/Transdigm%20Group%20Incorporated%20logo%20on%20mobile-by%20madamF%20via%20Shutterstock.jpg)

Valued at a market cap of $68.6 billion, TransDigm Group Incorporated (TDG) designs, produces, and supplies aircraft components. The Cleveland, Ohio-based company’s vast product portfolio includes mechanical and electromechanical actuators, ignition systems, specialized pumps, valves, cockpit security displays, and seatbelts.

This aerospace and defense company has considerably underperformed the broader market over the past 52 weeks. Shares of TDG have declined 14.6% over this time frame, while the broader S&P 500 Index ($SPX) has soared 26.8%. Moreover, on a YTD basis, the stock is down 6.6%, compared to SPX’s 9.7% rise.

Zooming in further, TDG has also lagged the sector-focused State Street Industrial Select Sector SPDR ETF’s (XLI) 21.7% rise over the past 52 weeks and 12.7% uptick on a YTD basis.

On May 5, shares of TDG soared 3.6% after posting impressive Q2 results. The company’s revenue grew 18.3% year-over-year to $2.54 billion, surpassing analyst forecasts of $2.46 billion. Its adjusted EPS of $9.85 per share also topped the consensus estimate of $9.44.

Supported by the robust quarterly performance, management increased its full-year 2026 outlook and now expects revenue of roughly $10.36 billion and adjusted EPS of nearly $39.52 at the midpoint. The upbeat results and improved outlook signaled healthy demand for its aerospace components, bolstering investor confidence.

For the current fiscal year, ending in September, analysts expect TDG’s EPS to grow 5.9% year over year to $37.82. The company’s earnings surprise history is mixed. It exceeded the consensus estimates in three of the last four quarters, while missing on another occasion.

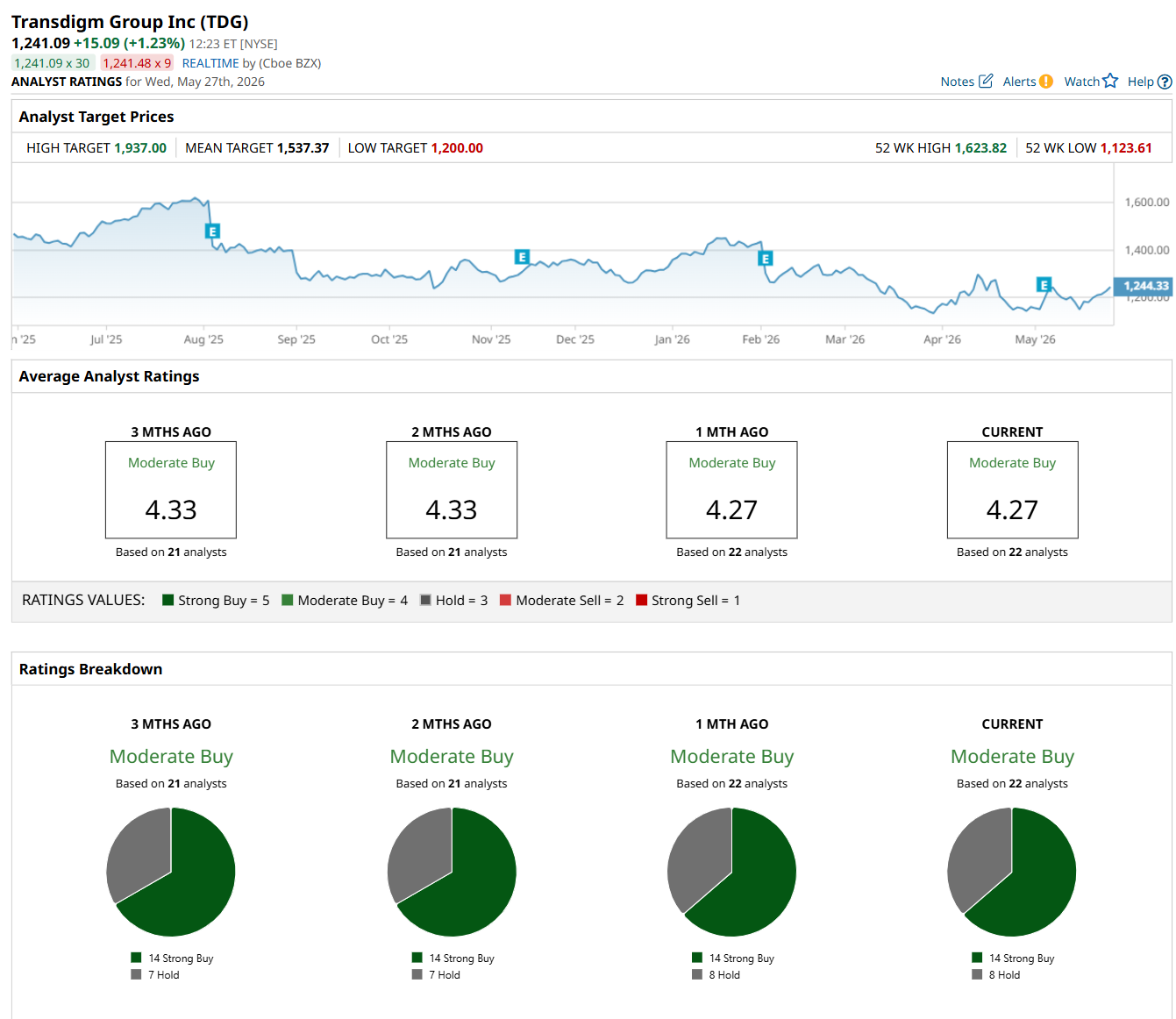

Among the 22 analysts covering the stock, the consensus rating is a "Moderate Buy," which is based on 14 “Strong Buy” and eight “Hold” ratings.

The configuration has remained fairly stable over the past three months.

On May 10, Jefferies maintained a “Buy” rating on TDG and raised its price target to $1,575, indicating a 26.9% potential upside from the current levels.

The mean price target of $1,537.37 suggests a 23.9% premium to its current price levels, while its Street-high price target of $1,937 implies a 56.1% potential upside.

On the date of publication, Neharika Jain did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)