Valued at a market cap of $11 billion. Wynn Resorts, Limited (WYNN) is a global hospitality and gaming company that develops, owns, and operates luxury resorts featuring hotels, casinos, fine dining, retail, entertainment, and convention facilities. Headquartered in Las Vegas, Nevada, the company serves customers through its properties in Macau, Las Vegas, and the United Arab Emirates.

Companies worth $10 billion or more are typically classified as “large-cap stocks,” and WYNN fits the label perfectly. Its portfolio includes iconic destinations such as Wynn Las Vegas, Encore Las Vegas, Wynn Palace, and Wynn Macau. In addition to its established properties, Wynn Resorts is expanding internationally with the development of Wynn Al Marjan Island in Ras Al Khaimah, which is expected to become the UAE's first integrated gaming resort.

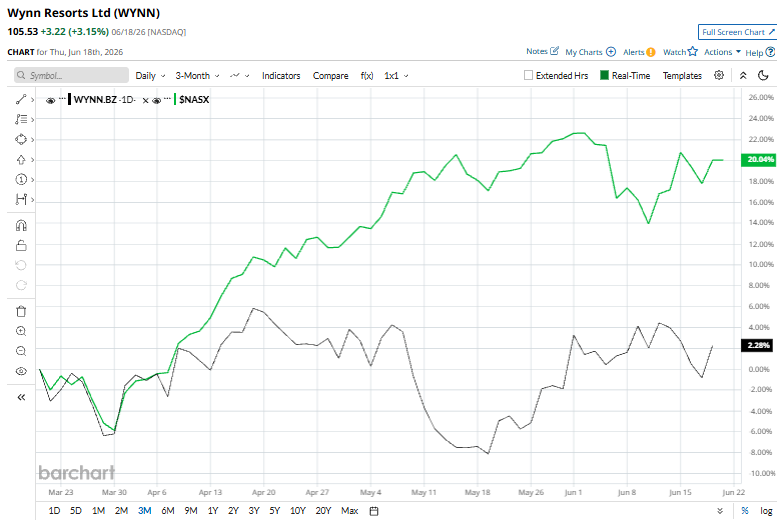

However, this resort and casinos company has dipped 21.7% from its 52-week high of $134.72, reached on Dec. 1, 2025. Shares of WYNN have surged 3.9% over the past three months, trailing the Nasdaq Composite ($NASX), which has gained 20% over the same time frame.

Moreover, on a YTD basis, shares of WYNN are down 12.3%, compared to NASX’s 14.1% rise. In the longer term, WYNN has rallied 21.4% over the past 52 weeks, trailing the index’s 35.7% uptick over the same time frame.

While WYNN has been trading below its 200-day moving average since mid-February, it climbed above its 50-day moving average at the start of this month.

Wynn Resorts' stock has lagged the broader market over the past year due to concerns about softer demand in its Las Vegas operations, weaker gaming hold rates in Macau, and earnings results that fell short of analysts' expectations. Investors have also been cautious about the company's high debt levels and its heavy reliance on a limited number of properties, particularly in Macau, which exposes it to regional economic and regulatory risks.

WYNN has surpassed its rival, Las Vegas Sands Corp. (LVS), which rallied 16.6% over the past 52 weeks and dipped 25.2% in 2026.

Despite WYNN’s recent underperformance, analysts remain highly optimistic about its prospects. The stock has a consensus rating of "Strong Buy” from the 18 analysts covering it, and the mean price target of $136.83 suggests a 29.7% premium to its current price levels.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Accenture%20plc%20buiding%20with%20logo-by%20JHVEPhoto%20via%20iStock.jpg)