/AI%20(artificial%20intelligence)/Data%20Center%20by%20Caureem%20via%20Shutterstock%20(2).jpg)

The two most common types of criticism that neoclouds receive are that they have too much debt and that they’re just renting GPUs. While these concerns may seem like genuine red flags, they miss the whole point of what a neocloud does. By definition, neclouds offer GPU-as-a-Service (GPUaaS). They’re the middlemen who buy compute and then resell it. Since compute is in extremely high demand, they can charge a premium, resulting in a hefty profit over their cost of capital.

This is also the reason why neoclouds have so much debt. Raising capital isn’t just part of the business model — it is practically the whole thing. Neoclouds take money from debt and equity investors and invest it into GPUs, much like a bank takes people’s money and invests it into assets.

For a company like CoreWeave (CRWV), the bull thesis is all about being in the right place at the right time. The company offers the operating excellence that is needed to run a cloud, orchestration, and API services. It also has the right relationships with the right vendors for access to the latest silicon, giving you the certainty that you have access to the best hardware. Once you have this capability, every single dollar you put into the business can give you incremental returns well above the cost of capital, assuming the demand for compute stays strong.

For now, compute demand is unlikely to go down. So when a firm like Meta Platforms (META) announces that it is entering the cloud infrastructure business, it is playing the same game as CoreWeave. It is a new entrant in a game already perfected by smaller, more nimble companies. Does it pose a threat to them? Sure, any business with Meta as their competitor should feel scared. But the caveat here is compute demand. With unlimited compute demand, in the presence of hardware bottlenecks causing supply issues, a new entrant isn’t necessarily affecting anyone’s business. Accordingly, the overreaction to the Meta news — and the subsequent decline in CRWV stock — represents a great buying opportunity for investors.

About CoreWeave Stock

CoreWeave is a cloud infrastructure company that provides GPU-accelerated computing for AI workloads. Its services include GPU compute, CPU compute, cloud storage, and networking. Founded in 2017, the company is headquartered in Livingston, New Jersey, and has a market capitalization of $38.7 billion.

Over the last 12 months, CRWV stock has declined by 48%, significantly underperforming the S&P 500’s ($SPX) 20% gain during the same period. CoreWeave stock has been fairly volatile, falling to as low as $67 in late March before approximately doubling to around $138 by early May. The rise was primarily driven by a landmark $21 billion deal with Meta as well as a strong earnings beat. CRWV stock recently fell again, though, after reports surfaced about Meta building its own cloud business. Concerns about CoreWeave facing competition from one of its biggest customers reduced CRWV stock by 14% in just one day.

CoreWeave Delivers Record Bookings Amid Rising Losses

CoreWeave reported first-quarter fiscal 2026 earnings on May 7. Revenue of $2.08 billion grew 112% year-over-year (YOY), beating the analyst consensus of $1.96 billion. However, loss per share of $1.40 missed the expected loss of $1.20 per share. Net loss also more than doubled from the same quarter last year, widening from $315 million to $740 million in Q1 2026, driven by heavy capital spending and rising interest expense. Despite the losses, CEO Michael Intrator described the period as the “strongest bookings quarter” in company history, with revenue backlog reaching nearly $100 billion.

CFO Nitin Agrawal reaffirmed the company’s full-year outlook on the earnings call. Agrawal believes the current margin pressure is temporary and should improve through the year, reaching low double digits by Q4. For fiscal 2026, the company now expects capital expenditures of $31 billion to $35 billion, with increased spending due to rising component and equipment prices.

What Are Analysts Saying About CoreWeave Stock?

In June, Cantor Fitzgerald analyst Brett Knoblauch reiterated an “Overweight” rating on CRWV stock with a price target of $167. The analyst believes that CoreWeave is on track to sign approximately $40 billion in new contracts in Q2, matching the record set in Q1. He also stated that the firm has already locked in 90% of the contracts needed to reach its $30 billion annual revenue target for 2027. Similarly, Wells Fargo analyst Michael Turrin has an “Overweight” rating on CoreWeave with a price target of $155 per share.

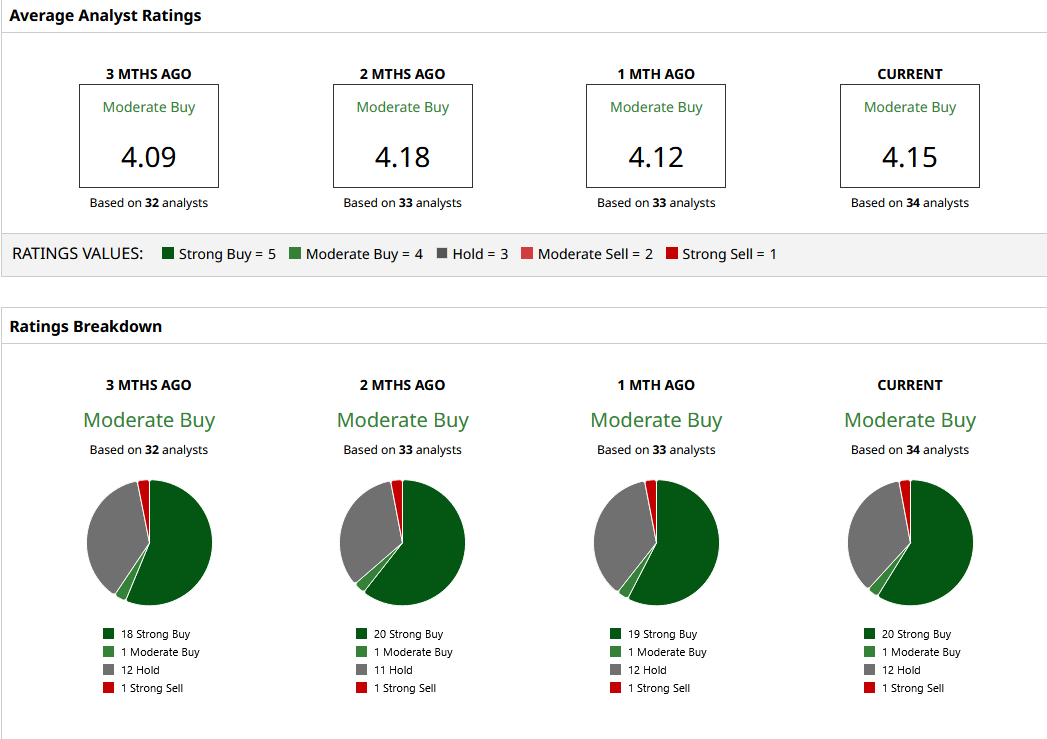

Based on 34 analysts with coverage, CoreWeave stock holds a consensus “Moderate Buy” rating. The mean price target of $139.31 indicates potential upside of 67% from here. Of those 34 analysts, 20 suggest a “Strong Buy,” one has a “Moderate Buy,” 12 analysts have a “Hold” rating, and only one analyst suggests a “Strong Sell,” reflecting that most analysts believe in the firm’s near-term growth. The strong analyst confidence also derives from the fact that CRWV stock has declined rapidly despite serious revenue growth and record bookings, making it a potentially attractive entry point for investors.

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/AI%20technology%20-%20by%20Wanan%20Yossingkum%20via%20iStock.jpg)

/Johnson%20%26%20Johnson%20location%20sign-by%20JHVEPhoto%20via%20iStock.jpg)

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)