Chipotle (CMG) shares have inched higher in recent sessions after JPMorgan’s senior analyst John Ivankoe issued a bullish note in favor of the fast-casual restaurant chain.

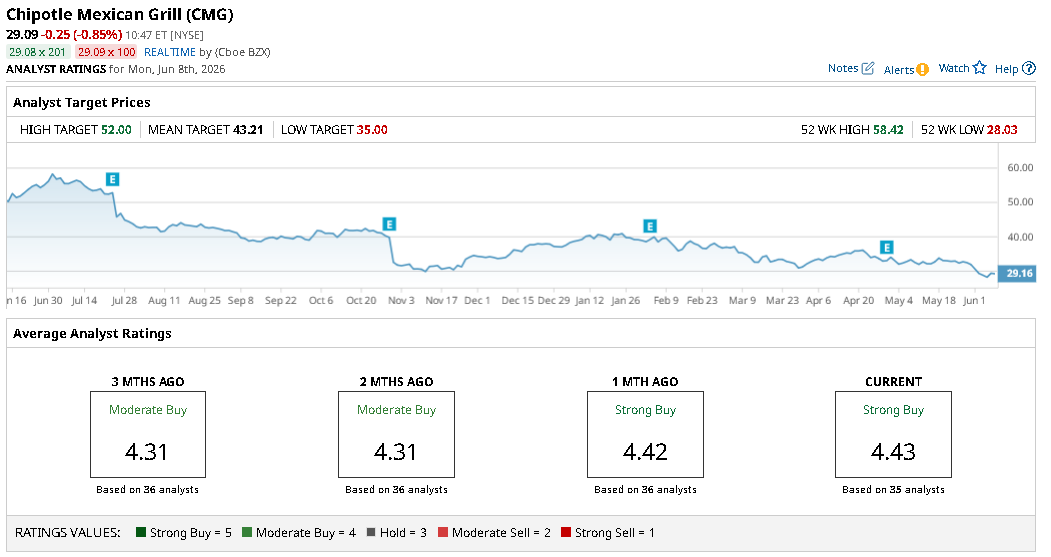

Ivankoe upgraded CMG to “Overweight” and announced a new $35 price objective, which signals potential upside of nearly 20% from current levels.

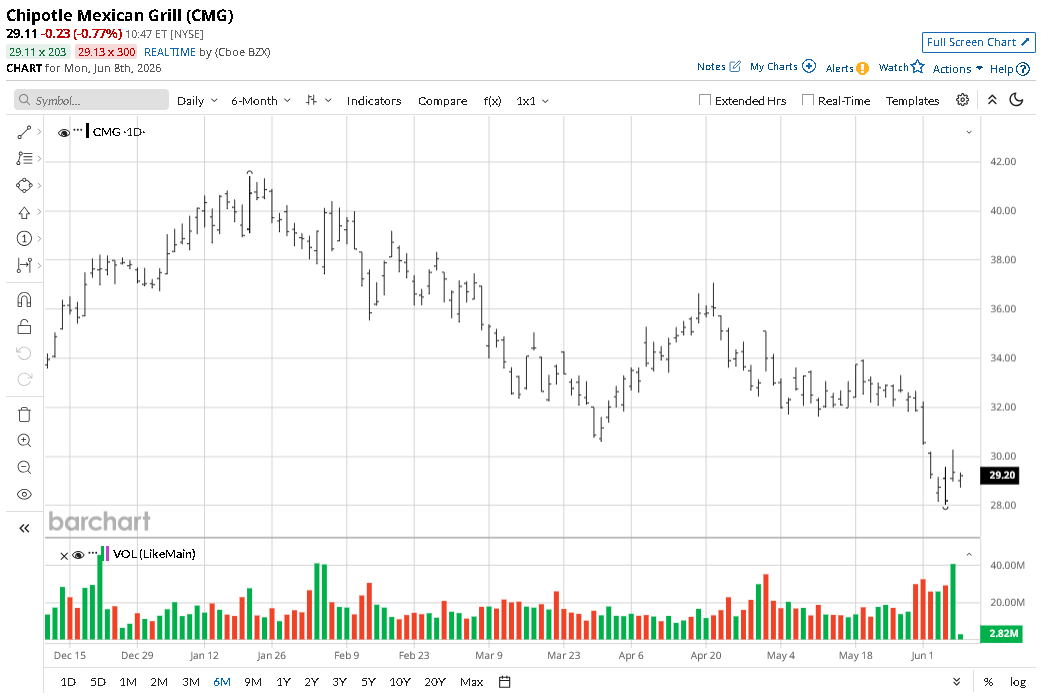

Despite recent gains, Chipotle stock remains down about 25% versus the start of this year.

Chipotle Is Attractively Priced in 2026

The core of Ivankoe’s upgrade is a valuation argument. CMG shares tanked by about 23% year-to-date versus the benchmark S&P 500 Index ($SPX), up roughly 10%.

This has repriced the company’s multiple to reflect a more measured growth trajectory, one that is slower than the pandemic-era peak but still well above the restaurant industry average.

In short — at less than $30 — Chipotle Mexican Grill presents far more risk-weighed upside than downside, he told clients in the research note.

JPM now frames CMG as offering “quality growth at the right price,” indicating a structural shift in how the firm sees its risk profile at these depressed levels.

What May Drive CMG Shares Higher?

Ivankoe’s upgrade followed a meeting at Chipotle’s headquarters with CEO Scott Boatwright and CFO Adam Rymer.

According to him, management was candid about past strategic mistakes and presented a forward-focused roadmap.

That conversation — combined with Q1 financials that surprised to the upside — gave JPM sufficient conviction to act.

The investment firm now projects about a 1.4% increase in same-store sales this year, ahead of CMG’s own guidance for flat comps.

With up to 370 new store openings planned for 2026, unit growth remains a durable tailwind even as the macro backdrop remains uncertain.

Note that Chipotle shares have a history of closing July with more than 2.5% gain on average — a seasonal pattern that makes them even more attractive to own in the near term.

How Wall Street Recommends Playing Chipotle

Other Wall Street analysts agree with Ivankoe’s bullish stance on CMG stock, especially since 60% of the company’s customers are households with earnings of more than $100,000 annually.

This positions Chipotle strongly to weather consumer pressures and stage a recovery to about $43 over the next 12 months, according to analysts.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/United%20Parcel%20Service%2C%20Inc_%20logo%20on%20truck-by%20100pk%20via%20iStock.jpg)