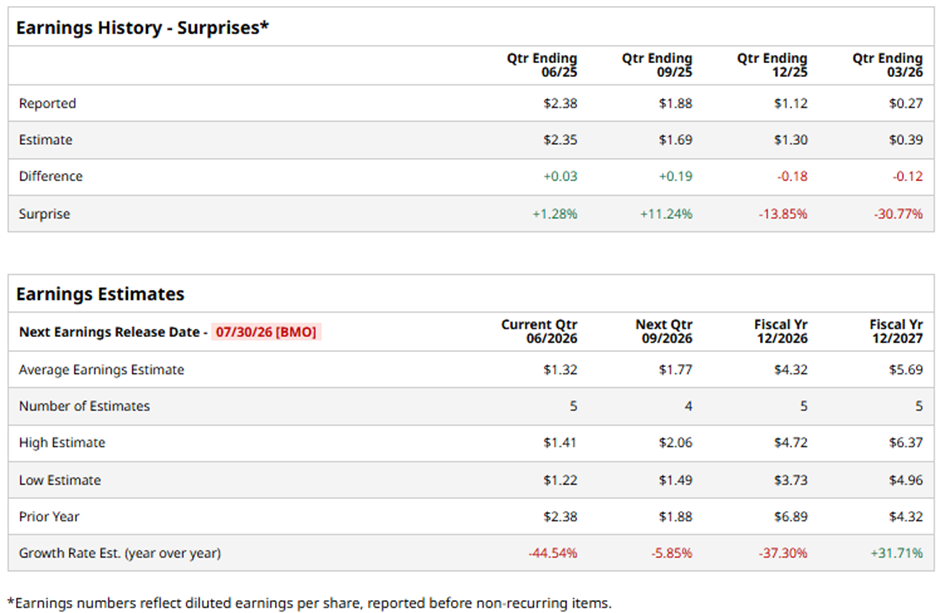

The Irving, Texas-based company is expected to release its fiscal Q2 2026 results before the market opens on Thursday, Jul. 30. Ahead of this event, analysts project BLDR to report an adjusted EPS of $1.32, a 44.5% decrease from $2.38 in the year-ago quarter. It has exceeded Wall Street's bottom-line estimates in two of the last four quarters while missing on two other occasions.

For fiscal 2026, analysts forecast the construction supply company to report adjusted EPS of $4.32, down 37.3% from $6.89 in fiscal 2025. However, adjusted EPS is projected to increase 31.7% year-over-year to $5.69 in fiscal 2027.

BLDR stock has declined 43.2% over the past 52 weeks, lagging behind the broader S&P 500 Index's ($SPX) nearly 20% return and the State Street Industrial Select Sector SPDR ETF's (XLI) 20.6% gain over the same period.

Shares of Builders FirstSource fell 5.2% on Apr. 30 after the company reported weak Q1 2026 results, with net sales declining 10.1% year-over-year to $3.3 billion and adjusted EBITDA dropping 42.1% to $213.8 million amid a softer housing starts environment and commodity deflation. Investors were also concerned as the company posted a net loss of $47.4 million, or $(0.43) per share while adjusted EPS plunged to $0.27.

In addition, BLDR’s adjusted EBITDA margin fell 360 basis points to 6.5%, net debt leverage rose to 3.2x, and management’s 2026 outlook projected continued weakness with single-family and multifamily housing starts expected to decline low-single digits.

Analysts' consensus view on BLDR stock is cautiously optimistic, with an overall "Moderate Buy" rating. Among 24 analysts covering the stock, 10 suggest a "Strong Buy," two give a "Moderate Buy," 11 provide a "Hold" rating, and one has a "Strong Sell." The average analyst price target is $96.24, indicating a potential upside of 25.8% from the current levels.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/Microsoft%20headquarters%20By%20Peter.jpeg)