/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

The semiconductor industry is having a huge year in 2026. Research firm Omdia has raised its 2026 chip revenue forecast to 62.7% year-over-year (YOY)growth, driven by strong demand for memory and logic chips as companies keep spending heavily on AI, servers, and cloud infrastructure. Computing and data storage revenue alone is expected to jump 90% this year to more than $700 billion, which would make 2026 the first year the global semiconductor industry tops $1 trillion in total revenue.

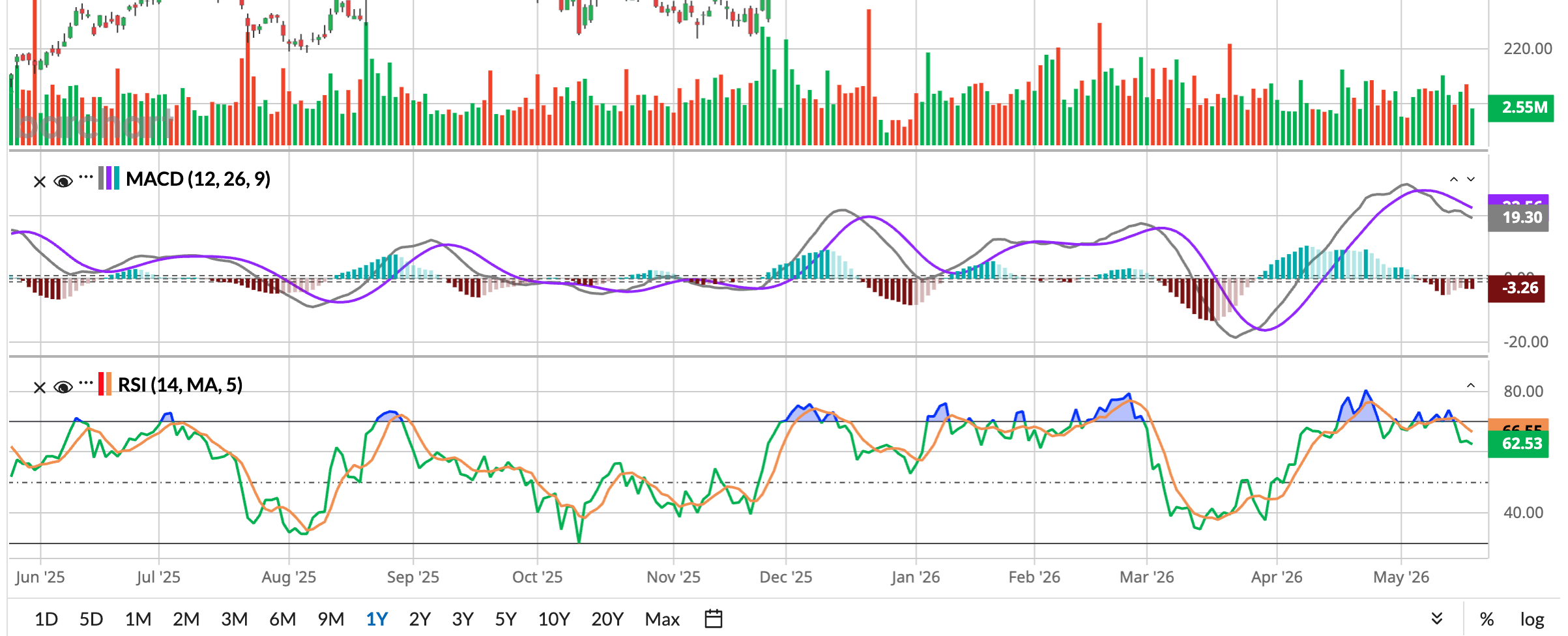

That strong backdrop has helped quality chip stocks move higher, and few have stood out more than Analog Devices (ADI). The Wilmington, Massachusetts-based company has caught Wall Street’s attention in 2026, with the stock up 84.39% over the past 52 weeks. That beats the S&P 500 Index ($SPX), which is up 23.1% and the S&P 500 Technology Sector SPDR Fund (XLK), which has returned 46.73% over the same period.

The rally has been backed by solid business performance. In its first quarter of fiscal 2026, Analog Devices posted 30% YOY revenue growth and a 51% increase in adjusted EPS, helped by strength in its industrial and communications businesses. Now, with the company set to report fiscal second-quarter 2026 results at 7:00 a.m. EST on Wednesday, May 20, followed by a conference call at 10:00 a.m. EST, investors are about to get a fresh look at whether that momentum is still going strong.

With the stock already up sharply and analysts calling for another 45.7% increase in full-year adjusted EPS for fiscal 2026, can this earnings report keep the rally going, or is the bar now too high?

Breaking Down Recent Performance

Analog Devices makes the chips and signal-processing products used in areas like factory equipment, cars, and communications systems. Its wide 52-week climb has helped the stock gain 53.95% year-to-date (YTD) and 79.81% in the past six months.

Ceretainly, the stock is not cheap. Analog Devices trades at about 36.77 times forward price-to-earnings, well above the sector average of 24.36 times. And, the company keeps returning cash to shareholders, with a 0.97% dividend yield, a quarterly dividend of $1.10, an 11% recent increase in that payout, a forward payout ratio of 45.58%, and a 24-year streak of dividend hikes.

In its latest quarter, Analog Devices reported $3.16 billion in revenue, up 30% from a year earlier, while adjusted EPS rose 51% to $2.46. Gross margin came in at 71.2%, and operating margin reached 45.5%, both showing the company is keeping a lot of profit from its sales.

Free cash flow was $1.26 billion in the quarter, and over the trailing 12 months, Analog Devices generated $5.1 billion in operating cash flow and $4.6 billion in free cash flow. It also returned $1 billion to shareholders in Q1. For the current quarter, the company expects revenue of about $3.5 billion and adjusted EPS of around $2.88.

Engines Powering Future Growth

In January 2026, Analog Devices made a direct strategic investment in Sense, a company focused on grid edge intelligence. The two companies are working with smart meter developers and other energy players to help build a smarter electric grid.

For Analog Devices, this is more than just an investment. It shows the company wants to play a bigger role in grid solutions by offering not just components, but also data and computing tools needed to make those systems work better. Sense’s software turns high-resolution data from smart meters into real-time insights for utilities, thereby helping consumers track and manage energy use within their homes.

Additionally, Analog Devices made a big supply chain move in October 2025. The company said it would work with ASE Industrial Holding (ASX) to sell its manufacturing plant in Penang, Malaysia, while further locking in a long-term supply agreement and co-investing in the site’s future capabilities. The goal is to make its supply chain stronger going into 2026 and beyond. The Penang facility, which opened in 1994 and covers more than 680,000 square feet in Bayan Lepas, will also help expand ASE’s global chip packaging and testing footprint.

Then in November 2025, Analog Devices rolled out CodeFusion Studio 2.0, an open-source AI development platform for embedded systems. It gives developers tools like model compatibility checks, performance testing, optimization features, multi-core support, broader device compatibility, and built-in debugging, all meant to make it easier and faster to deploy AI across Analog Devices’ processors and microcontrollers.

Analysts Signal What’s Ahead

For the April 2026 quarter, analysts expect Analog Devices to report earnings of $2.89 per share, up from $1.85 a year ago, which points to 56.22% growth. The next quarter is also expected to stay strong, with estimates at $2.96 compared to $2.05 last year, a 44.39% increase. For the full year, analysts see earnings reaching $11.35 for fiscal 2026, which would mean 45.70% growth.

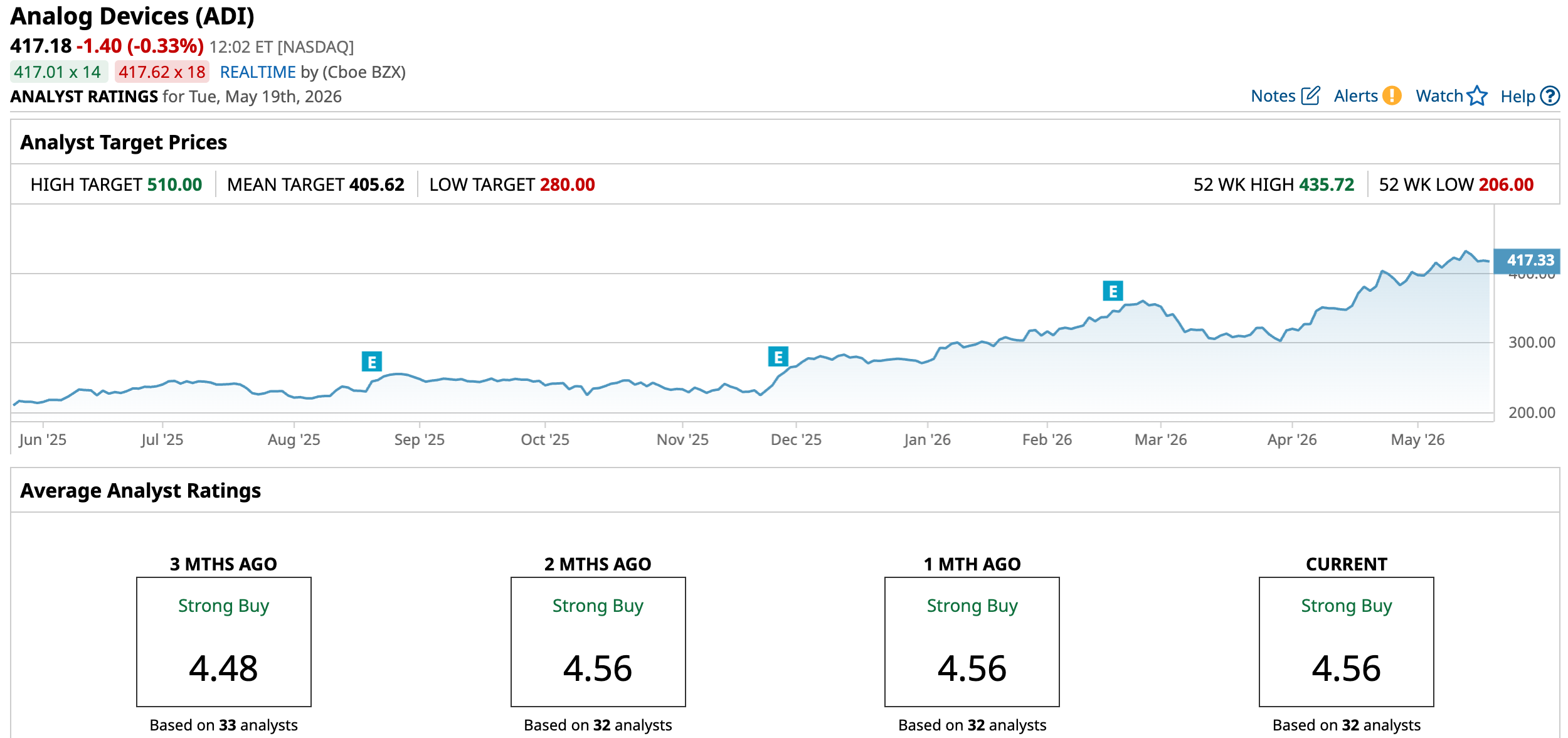

That confidence is showing up in analyst calls. On May 13, Wells Fargo raised its price target to $470 from $410 and kept an “Overweight” rating, pointing to steady demand across Analog Devices’ key markets. Earlier in the year, Morgan Stanley’s Joseph Moore raised his price target to $314 on January 16 and maintained an “Overweight” rating, showing continued institutional support even before the latest run higher.

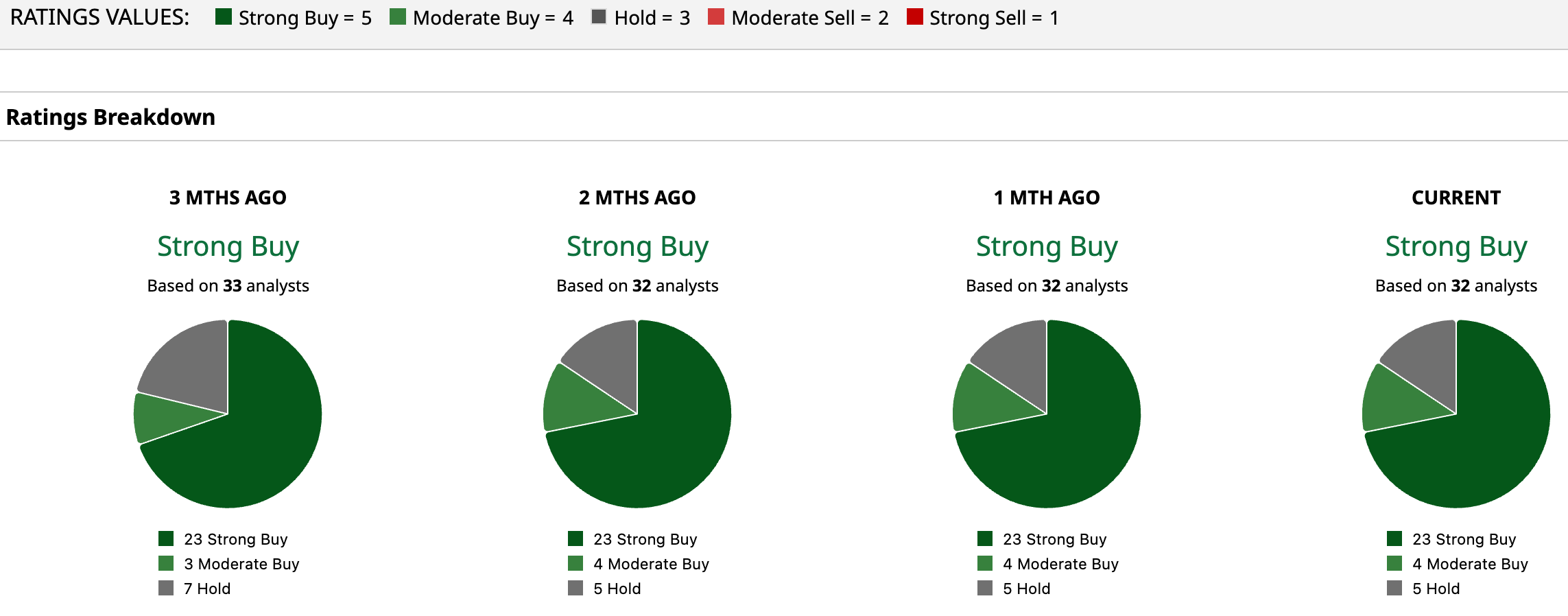

Overall, Wall Street is clearly bullish. A consensus among 32 analysts covering Analog Devices rates it a “Strong Buy.” Still, the average price target is $405.62, which is about 2.8% below the current price. Yet the Street-high price of $510 shows a possible upside of 22.3% from here.

Conclusion

Analog Devices heads into its May 20 earnings with strong momentum, along with a lot already priced in. The company is executing well, growth is accelerating, and Wall Street remains firmly bullish, yet the premium valuation leaves little room for disappointment. Most likely, the near-term direction will hinge on whether ADI can beat expectations and raise guidance again. If it does, the rally can extend further. If not, the stock could see a pause or modest pullback as investors reassess after such a sharp run.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)

/Apple%20products%20on%20desk%20by%20Ake%20Ngiamsanguan%20via%20iStock.jpg)

/McDonald's%20Corp%20arches%20by-%20TonyBaggett%20via%20iStock.jpg)