/Alphabet%20Inc_%20and%20Google%20logos%20seen%20displayed%20on%20a%20smartphone%20by%20IgorGolovniov%20via%20Shutterstock.jpg)

Tech giant Alphabet (GOOG) (GOOGL), the parent company of Google, could soon face intensified competition in the artificial intelligence (AI) infrastructure market. The latest challenge comes from e-commerce giant Amazon (AMZN), which has unveiled plans to sell its custom AI chips to external companies with data center requirements. Amazon's AI chief recently told Bloomberg that discussions with potential customers are already underway, highlighting the growing demand for AI infrastructure.

The company first launched Trainium in 2021 and has since rolled out Trainium2 and the currently available Trainium3. Now, it is working on Trainium4, Amazon’s most powerful AI chip yet. The upcoming processor is expected to offer around six times the performance in FP4 workloads, four times the memory bandwidth, and nearly double the memory capacity of Trainium3, making it a major step forward in Amazon's AI hardware strategy.

Importantly, Trainium4 will go head-to-head with Google's Tensor Processing Unit (TPU), the company's custom-designed application-specific integrated circuit (ASIC) built to accelerate artificial intelligence and machine learning workloads. Google's TPUs have already been battling intense competition from Nvidia's (NVDA) dominant data center GPUs. Now, with Amazon accelerating its AI chip ambitions, the competitive landscape is becoming even more crowded.

Could this emerging challenge put additional pressure on Google's AI business, or does Google still possess the scale, technology, and ecosystem advantages needed to maintain its leadership position in the rapidly evolving AI market?

About Google Stock

Founded in 1998 by Larry Page and Sergey Brin while they were Ph.D. students at Stanford University, Google has evolved from a simple search engine into one of the world's most influential technology companies. Headquartered in Mountain View, California, the company serves billions of users worldwide. Best known for its dominant search engine, Google has built a vast ecosystem that spans digital advertising, cloud computing, artificial intelligence, consumer hardware, and online video through YouTube.

Its operations are primarily organized into Google Services, which include Search, YouTube, Android, Chrome, and hardware products, and Google Cloud, which provides infrastructure and software solutions to businesses worldwide. By continuously innovating across some of the fastest-growing areas of technology, Google has cemented its position as one of the world's most valuable and influential companies.

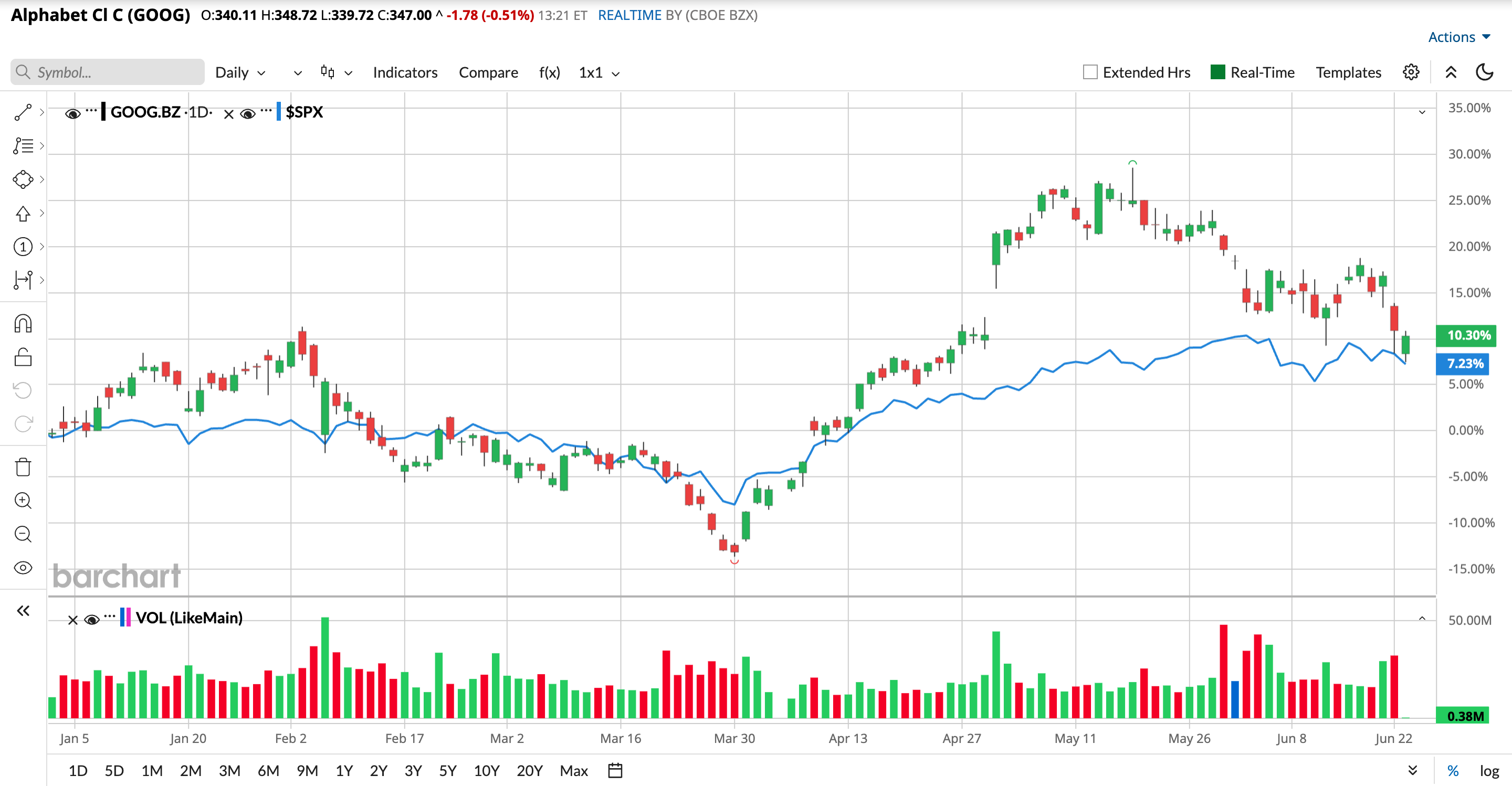

Even as competitive pressures mount, Google remains a Wall Street powerhouse. With a market capitalization of roughly $4.225 trillion, the tech giant ranks among the world's most valuable companies. Its stock performance has been equally impressive, with Class C shares surging 109% over the past year, dramatically outperforming the S&P 500 Index ($SPX) 22.85% gain during the same stretch.

While regulatory challenges and broader tech-sector volatility have weighed on sentiment this year, Google has still delivered an 10.56% year-to-date (YTD) return, ahead of the market's 8.13% advance. Although the stock has retreated 14.14% from its record high of $404.47 reached on May 18, its long-term momentum remains firmly intact.

Inside Google’s Q1 Earnings Results

Google delivered a blockbuster fiscal 2026 first-quarter report on April 29, crushing Wall Street's expectations on both the top and bottom lines as surging demand for cloud and AI services continued to fuel extraordinary growth. Consolidated revenue jumped 22% year-over-year (YOY) to $109.9 billion, marking the company's 11th consecutive quarter of double-digit growth and comfortably surpassing analysts' $107 billion estimate.

The earnings story was even more impressive. Powered by significant operating leverage, net income soared 81% from the year-ago period to $62.6 billion. Earnings per share (EPS) came in at $5.11, nearly double the consensus forecast of $2.67. Also, profitability improved meaningfully, with Google’s consolidated operating margin expanding to 36% from 34% a year earlier, driven by a 30% increase in operating income. Investors cheered the exceptional results, sending the stock nearly 10% higher in the session following the release.

The standout performer was Google Cloud, which surpassed the $20 billion revenue milestone for the first time in its history. Revenue from the division surged 63% YOY to $20.03 billion, fueled by strong adoption of Google Cloud Platform (GCP) across enterprise AI solutions, enterprise AI infrastructure, and core GCP services. Management noted that AI solutions were the largest contributor to cloud growth during the quarter, supported by robust demand for the company's industry-leading models, including Gemini 3.

Underscoring the scale of future demand, Google Cloud's total backlog nearly doubled sequentially to an eye-popping $462 billion. At the same time, Google's core Services segment continued to fire on all cylinders. Revenue from the division rose 16% YOY to $89.6 billion. Google Search and related revenues climbed 19% to $60.4 billion, demonstrating that AI-powered features such as "AI Overviews" and "AI Mode" are enhancing user engagement rather than cannibalizing traditional search activity.

YouTube also delivered solid results, with advertising revenue increasing 11% YOY to $9.9 billion. Management highlighted that the quarter was the strongest ever for Google's consumer AI subscription offerings, driven primarily by the Gemini app. Total paid subscriptions across the company's ecosystem have now reached 350 million, with YouTube and Google One serving as the primary growth engines.

Meanwhile, Gemini Enterprise continues to gain traction, recording 40% quarter-over-quarter growth in paid monthly active users. The only notable concern in an otherwise stellar quarter was the enormous cost of maintaining Google’s leadership in the AI race. Capital expenditures more than doubled YOY to $35.7 billion as the company aggressively expanded its data center footprint and invested heavily in custom AI silicon infrastructure.

The spending spree significantly pressured cash generation, causing free cash flow to fall 47% to $10.1 billion. Looking ahead, CFO Anat Ashkenazi signaled that AI-related investments are set to accelerate further, raising full-year 2026 capital expenditure guidance to between $180 billion and $190 billion, up from the prior range of $175 billion to $185 billion, while warning that spending in 2027 is expected to increase significantly once again.

How Do Analysts View Google Stock?

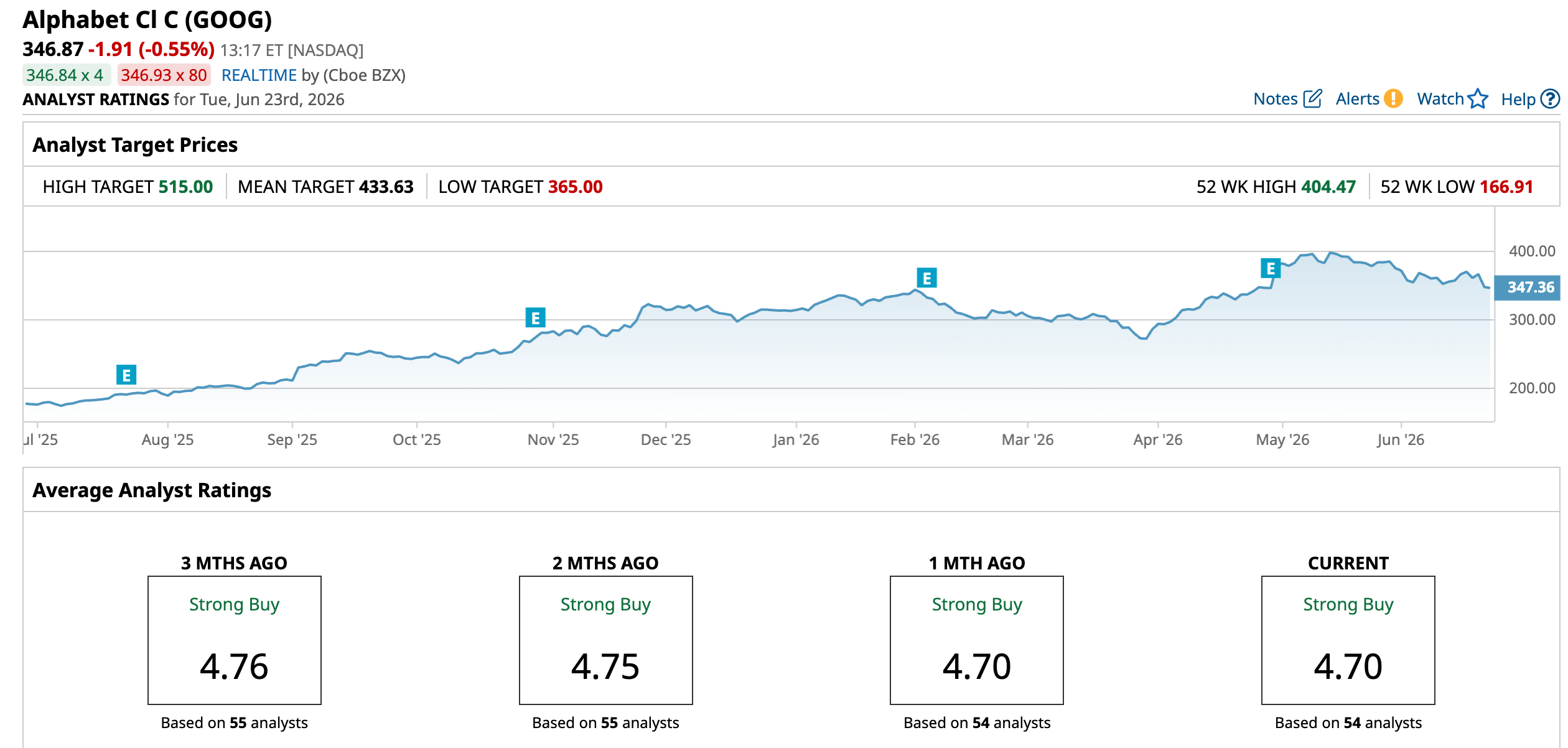

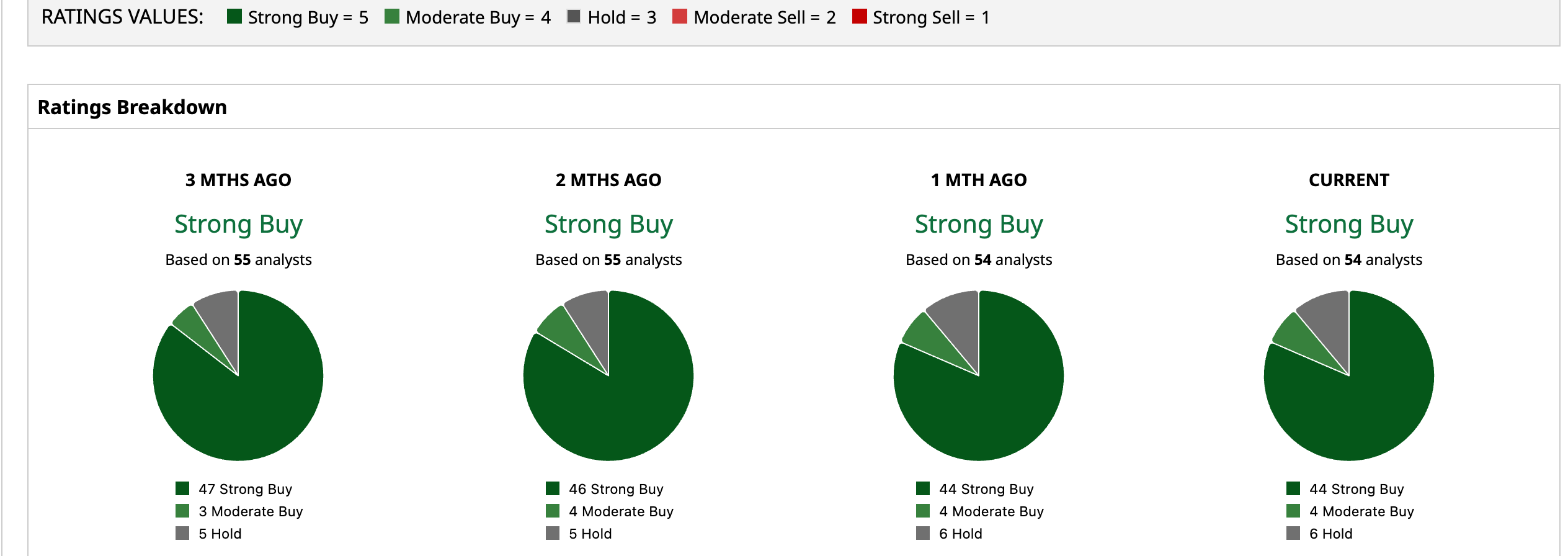

Wall Street remains firmly in Google's corner. The stock currently carries a consensus “Strong Buy” rating, reflecting broad confidence in the company's long-term growth prospects. Among the 54 analysts covering the stock, 44 recommend “Strong Buy,” four rate it “Moderate Buy,” and only six suggest “Hold.”

Analysts also see meaningful upside ahead, with the average price target of $433.63 implying a potential gain of 25% from current levels. Even more notably, the Street-high target of $515 points to a possible 48.5% rally, underscoring continued optimism about Google's ability to capitalize on the AI revolution and sustain its market leadership.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)