/Microsoft%20logo%20on%20building%20by%20franz12%20via%20iStock.jpg)

Software giant Microsoft (MSFT) will be letting go of thousands of employees yet again. This time, the number is set to be 4,800, or 2% of its global workforce, with about two-thirds expected to be from its gaming and entertainment division, Xbox.

Newly installed Xbox CEO Asha Sharma has cited lower gross margins than competitors, stating in an internal memo to employees that the console maker was “losing 64 cents for every dollar invested.”

Thus, with this latest round of layoffs, Microsoft has shed close to 35,000 employees in the past three and a half years. Was this rewarding for shareholders? As harsh as it may sound… yes, it has paid off, so far at least. Operating margins have increased to 46.3% from 42.3%, and MSFT stock is up 72% in the same period. And while it has not been explicitly stated, the cost savings have flown into the company's AI endeavors, headlined by its cloud business Azure, which has been narrowing the lead with Amazon's (AMZN) AWS.

However, the division primarily impacted this time is Xbox. Will this round of layoffs finally provide a fillip to it?

Xbox Lagging

The $69 billion acquisition of Activision Blizzard was supposed to herald a new era for Microsoft's gaming division. CEO Satya Nadella, sounding gung-ho about gaming in general, had then said, “Gaming is the most dynamic and exciting category in entertainment across all platforms today and will play a key role in the development of metaverse platforms. We’re investing deeply in world-class content, community and the cloud to usher in a new era of gaming that puts players and creators first and makes gaming safe, inclusive and accessible to all.”

However, later that year, generative AI had its breakout moment with OpenAI's ChatGPT, in which Microsoft was heavily invested (and still is). And so, gaming became secondary, and AI took over as the priority for Microsoft.

CEO Asha Sharma has asserted that consumers spend about 70 billion hours on the Xbox ecosystem in a year; the consequent finances are not reflective of this staying power.

Sales are down 5% on a year-over-year (YoY) basis in the latest quarter, operating at a 3% profit margin against the roughly 30% Microsoft expects from its major divisions. On consoles specifically, Xbox Series X and S sold approximately 9.8 million units in 2023 and collapsed 51% to 4.79 million in 2024, with cumulative lifetime sales sitting at roughly 34 million units through 2025. By contrast, Sony's (SONY) PlayStation 5 has sold over 65 million units lifetime, nearly double Xbox's current generation total, while Nintendo's (NTDOY) Switch 2, which launched in June 2025, captured dominant global hardware market share across every major region

Game Pass, Xbox's primary subscription vehicle, reached 34 million subscribers in February 2024 but then shed millions of users after a 50% price hike in October 2025 pushed the Ultimate tier from roughly $19.99 to $29.99 per month, and Microsoft has not disclosed subscriber counts since. To bring these subscribers back and gain new ones, Sharma announced an immediate price reduction, bringing the monthly cost of Game Pass Ultimate down from the peak of $30 to $23/month. The result? Thus far, it hasn't been enough to bring them back, which may have ultimately led to the layoff.

Thus, Sharma's strategy now should be to leverage Xbox's massive IP, which includes iconic names of the gaming world like Call of Duty, Minecraft, Fallout, and Diablo, among others. Further, the growth model going forward is explicitly platform agnostic, releasing games on PC and rival consoles from Sony and Nintendo to reach players beyond Xbox's shrinking hardware base, while holding back a handful of true exclusives like Gears of War: E-Day to give hardware owners a reason to stay.

In terms of AI, while Sharma pulled the plug on Copilot from consoles, Project Tokolos will be taking center stage. Still circling within company insiders, Project Tokolos is an AI frame generation system designed to double perceived frame rates at the platform level so every game benefits without developer integration. Additional AI efforts include AI-driven bitrate adaptation for Xbox Cloud Gaming that already reduces data usage by 40% without visible quality loss, a material edge for subscriber growth in bandwidth-constrained markets like India and Brazil.

Finally, there is Project Helix, which Sharma, in a post on X (formerly Twitter), described as a next-generation console that will lead in performance and play both Xbox and PC games, collapsing a divide that the industry has maintained for two decades. Notably, Project Helix will run on a custom AMD (AMD) System on Chip (SoC), with the leaked codename Magnus, built on AMD's RDNA 5 GPU architecture and Zen 6 CPU, paired with a dedicated NPU capable of up to 110 TOPS at 6 watts, a figure that dwarfs anything in current generation consoles. The NPU underpins AMD's FSR Diamond technology, which integrates hardware-level machine learning upscaling, multi-frame generation, and ray regeneration directly into the silicon, with Microsoft promising an order of magnitude leap in ray tracing performance over the Xbox Series X.

Microsoft's Otherwise Top-Notch Financials

Microsoft's financial performance continues to underscore the reasons for its longstanding favor among investors despite occasional skepticism. Over the past decade, the company has expanded revenue at a compound annual growth rate of 13.86% and earnings at 28.15%, while its market capitalization has multiplied tenfold during the same timeframe.

In the most recent quarter, Microsoft exceeded revenue projections by about $1.5 billion and delivered its tenth consecutive earnings beat. Revenue for the third quarter of 2026 reached $82.9 billion, reflecting an 18% increase from the year-earlier period. The cloud business maintained robust momentum with 29% YoY growth to $54.5 billion, supported by a 99% rise in commercial remaining performance obligations to $627 billion. This performance stands out for a firm that some had questioned as losing relevance.

Earnings per share advanced 23% to $4.27, surpassing the consensus estimate of $4.06, marking the tenth consecutive quarter of earnings beat from the company.

Operating cash flow for the third quarter totaled $46.7 billion, up from $37 billion in the prior year period. Overall, Microsoft closed the year with $32.1 billion in cash, substantially exceeding its short-term debt balance of $8.8 billion.

Finally, the recent pullback in the stock price, which is down 19% year-to-date (YTD), has brought valuations to more reasonable levels. The forward P/S multiple of 8.80 times remains above the sector median of 3.34 times, but the forward P/E ratio of 23.22 times and P/CF multiple of 17.11 times sit comfortably in line with sector medians of 24.61 times and 19.24 times, respectively.

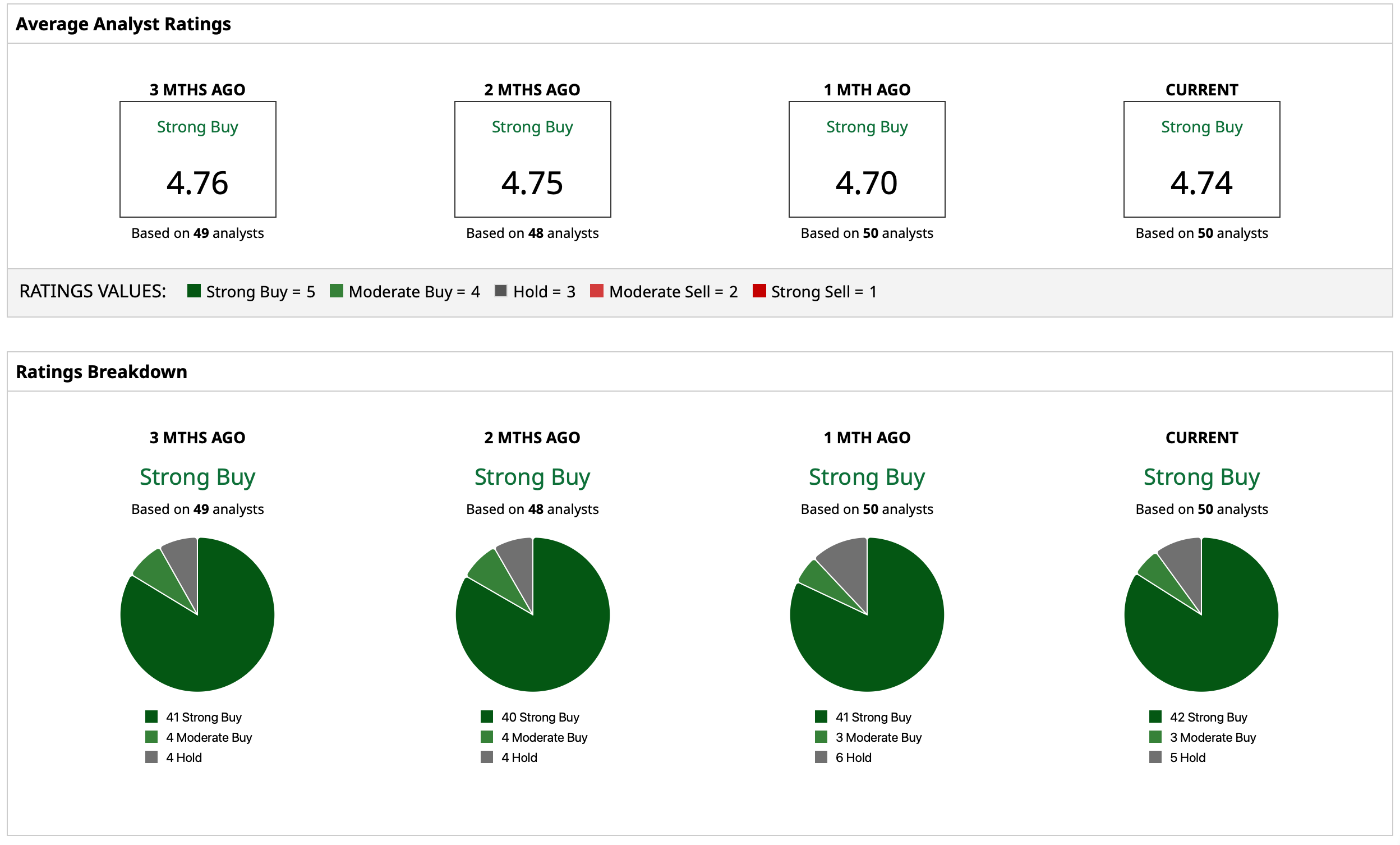

Analyst Opinion of MSFT Stock

Considering all this, analysts have assigned to MSFT stock an overall rating of “Strong Buy,” with a mean target price of $550.48, indicating an upside potential of about 40% from current levels. Out of 50 analysts covering the stock, 42 have a “Strong Buy” rating, three have a “Moderate Buy” rating, and five have a “Hold” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)