Telecommunications giant Verizon Communications (VZ) is rolling out an aggressive customer-retention strategy as competition in the wireless industry heats up, and carriers battle to keep subscribers from switching providers. The company recently introduced a sweeping set of loyalty-focused initiatives, betting that simplified plans, cashback rewards, and exclusive perks can help strengthen customer relationships in an increasingly crowded market.

The move reflects Verizon's broader effort to make its services easier to understand and more rewarding to use. At the center of the overhaul is Verizon Simplicity, a new wireless plan that eliminates network tiers and gives every customer access to the same 5G experience. The company has also launched Verizon One, a bundled offering that combines mobility and home services into a single bill for a more streamlined experience.

To further boost loyalty, Verizon has scrapped upgrade and activation fees for both new and existing customers through its Verizon Loyalty program. Subscribers can also earn 3% back in Verizon Dollars each month to spend on a range of products and services. Adding a layer of excitement, the company is offering weekly sweepstakes featuring prizes ranging from dining vouchers and Amazon (AMZN) gift cards to an NFL trip to Australia and even the chance to attend a FIFA World Cup match in New York City with soccer icon David Beckham.

In addition, customers are being treated to weekly "daily drops" through the Verizon app, which include perks such as complimentary Starbucks (SBUX) coffee, a free hour at Topgolf, and other promotional rewards. The latest initiatives come as Verizon seeks new ways to differentiate itself in a market where the nation's three major carriers offer increasingly similar network performance. With coverage and service quality becoming less of a distinguishing factor, telecom companies are leaning more heavily on pricing flexibility, bundled offerings, loyalty programs, and lifestyle perks to attract and retain customers.

Whether freebies and rewards will be enough to meaningfully slow customer churn remains an open question. However, Verizon's latest push underscores the growing pressure facing telecom providers to compete beyond network quality alone. Combined with its long-standing commitment to returning capital through dividends and share repurchases, the company's customer-first strategy could give investors another reason to keep Verizon on their radar.

About Verizon Stock

A pillar of modern communications, Verizon Communications sits at the heart of how millions of people connect, work, and consume content every day. Through its vast wireless network, broadband and fiber offerings, and enterprise solutions, the telecom giant provides the mobility, connectivity, and security that businesses and consumers increasingly depend on in a digital-first world. Its reach extends across organizations of all sizes, including nearly every Fortune 500 company.

Since its formation in 2000 and headquarters establishment in New York City, Verizon has grown into one of the world's largest communications providers, serving customers across multiple countries while maintaining a critical role in global communications infrastructure. The company's scale remains formidable, with approximately $138.2 billion in revenue generated in 2025 alone. Looking ahead, Verizon is positioning itself for the next phase of technological evolution by embedding artificial intelligence more deeply into its operations.

The company is leveraging artificial intelligence (AI) to enhance network performance, improve operational efficiency, and elevate customer experiences, while combining those capabilities with its expanding 5G platform to support increasingly data-intensive applications. Yet despite these technological advances and its recent push to strengthen customer retention, the stock has largely moved sideways, suggesting the market has yet to fully recognize the company's transformation efforts.

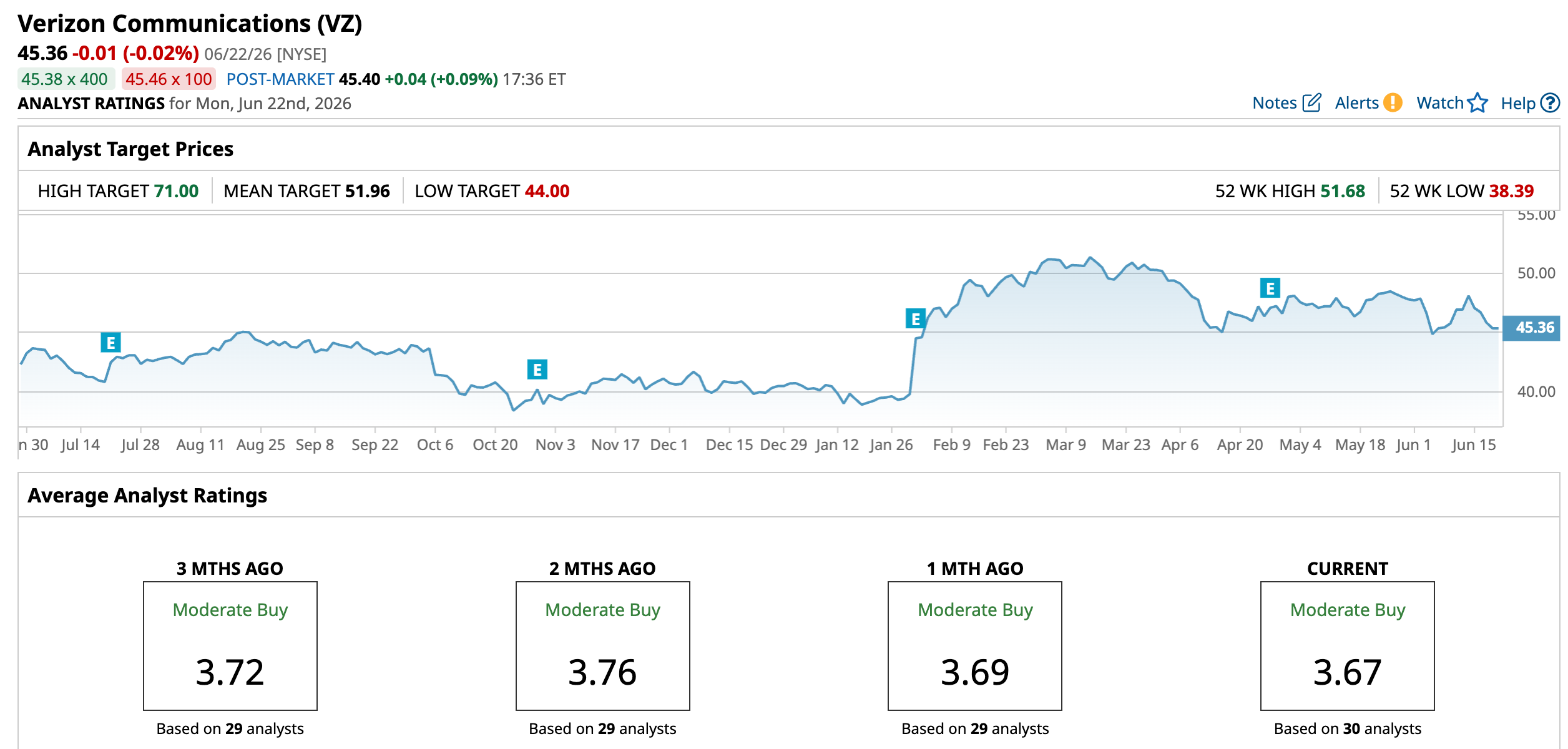

With a market capitalization of approximately $189.45 billion, Verizon remains one of the largest names in the telecom space. The stock has gained 11.37% year-to-date (YTD) in 2026, outperforming the broader S&P 500 Index ($SPX), which has advanced 9.16% over the same period. Shares surged to a 52-week high of $51.68 on March 24 before retreating roughly 12.2% from that peak, leaving investors to consider whether Verizon's operational momentum and strategic transformation are being fully appreciated by the market.

Verizon's 6.2% Yield Remains a Major Draw for Investors

Beyond its efforts to attract and retain customers, Verizon has remained a favorite among income investors thanks to its long-standing commitment to shareholder returns. The telecom giant has increased its dividend for 21 consecutive years, underscoring the resilience of its cash-generating business model and its focus on delivering value to investors.

Earlier this month, Verizon announced a quarterly dividend of $0.7075 per share, payable on Aug. 3 to shareholders. At current share prices, the company's forward annualized dividend of $2.83 per share equates to an attractive yield of approximately 6.24%, making the stock particularly appealing for investors seeking a combination of income, stability, and dependable cash returns.

Management has made clear that returning capital to shareholders remains a key priority even as the company undergoes a broader transformation. Verizon's leadership views its dividend policy as a reflection of both its financial strength and disciplined approach to capital allocation. That commitment is backed by substantial cash distributions, with the company paying out approximately $11.5 billion in dividends during 2025 alone.

For investors searching for reliable income in an uncertain market environment, Verizon's combination of a high yield, two decades of dividend growth, and significant cash-return program continues to stand out.

Verizon's Q1 Earnings Snapshot

Verizon's first-quarter fiscal 2026 results offered investors plenty to like, proving that strong execution can outweigh a few headline misses. When the telecom giant reported earnings on April 27, the market looked past a modest revenue shortfall and instead focused on robust earnings growth, improving subscriber trends, and a more optimistic outlook for the year ahead.

Revenue for the quarter increased 2.9% year-over-year (YOY) to $34.4 billion. While that marked healthy growth, it came in slightly below analysts' expectations of $35.03 billion. The miss was primarily attributed to Verizon's decision to scale back aggressive promotional activity and the impact of customer credits issued following a major network outage in January, which reduced wireless service revenue by approximately 80 basis points.

Despite those headwinds, Verizon's profitability painted a much stronger picture. Adjusted earnings per share climbed 7.6% from the prior-year period to $1.28, surpassing the consensus estimate of $1.22 and delivering the company's strongest quarterly earnings growth since 2021. Investors welcomed the performance, sending the stock 1.55% higher following the announcement.

Perhaps the most encouraging development came from Verizon's wireless business. The company reported 55,000 postpaid phone net additions during the quarter, an unexpected gain and its first positive first-quarter result in this category since 2013. The milestone suggested that Verizon's efforts to improve customer acquisition and retention may be beginning to gain traction.

Growth was equally impressive across the company's broadband operations. Verizon added a total of 341,000 broadband subscribers in the quarter, including 214,000 fixed wireless access net additions and 127,000 fiber broadband additions. As a result, the company now serves approximately 16.8 million fixed wireless access and fiber broadband connections, highlighting the continued expansion of its next-generation connectivity platform.

The quarter also showcased Verizon's improving financial flexibility. Since completing its acquisition of Frontier, the company has already paid down roughly half of the acquired debt and expects to eliminate substantially all of the remaining balance before year-end. Meanwhile, Verizon returned significant capital to shareholders, repurchasing $2.5 billion worth of stock during the quarter and remaining on pace to exceed its full-year buyback target of at least $3 billion.

Cash generation remained healthy as well. Free cash flow rose 4% YOY to $3.8 billion, compared to $3.6 billion in the prior-year quarter, providing additional support for the company's investment plans and shareholder-return initiatives.

Buoyed by its strong start to the year, Verizon raised its full-year 2026 guidance. The company now expects adjusted EPS growth of 5% to 6%, an improvement from its previous forecast of 4% to 5%. Management also expects postpaid phone net additions to finish in the upper half of its targeted range of 750,000 to 1 million additions, a level that would represent roughly two to three times the company's 2025 performance.

How Do Analysts View Verizon Stock?

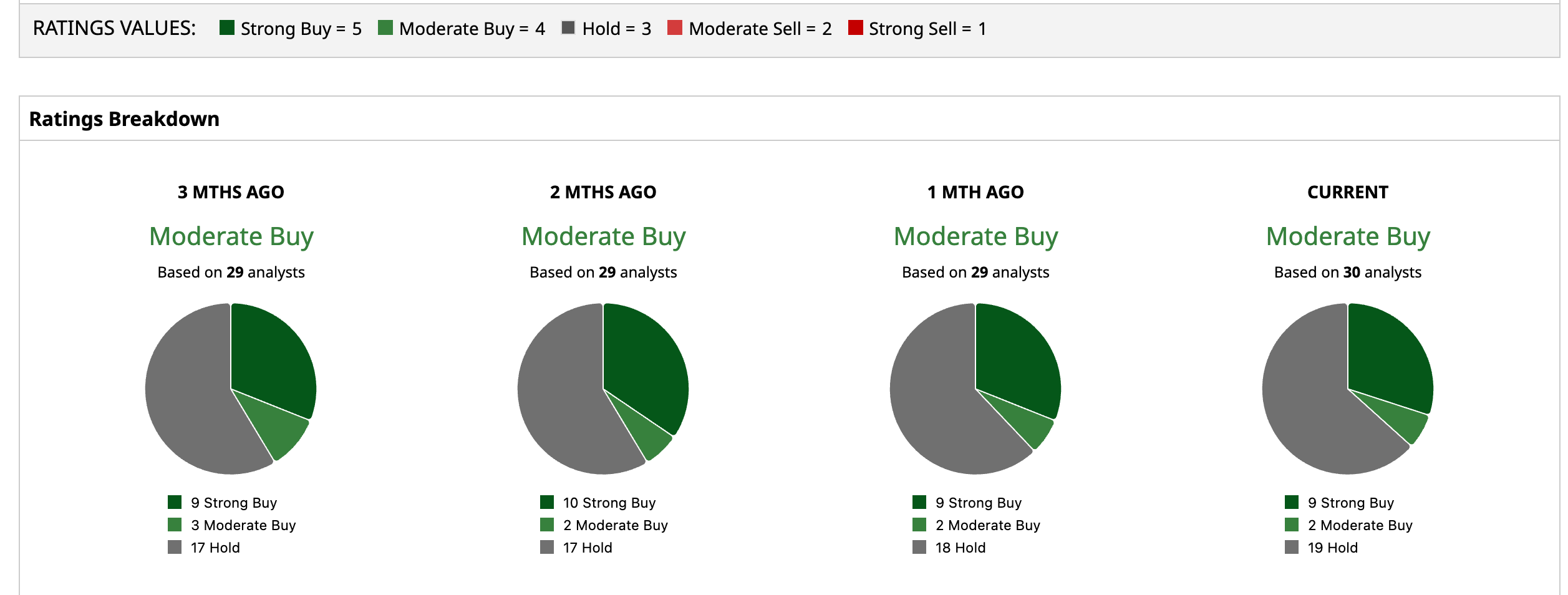

Wall Street isn't ready to fully embrace Verizon just yet, but analysts are becoming increasingly constructive on the telecom giant's prospects. The stock currently carries a consensus "Moderate Buy" rating, reflecting a mix of optimism and caution as investors assess whether the company's operational improvements can translate into sustained growth. Among the 30 analysts covering Verizon, nine have assigned "Strong Buy" ratings, while two recommend "Moderate Buy." The remaining 19 analysts maintain "Hold" ratings, highlighting a wait-and-see approach as the company continues executing its transformation strategy.

Even so, analysts see meaningful upside potential ahead. The average price target of $51.96 suggests the stock could climb approximately 14.55% from current levels. For investors willing to bet on a stronger turnaround, the most bullish target on Wall Street stands at $71, implying a potential gain of 56.5% if Verizon continues delivering on its growth.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Accenture%20plc%20buiding%20with%20logo-by%20JHVEPhoto%20via%20iStock.jpg)