Brown & Brown, Inc. (BRO) is a leading insurance brokerage and risk management services provider offering property, casualty, employee benefits, and specialty programs to commercial, public, and individual clients. Headquartered in Daytona Beach, Florida, it operates across the U.S. and select international markets. The company has a market capitalization of $23.73 billion.

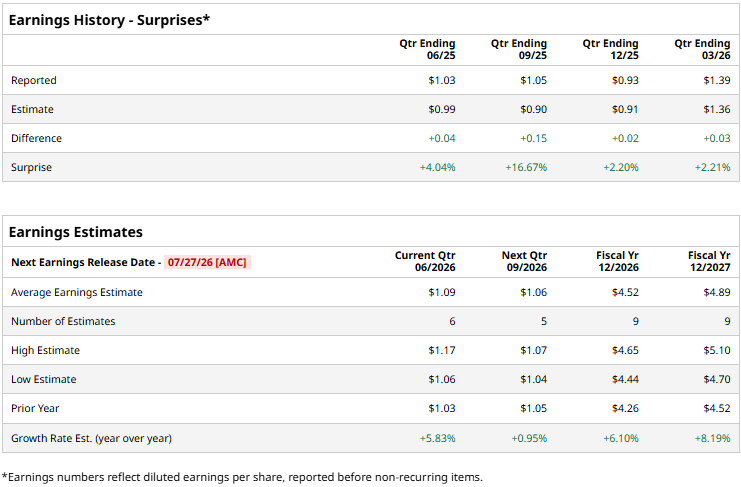

Brown & Brown is set to report its second-quarter results for fiscal 2026 on July 27 after the market closes. Ahead of the results, Wall Street analysts expect the company’s profit to increase 5.8% year-over-year (YOY) to $1.09 per diluted share for Q2. Brown & Brown has a solid record of earnings surprises, exceeding estimates in all four trailing quarters. Analysts expect the company’s bottom line to rise by 6.1% to $4.52 in the current fiscal year. For the fiscal year 2027, Wall Street analysts expect Brown & Brown’s diluted EPS to be $4.89, up 8.2% YOY.

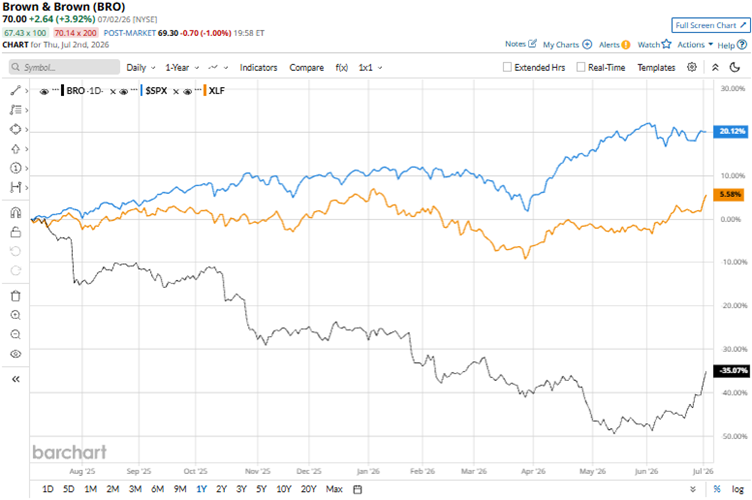

Sector rotation has pressured defensive financials and insurance brokers as investors have shifted toward AI and tech names, while higher, more volatile interest rates have created uncertainty around insurance pricing cycles. Over the past 52 weeks, the stock has declined 35.1%, and 12.2% year-to-date (YTD). On the other hand, the broader S&P 500 Index ($SPX) has increased by 20.2% and 9.3% over the same periods, respectively. Therefore, the stock has underperformed the broader market.

We now compare Brown & Brown’s performance with that of its sector. The State Street Financial Select Sector SPDR ETF (XLF) has increased 5.7% over the past 52 weeks and 1.6% YTD. Therefore, Brown & Brown has underperformed its sector over these periods.

In the first quarter, Brown & Brown reported better-than-expected results as its total revenue increased 35.4% YOY to $1.90 billion. However, its organic revenues remained flat YOY at $1.35 billion. Its adjusted EPS grew by 7.8% from the prior-year period to $1.39. Despite this, the stock dropped 4.5% intraday on Apr. 28 after the results release.

Wall Street analysts have been bullish about Brown & Brown’s future. Among the 22 analysts covering the stock, the consensus rating is “Moderate Buy.” The rating configuration is more bullish than it was two months ago, with four “Strong Buy” ratings now, up from two. The ratings are rounded off by one “Moderate Buy” and 17 “Holds.” The mean price target of $74.61 implies a 6.6% upside from current levels, while the Street-high price target of $117 implies 67.1% upside.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)

/Doctor%20stacking%20healthcare%20medical%20insurance%20icons%20by%20Dilok%20via%20Adobe%20Stock.jpeg)