Equinix, Inc. (EQIX) is the company helping keep the modern digital world connected behind the scenes. Headquartered in Redwood City, California, it operates the world’s largest network of data center facilities, with more than 280 locations spread across six continents.

The company provides secure spaces where enterprises, cloud providers, telecom operators, and technology firms can store data, connect networks, and access cloud services with minimal delay. As demand for AI, cloud computing, and real-time digital services grows, Equinix has become a critical infrastructure player, building interconnected ecosystems that help businesses move data faster, operate efficiently, and stay connected globally. Its market capitalization currently stands at $106.5 billion.

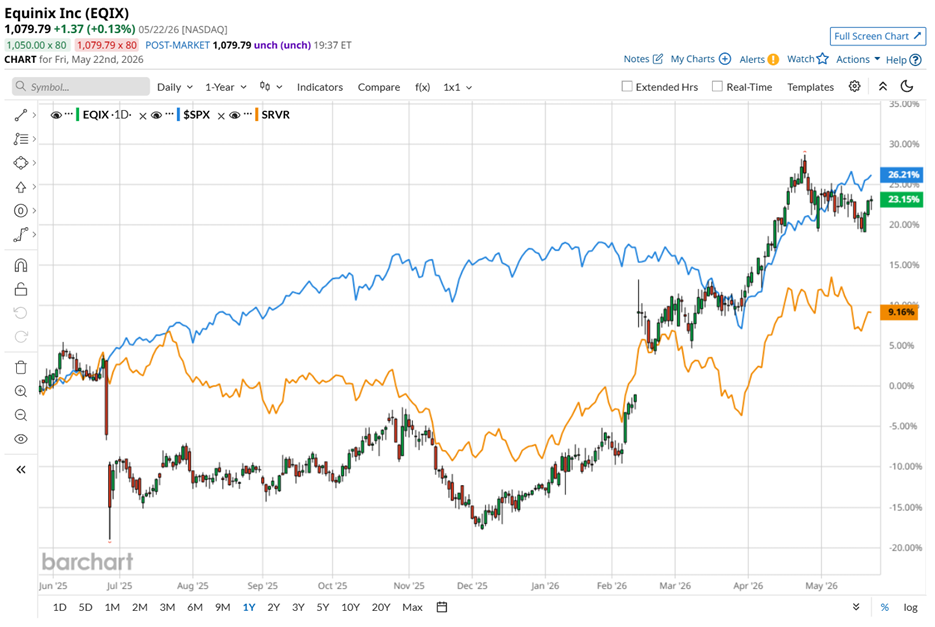

EQIX stock has climbed 24.6% over the past 52 weeks. While that still trails the S&P 500 Index’s ($SPX) 28% gains during the same stretch, the story in 2026 has looked far more impressive. EQIX stock has surged 41% on a year-to-date (YTD) basis, comfortably outperforming the broader market’s 9.2% gains.

The rally looks equally impressive when compared to the industry ETF. EQIX stock has comfortably outperformed the Pacer Data & Infrastructure Real Estate ETF (SRVR), which gained just 10.4% over the past year and rose 20% so far in 2026.

The biggest force behind Equinix’s rally has been the impressive rise of artificial intelligence and the enormous infrastructure needed to support it. As companies rapidly shifted from simply testing AI tools to deploying them across entire businesses, demand for high-performance data centers surged. That trend placed Equinix right in the middle of one of tech’s biggest spending waves.

The company continues benefiting from growing cloud adoption, hybrid multicloud architectures, and rising global data exchange needs. Businesses increasingly want secure, low-latency connections between cloud platforms, networks, and AI workloads – exactly where Equinix’s interconnected platform stands out.

Its recurring revenue model has also added stability to the growth story. In Q1 2026, recurring revenues rose 10% year over year (YOY), while colossal interconnection revenue climbed 9%. Operational momentum remained strong, too, with record cabinet backlogs and continued expansion across major global markets.

At the same time, Equinix has continued rewarding shareholders through steady dividend growth, balancing aggressive expansion with consistent long-term cash flow generation. The company has raised its quarterly dividend for a decade now. In fact, its annualized dividend yield of 1.91% exceeds the State Street SPDR S&P 500 ETF Trust’s (SPY) 0.99% yield.

Looking ahead, Wall Street still sees solid long-term momentum for Equinix, even if growth moderates briefly along the way. Analysts expect the company to generate funds from operations (FFO) of $37.72 per share for fiscal 2026, down slightly YOY. But in fiscal 2027, FFO is projected to rebound nearly 8.3% annually to $41.09 per share as AI-driven demand and expansion projects continue scaling. Equinix has also built a reputation for outperforming expectations. The company has beaten Wall Street estimates in each of the last four quarters, reinforcing investor confidence around execution and demand trends.

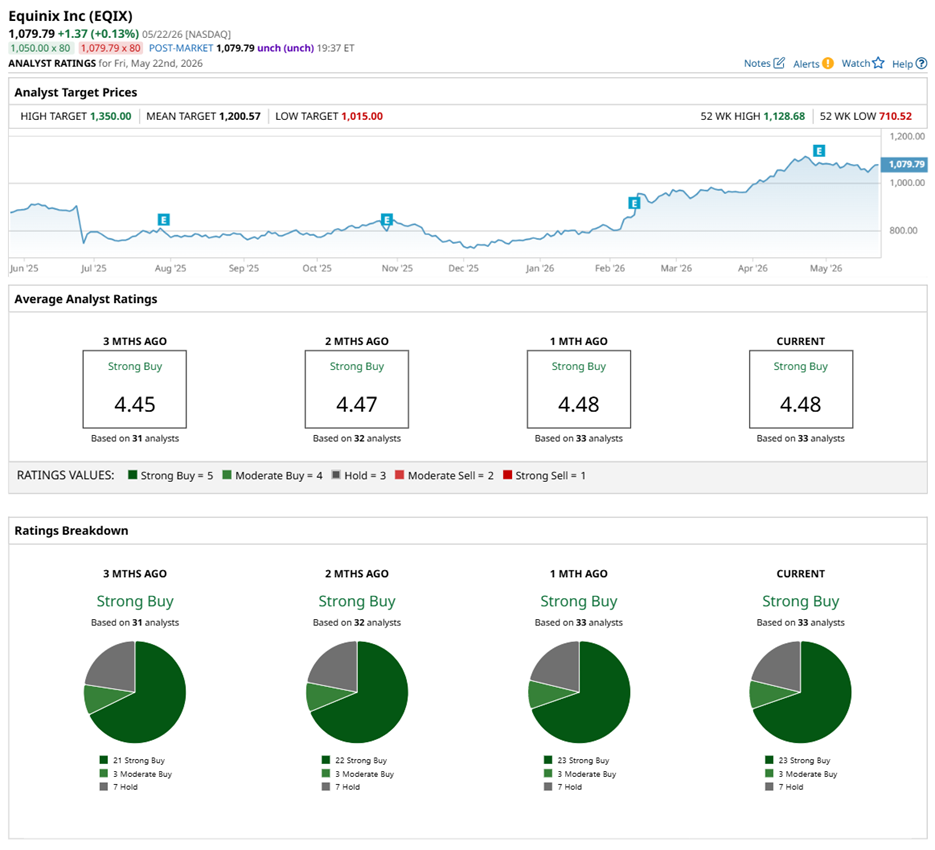

That optimism is clearly reflected in analyst sentiment, too. The overall consensus rating on EQIX stock currently sits at a “Strong Buy.” Among the 33 analysts covering the company, 23 recommend a “Strong Buy,” three suggest a “Moderate Buy,” while only seven remain on the sidelines with “Hold” ratings.

Analyst sentiment has grown a bit more optimistic lately, with the stock picking up an additional “Strong Buy” rating compared to two months ago.

On May 20, Guggenheim analyst Joseph Osha reiterated a “Buy” rating on EQIX and kept his $1,235 price target unchanged, signaling continued confidence in the company’s long-term growth story. As of writing, that suggests an upside potential of 14.4%.

EQIX’s average analyst price target is $1,200.57, indicating a potential upside of 11.2% from the current levels. The Street-high price target of $1,350 implies the stock could rise as much as 25% from the current price levels.

On the date of publication, Sristi Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Autodesk%20Inc_%20Portland%20office-by%20hapabapa%20via%20iStock.jpg)

/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)