/Meta%20Platforms%20by%20Primakov%20via%20Shutterstock.jpg)

Meta Platforms (META) is once again testing investor patience as it doubles down on artificial intelligence (AI) infrastructure amid growing signs of execution stumbles and a punishing stock reaction.

The company behind Facebook, Instagram, and WhatsApp has made no secret of its ambitions to lead the next wave of AI-powered experiences. Yet with capital expenditures exploding and flagship models slipping, the market is starting to ask whether this spending spree is strategic foresight or a reflexive escalation that risks echoing past overcommitments.

Surging Investment in AI Infrastructure

The latest escalation involves Meta’s massive AI data-center project in El Paso, Texas. The company originally committed $1.5 billion to the site last fall. Now that figure has surged to $10 billion, reflecting an aggressive push to secure computing power for its AI ambitions. This single facility underscores a company-wide capex ramp-up that Meta outlined earlier this year — full-year 2026 guidance of $115 billion to $135 billion, with the overwhelming majority earmarked for AI data centers and custom silicon.

That scale aligns with a broader industry frenzy. Major hyperscalers have collectively pledged more than $630 billion in AI infrastructure spending this year alone, a sum that highlights just how high the stakes have become.

Market Delivers a Harsh Verdict

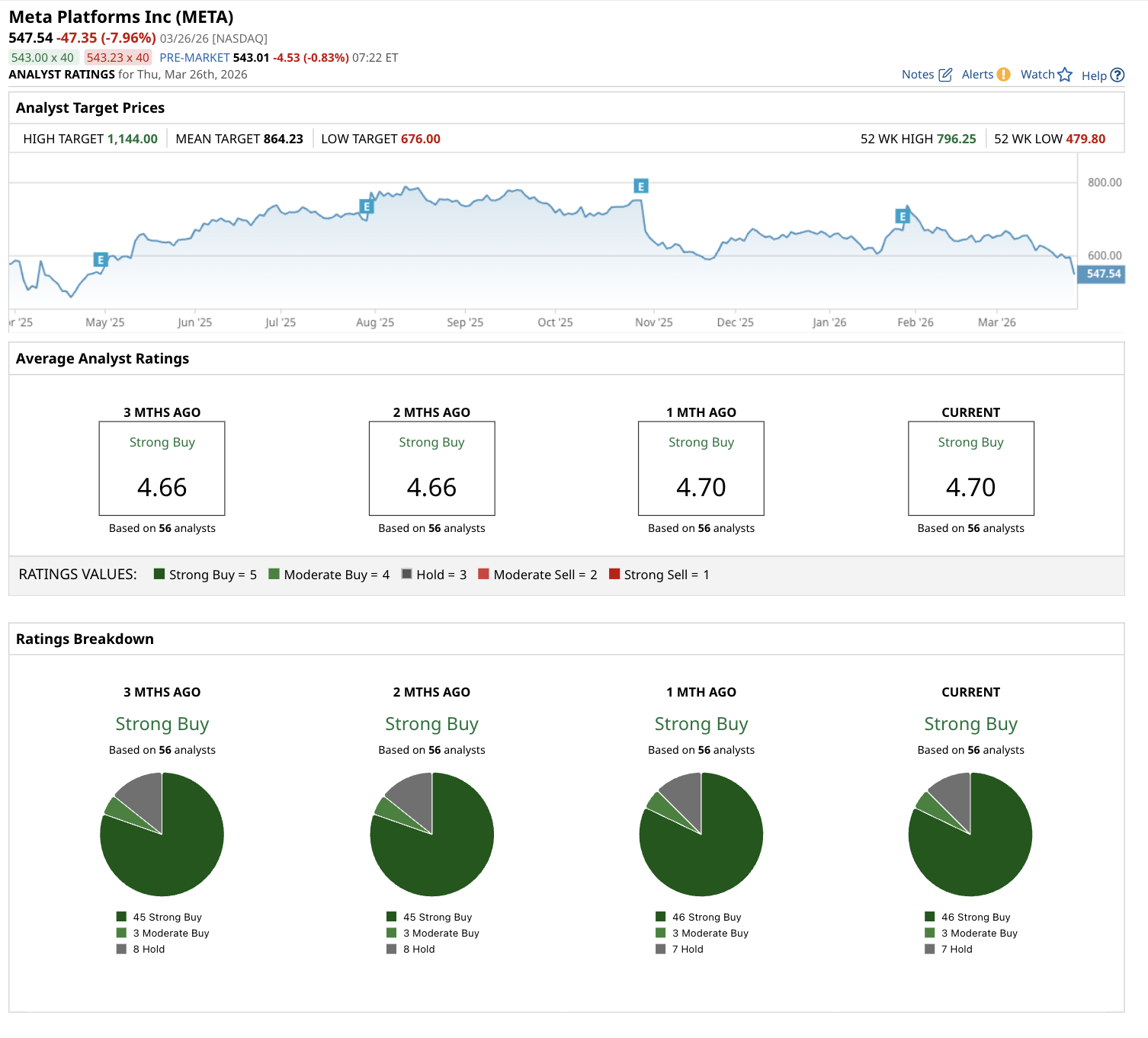

The market delivered its verdict quickly. Meta shares plunged roughly 8% on March 26, closing at their lowest level since last April and erasing billions in market value in a single session. META stock is now down approximately 20% year-to-date (YTD), underperforming the broader market and many of its Big Tech peers.

Compounding the pressure are clear setbacks on the AI product front. Last year’s Llama 4 release underwhelmed developers and analysts alike, falling short on reasoning capabilities and overall innovation relative to competitors. Now Meta has pushed back the debut of its next major model, internally known as Avocado, from an expected March launch to at least May.

The delay stems from disappointing results on internal benchmarks for reasoning, coding, and writing — areas where the model still trails the latest offerings from OpenAI, Anthropic, and Alphabet (GOOGL). Insiders say the company has even floated the idea of temporarily licensing rival technology to close the gap while it iterates.

These stumbles leave Meta at real risk of falling further behind in the AI race. Rather than stepping back to refine its approach, the company appears to be responding by throwing even more capital at the problem. At the same time, new rounds of layoffs are rippling through the organization, with reports suggesting hundreds of roles could be affected across teams. The contrast is striking. Meta is investing tens of billions in automation and efficiency tools while simultaneously trimming its workforce to help absorb the ballooning infrastructure costs.

Echoes of the Metaverse Misstep

The situation carries uncomfortable echoes of Meta’s earlier metaverse spending binge. Under the rebranding push led by CEO Mark Zuckerberg, the company poured billions into virtual worlds and hardware through its Reality Labs division. Cumulative losses exceeded $80 billion in recent years, with minimal revenue or user traction to show for it. Today, much of that pure metaverse vision has been quietly shelved or redirected toward more practical AI-powered wearables and advertising tools. The episode stands as a reminder of what can happen when visionary bets outpace measurable returns.

Despite the recent turbulence, Wall Street remains broadly constructive. Analysts tracking META stock maintain a consensus “Strong Buy” rating, based on 56 firms with coverage. The mean 12-month price target sits at $864.23, implying 64% potential upside from current levels. The range of targets spans from $676 on the low end to as high as $1,144, reflecting confidence in Meta’s core advertising engine even as AI investments dominate the narrative.

The Bottom Line

Meta Platforms exhibits classic signs of addiction in its AI spending trajectory — needing ever-larger doses of capital to chase the same competitive high as rivals pull ahead; allowing the pursuit to consume an increasing share of its strategic focus and resources; and, in some interpretations, leaning on future cash flows or balance sheet strength to fund the habit amid mounting infrastructure commitments. Downplaying challenges — such as model delays and execution hiccups — while pressing forward with bigger bets fits the pattern of refusing to fully admit the severity or pivot decisively.

That said, Meta still looks like a long-term winner. Its core social platforms generate enormous value, providing a stable base few competitors can match. Yet as AI spending continues to escalate across the industry — with hyperscalers collectively burning through hundreds of billions of dollars — the moment for an “intervention” may be approaching. Whether through market discipline, internal discipline, or clearer returns on investment, Meta and its peers will eventually need to demonstrate that this massive outlay translates into sustainable advantages rather than diminishing returns.

For now, the company is all-in on AI, but investors need to see whether it yields lasting rewards or another expensive lesson.

On the date of publication, Rich Duprey did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Data%20Center%20by%20Caureem%20via%20Shutterstock%20(2).jpg)

/A%20corporate%20sign%20for%20SK%20Hynix%20by%20Tada%20Images%20via%20Adobe%20Stock.jpeg)