/F5%20Inc%20HQ%20logo-by%20Sundry%20Photography%20via%20Shutterstock.jpg)

F5, Inc. (FFIV) is a prominent technology company that specializes in application delivery, cybersecurity, cloud networking, and enterprise application management solutions. Headquartered in Seattle, Washington, the company helps businesses secure, manage, and optimize applications across on-premise, cloud, and hybrid IT environments. The company is currently valued at a market capitalization of $22.2 billion.

FFIV shares have surged 38.4% over the past year, outpacing the broader S&P 500 Index ($SPX), which has rallied 27.9%. Moreover, the company's shares are up 54.2% year to date, compared with SPX’s 9.2% rise.

Narrowing the focus, FFIV stock has underperformed the State Street Technology Select Sector SPDR ETF’s (XLK) 57.3% rise over the past 52 weeks but has outpaced the ETF’s 25.3% rise in 2026.

On May 18, F5 shares rose 4.2% as investor sentiment toward traditional software and infrastructure companies improved. The rebound came as markets softened concerns that artificial intelligence could significantly disrupt established software businesses, with investors increasingly recognizing that companies like F5 benefit from entrenched enterprise relationships, mission-critical networking infrastructure, and growing AI integration opportunities within cybersecurity and application management.

For the fiscal year ending in September 2026, analysts expect FFIV's EPS to grow 7.8% year over year to $12.79. The company's earnings surprise history is solid. It beat the consensus estimates in the last four quarters.

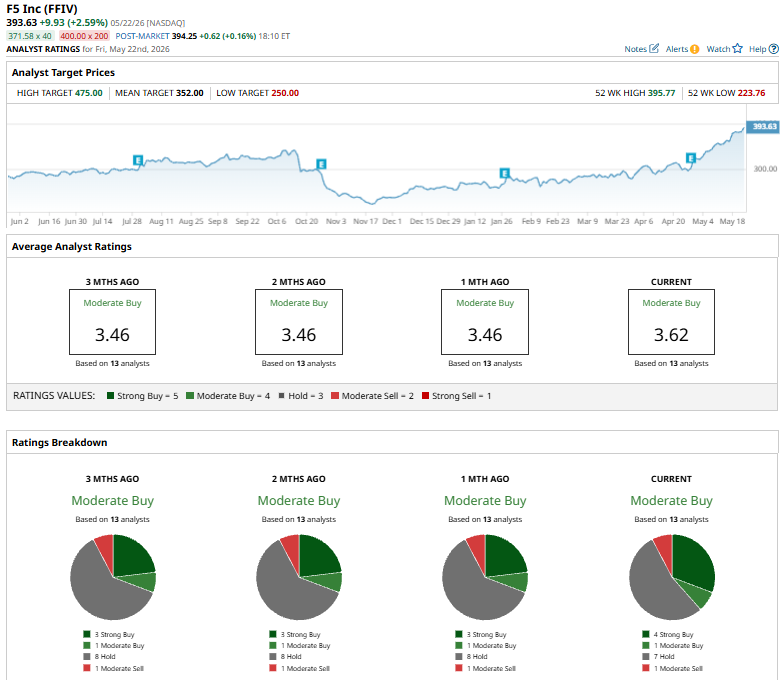

FFIV stock has a consensus “Moderate Buy” rating overall. Of the 13 analysts covering the stock, opinions include four “Strong Buys,” one “Moderate Buy,” seven “Holds,” and one “Moderate Sell.”

The configuration is bullish than a month ago when the stock had three “Strong Buy” suggestions.

On May 20, Morgan Stanley analyst Meta Marshall raised the price target on F5 to $380 from $340 while maintaining an “Equal Weight” rating on the stock. The higher target reflects improved confidence in F5’s business momentum, particularly its growing software and security revenue streams, although the firm continues to view the shares as fairly valued relative to peers.

The stock currently trades above the mean price target of $352, and the Street-high target of $475 implies 20.7% upside from the current market prices.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.