/Fifth%20Third%20Bancorp%20ban%20location%20by-Joe%20Hendrickson%20via%20iStock.jpg)

With a market cap of $48.4 billion, Fifth Third Bancorp (FITB) provides a broad range of financial products and services through its principal subsidiary, Fifth Third Bank, National Association. The company operates across three segments: Commercial Banking; Consumer and Small Business Banking; and Wealth and Asset Management, serving individuals, businesses, government entities, and institutional clients.

Companies valued at more than $10 billion are generally considered “large-cap” stocks, and Fifth Third Bancorp fits this criterion perfectly. The company offers services including lending, deposit products, wealth management, investment advisory, mortgage banking, and insurance solutions.

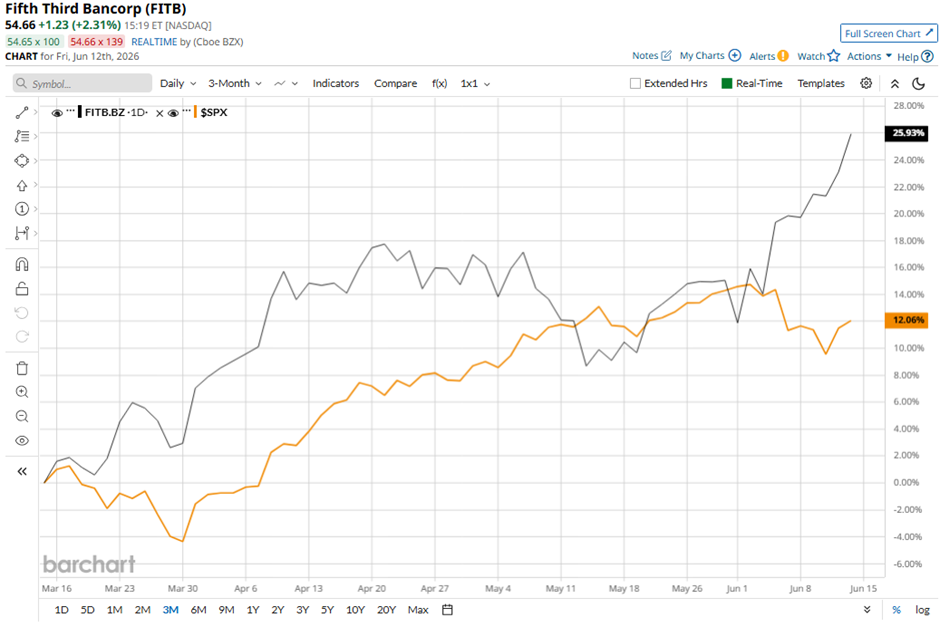

Shares of the Cincinnati, Ohio-based company have decreased 1.5% from its 52-week high of $55.44. Over the past three months, its shares have increased 25.1%, exceeding the broader S&P 500 Index’s ($SPX) 11.3% rise during the same period.

FITB stock is up 16.5% on a YTD basis, outperforming SPX's 8.5% gain. Longer term, shares of the company have returned 39.9% over the past 52 weeks, compared to the 22.9% return of the SPX over the same time frame.

The stock has been trading above its 200-day moving average since last year.

Shares of Fifth Third Bancorp rose 1.7% on Apr. 17 after the bank reported a strong Q1 2026 performance, with adjusted net income increasing to $731 million, supported by a 34% rise in net interest income to $1.93 billion. Investors were also encouraged by a 27-basis-point expansion in net interest margin and significant loan growth, as average portfolio loans and leases climbed to $157.63 billion from $121.27 billion a year ago.

Additionally, optimism surrounding the bank’s February acquisition of Comerica Incorporated and a 49% jump in capital markets fees to $134 million further boosted confidence.

In comparison, FITB stock has outperformed its rival, The PNC Financial Services Group, Inc. (PNC). PNC stock has gained 14% on a YTD basis and 33.9% over the past 52 weeks.

Due to FITB’s outperformance over the past year, analysts remain bullish about its prospects. The stock has a consensus rating of “Strong Buy” from 22 analysts in coverage, and the mean price target of $57.40 is a premium of 5% to current levels.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Arista%20sing%20at%20headquarters%20of%20an%20American%20multinational%20technology%20company%20Arista%20Networks%20-%20Santa%20Clara%2C%20California%2C%20USA%20-%202020%20By%20MichaelVi.jpeg)