/Global%20Network.jpg)

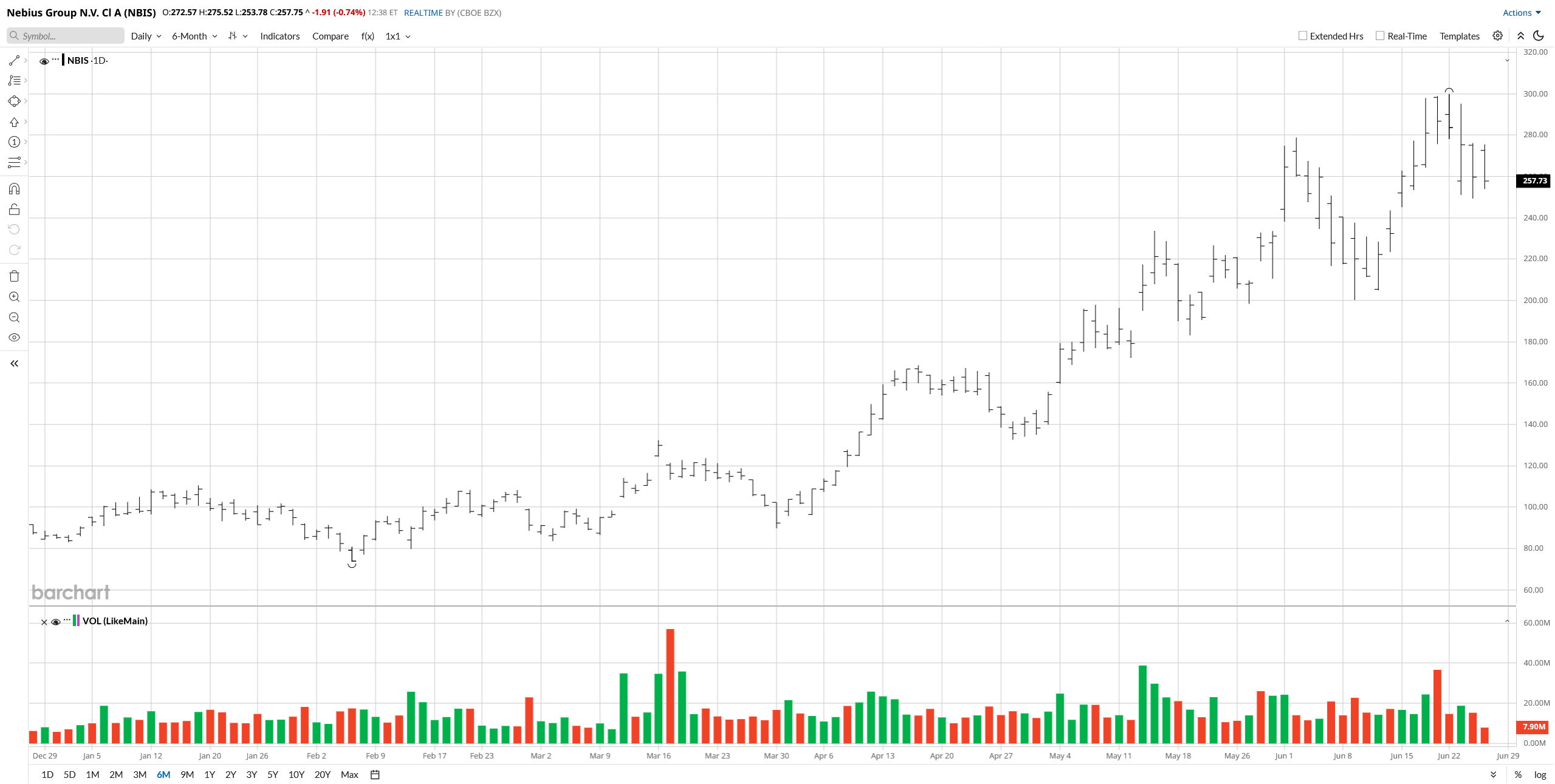

The recent price declines of Nvidia's (NVDA) B200 AI chips, spurred by rapidly increasing competition in the AI-chip space, bode poorly for Nebius' (NBIS) outlook. Meanwhile, over the longer term, the firm could be hurt by the advent of space-based data centers, while the stock's valuation continues to be extremely high.

In light of these points, I suggest that investors consider selling Nebius' shares.

About Nebius

The company's graphics processing unit (GPU) chips and other hardware, obtained from partners such as Nvidia and based in data centers, are used by major hyperscalers, including Microsoft (MSFT) and Meta Platforms (META), to develop AI. Nebius also has other customers in several different sectors, including robotics, healthcare, finance, and government. Founder Arkady Volozh serves as the CEO of the company, which has also moved into launching and servicing supercomputers. Although headquartered in Amsterdam, Nebius has offices in Israel and the U.S. Volozh holds Israeli citizenship and has called himself “an Israeli businessman.”

Price Declines for Nvidia's Chips Amid Rising Competition Could Foreshadow a Negative Catalyst for Nebius

As I noted in a recent column, “The prices for Nvidia's (NVDA) B200 AI chips, which were released in the second quarter of 2024, tumbled from $6.11 per hour on May 30 to $4.22 by June 21.” The drop, I pointed out, indicates that "Nvidia's rising competition is depressing the overall value of its chips."

Indeed, with Alphabet (GOOG) (GOOGL) selling AI chips, Amazon (AMZN) looking to do the same, Nebius and Coreweave (CRWV) constantly renting out more of Nvidia's chips, and the chip sales of Marvell (MRVL), Nvidia, and Broadcom (AVGO) all rapidly increasing, the market is becoming increasingly saturated. And prices are apparently dropping due to the latter trend. Of course, that trend is likely to negatively impact Nebius. Specifically, if the prices that it can charge for leasing its AI chips drop sharply, its top-and-bottom-line growth is likely to fall significantly.

Space-Based Data Centers and NBIS Stock's Elevated Valuation

Alphabet seems to believe that space-based data centers may very well be feasible. The tech giant is already, as I reported in a prior article, working with Planet Labs (PL) in order to explore placing its AI chips in space. And “The Wall Street Journal reported that (GOOG is) negotiating with Elon Musk’s SpaceX (SPCX) about placing data centers in space. Additionally, GOOG is also holding talks with additional satellite-launch firms.”

Further, Planet Labs CEO Will Marshall stated that, "It’s very clear to me that (space-based data centers are) going to make sense fiscally and from an engineering standpoint." Finally, Jeff Bezos' Blue Origin is also seriously looking at space-based data centers, and many say that such data centers will be meaningfully cheaper than Earth-based ones.

But today's chips won't be able to be used in space, according to Dr. Paul Struhsaker, a former VP at AMD (AMD). Instead, “custom silicon” will be needed in the final frontier, he reported. That creates many unknowns for Nebius and the investors who want to hold NBIS stock for the long term.

For example, if space-based data centers become dominant, will Nebius be able to obtain such data centers as easily as it acquires terrestrial ones now? Will it get this “custom silicon” as easily as it gets Nvidia's chips now? Could its margins on the new chips be much lower than they are on Nvidia's current chips? Could Google and Amazon, which are likely to partner with Blue Origin, dominate the space-based data center market, utilize only their own chips there, and refuse to sell any of them to Nebius?

There are just too many unknowns around these questions to make NBIS stock a viable investment right now.

On the valuation front, the shares are changing hands at a forward price-sales ratio of 19.4x, based on analysts' average 2026 sales estimate. Given its multiple potential negative catalysts and the fact that its operating income in the first quarter came in at -$128 million, the shares are very expensive, and investors should just avoid NBIS at this time.

On the date of publication, Larry Ramer had a position in: AMZN , AMZU , MRVL . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Data%20codes%20through%20eyeglasses%20by%20Kevin%20Ku%20via%20Pexels.jpg)

/Space/Rocket%20launch%20streak%20by%20Alones%20via%20Shutterstock.jpg)