/Charles%20River%20Laboratories%20International%20Inc_%20logo-%20by%20IgorGolovniov%20via%20Shutterstock.jpg)

Valued at a market cap of $7.7 billion, Charles River Laboratories International, Inc. (CRL) is a leading global provider of essential drug discovery, early-stage development, and manufacturing support services to the pharmaceutical, biotechnology, government, and academic sectors. The Wilmington, Massachusetts-based company serves as a vital contract research organization (CRO) that accelerates the life sciences pipeline, assisting in the development of a vast majority of the novel drugs approved by the FDA.

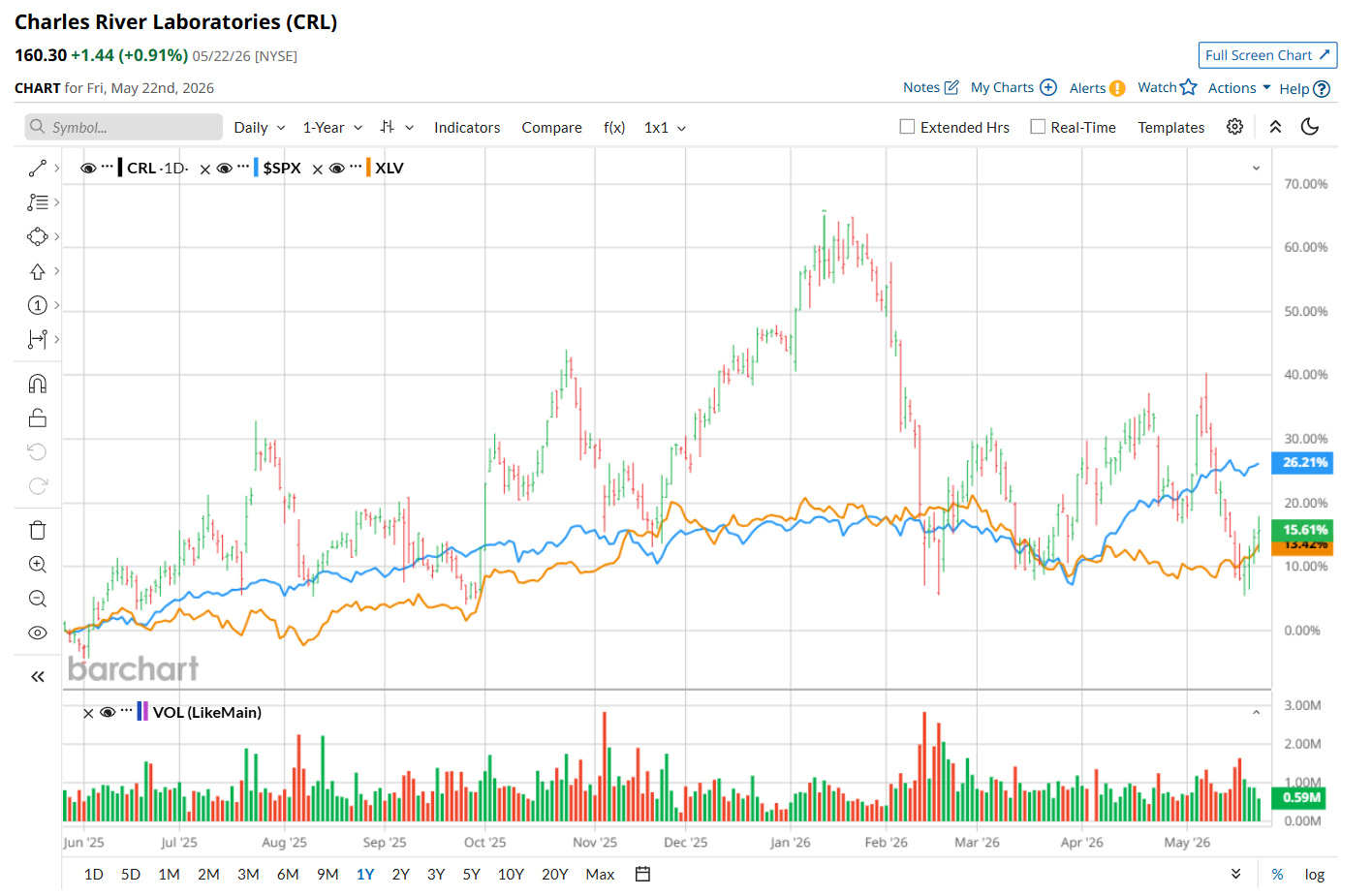

This healthcare company has underperformed the broader market over the past 52 weeks. Shares of CRL have gained 18.2% over this time frame, while the broader S&P 500 Index ($SPX) has soared 27.9%. Moreover, on a YTD basis, the stock is down 19.6%, compared to SPX’s 9.2% rise.

Narrowing the focus, CRL has outpaced the State Street Health Care Select Sector SPDR ETF’s (XLV) 14.8% rise over the past 52 weeks. However, it has lagged XLV’s 3.2% YTD drop.

On May 7, shares of CRL closed down marginally despite delivering better-than-expected Q1 results. The company’s revenue increased 1.2% year-over-year to $995.8 million, topping analyst estimates by 2.5%. Moreover, its adjusted EPS of $2.06 came in 5.1% ahead of consensus expectations. Management highlighted strategic divestitures, portfolio optimization initiatives, and ongoing cost-efficiency measures as major factors aiding its performance. Results were also supported by steady demand from global pharmaceutical clients, although activity levels among small and mid-sized biotech customers remained uneven across regions and business segments.

For the current fiscal year, ending in December, analysts expect CRL’s EPS to grow 7.5% year over year to $11.05. The company’s earnings surprise history is promising. It exceeded the consensus estimates in each of the last four quarters.

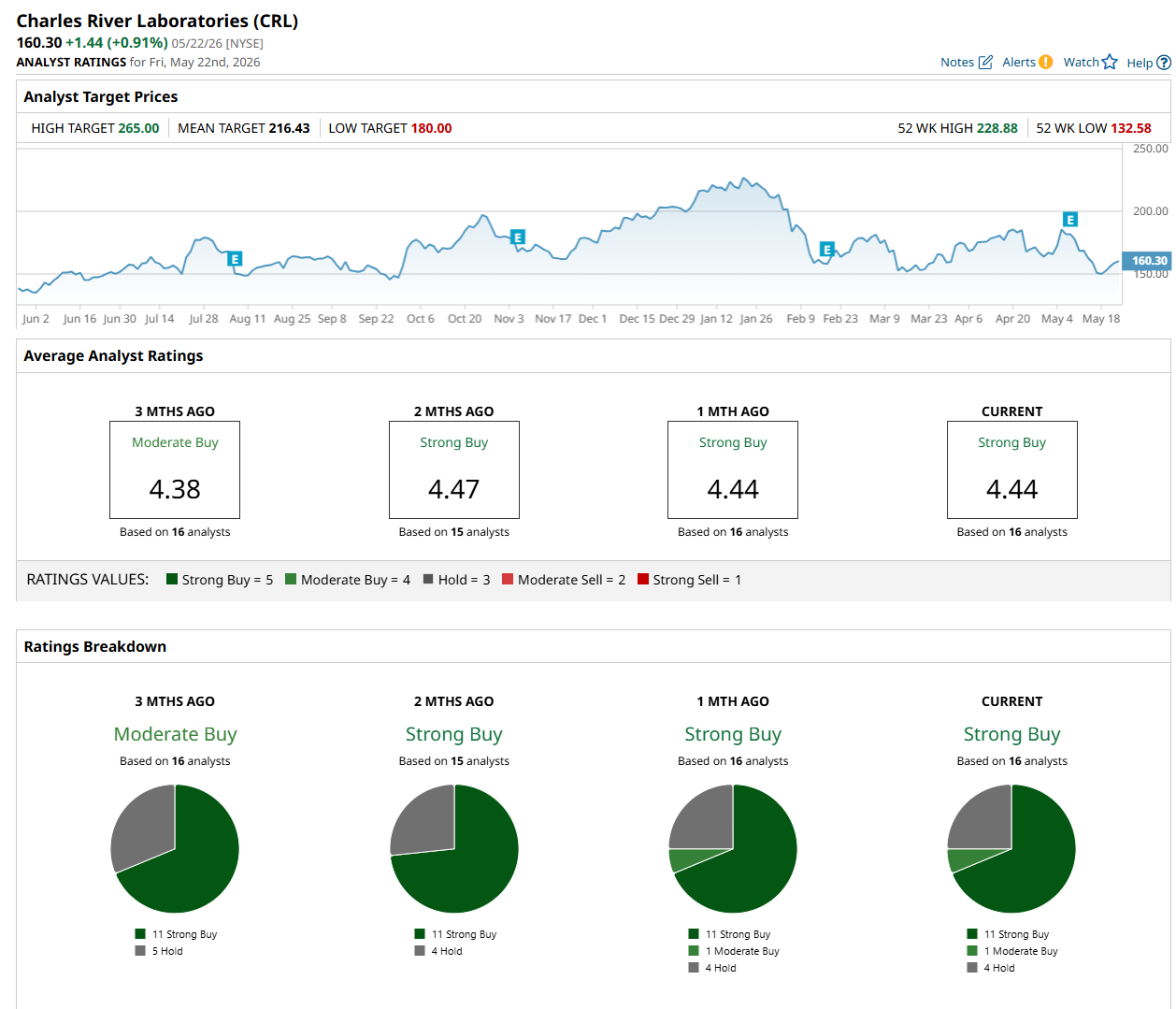

Among the 16 analysts covering the stock, the consensus rating is a "Strong Buy," which is based on 11 “Strong Buy,” one "Moderate Buy,” and four “Hold” ratings.

The configuration has remained fairly stable over the past three months.

On May 12, Morgan Stanley analyst Kallum Titchmarsh maintained a “Hold” rating on CRL and set a price target of $168.46, indicating a 5.1% potential upside from the current levels.

The mean price target of $216.43 suggests a 35% premium to its current price levels, while its Street-high price target of $265 implies a 65.3% potential upside.

On the date of publication, Neharika Jain did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/Green%20hydrogen%20by%20Scharfsinn%20via%20Shutterstock.jpg)

/Abbvie%20Inc%20HQ%20photo-by%20vzphotos%20via%20iStock.jpg)