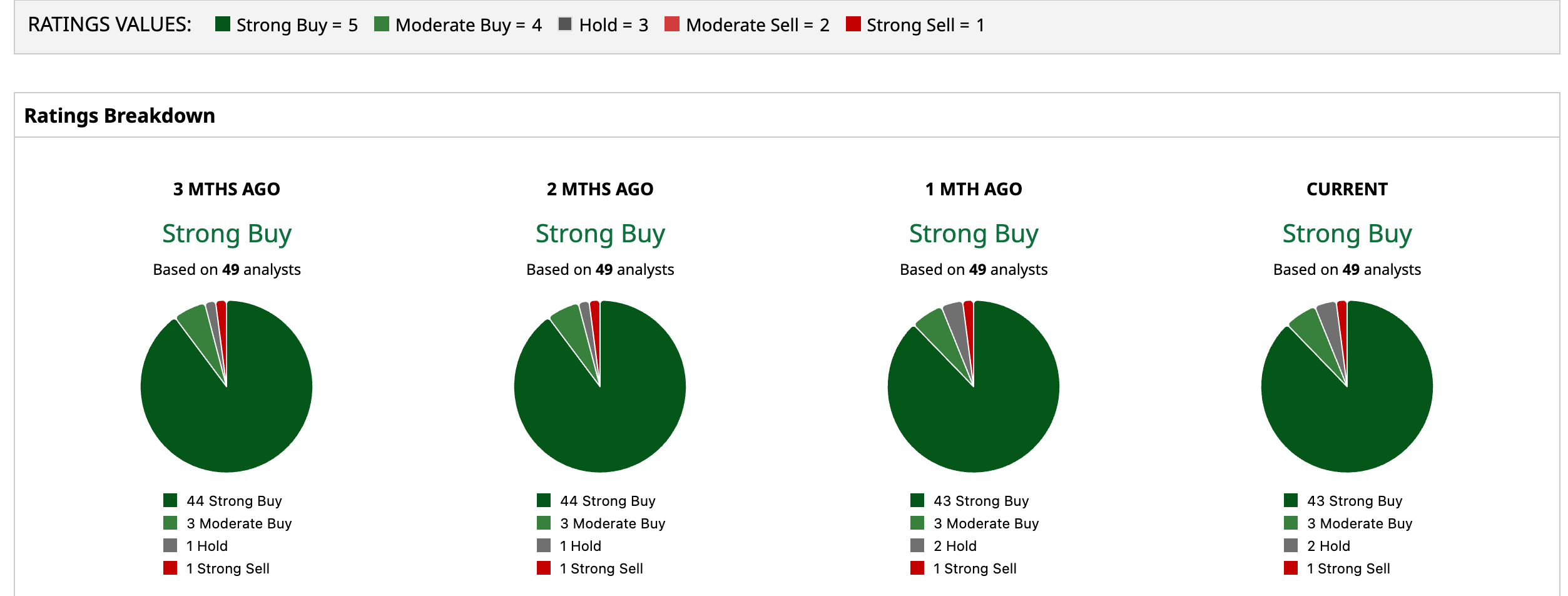

/Nvidia%20logo%20on%20phone%20screen%20with%20stock%20chart%20by%20xalien%20via%20Shutterstock.jpg)

The artificial intelligence boom has become something larger than a technology cycle. It has evolved into a capital spending race where every major cloud provider feels compelled to build faster than its rivals.

Amazon (AMZN), Microsoft (MSFT), Alphabet (GOOG) (GOOGL), and Meta Platforms (META) are collectively on pace to spend roughly $757 billion on capital expenditures in 2026, according to Goldman Sachs Group (GS), with much of that directed toward AI infrastructure. That spending has fueled explosive growth for chipmakers like Nvidia (NVDA), but cracks are beginning to appear.

Wall Street is now debating whether AI investment is keeping pace with actual business returns, or whether spending has become an end in itself.

AI Spending Has Become Self-Reinforcing

AI infrastructure spending now feeds on itself. Every new data center encourages competitors to build another. Each novel AI model requires more GPUs, networking equipment, and power generation.

That cycle has benefited Nvidia more than any other company. Its GPUs sit at the center of nearly every major AI deployment, making Nvidia the primary supplier to hyperscale cloud providers.

The problem is that this investment wave is becoming harder to finance internally. Many hyperscalers continue to generate enormous cash flows, but capital spending is rising even faster. Rather than relying solely on operating cash, companies have increasingly turned to debt markets and creative financing structures.

For example, Meta has begun using financing arrangements that move portions of infrastructure obligations off its balance sheet. While those commitments remain real economic liabilities, they become less visible in traditional debt metrics. Other technology companies have adopted similar approaches as AI projects become larger and more expensive.

None of this suggests balance sheets are under immediate stress. But it does highlight the increasingly expensive cost of the AI race.

Wall Street Is Sending Mixed Signals

Last month, Bain & Company published survey results showing AI investments have delivered weaker returns than many businesses expected. According to Bain, "AI investments are a circular bet, as ROI disappoints," with many companies falling well short of projected cost savings and productivity improvements.

That finding is significant because companies continue increasing AI budgets despite disappointing financial returns. Yet Goldman Sachs sees the opposite risk.

The investment bank recently argued consensus forecasts actually underestimate future AI spending. While analysts expect AI-related capital expenditures to rise from $757 billion in 2026 to roughly $920 billion in 2027, that represents only 22% year-over-year (YOY) growth, compared with an 84% increase this year.

Goldman believes spending could climb even higher if competitive pressures continue forcing hyperscalers to invest. The result is a market receiving two conflicting messages: spending should become more disciplined, yet spending forecasts may still prove too low.

Both scenarios create uncertainty. If companies continue overspending, debt burdens and financing costs rise. If they slow spending to match actual returns, AI suppliers immediately feel the impact.

Nvidia Sits at the Center of the Risk

No company is more exposed to that balancing act than Nvidia. The company's extraordinary growth has been driven by one simple fact: nearly every dollar of AI infrastructure eventually flows toward GPUs, networking equipment, or related hardware.

That concentration has made Nvidia one of the market's biggest winners. It also makes it the company with the most to lose if AI capital spending moderates. Investors are concerned. Its stock is up just 4.85% so far in 2026.

Granted, demand remains strong today. Large cloud providers continue announcing new data centers, sovereign AI initiatives are expanding globally, and enterprise adoption continues growing. But spending fueled by competitive pressure rather than measurable returns rarely accelerates forever.

If boards begin insisting that AI budgets reflect demonstrated business value instead of future expectations - as Bain calls for - Nvidia would likely experience that slowdown before most software companies because hardware purchases are the first large expense businesses can postpone.

Key Takeaway

In short, Nvidia remains one of the strongest businesses benefiting from the AI revolution, but investors should recognize where the biggest risk lies.

The AI boom has become a feedback loop where infrastructure spending encourages even more infrastructure spending. As long as that cycle continues, Nvidia should remain a major beneficiary.

Ultimately, however, Wall Street is beginning to ask whether AI investment has outpaced AI returns. Bain says many companies are not earning the productivity gains they expected, while Goldman Sachs argues spending forecasts may still be too conservative. Both cannot remain true indefinitely.

For Nvidia shareholders, that makes capital spending - not AI demand itself - the metric worth watching most closely over the next several quarters. If hyperscalers keep opening their checkbooks, Nvidia's growth story continues. If spending begins aligning with actual returns instead of competitive fear, Nvidia could feel the slowdown before anyone else.

On the date of publication, Rich Duprey did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Uber%20Technologies%20Inc%20logo%20outside%20offices-by%20Sundry%20Photography%20via%20iStock.jpg)

/Space%20Technology%20by%20Rini_%20com%20via%20Shutterstock.jpg)