With a market cap of $17.8 billion, Dollar Tree, Inc. (DLTR) is a leading discount retail company that operates the Dollar Tree and Dollar Tree Canada brands across the United States and Canada, offering a wide range of affordable everyday products. It provides consumables, variety merchandise, and seasonal items to meet customers’ daily household and shopping needs.

Shares of the Chesapeake, Virginia-based company have lagged behind the broader market over the past 52 weeks. DLTR stock has risen 2.3% over this time frame, while the broader S&P 500 Index ($SPX) has gained 23.6%. Moreover, shares of the company are down nearly 28% on a YTD basis, compared to SPX’s 7.7% rise.

Narrowing the focus, shares of Dollar Tree have underperformed the Consumer Staples Select Sector SPDR Fund’s (XLP) 3.9% return over the past 52 weeks.

Shares of DLTR rose 6.4% on Mar. 16 after the company reported stronger-than-expected Q4 2025 results, including Q4 net sales growth of 9.0% to $5.45 billion, same-store sales growth of 5.0%, and adjusted EPS jumping 21% to $2.56. Investors were also encouraged by the company’s full-year fiscal 2026 guidance, which projected comparable store sales growth of 3% to 4%, net sales of $20.5 billion to $20.7 billion, and adjusted EPS of $6.50 to $6.90. Additional optimism stemmed from Dollar Tree’s aggressive shareholder returns and expansion strategy, which included $1.55 billion in share repurchases during fiscal 2025, 402 new store openings, and the expansion of its multi-price format to approximately 5,300 stores.

For the fiscal year, ending in January 2027, analysts expect DLTR’s adjusted EPS to increase 17.4% year-over-year to $6.75. The company’s earnings surprise history is promising. It beat the consensus estimates in the last four quarters.

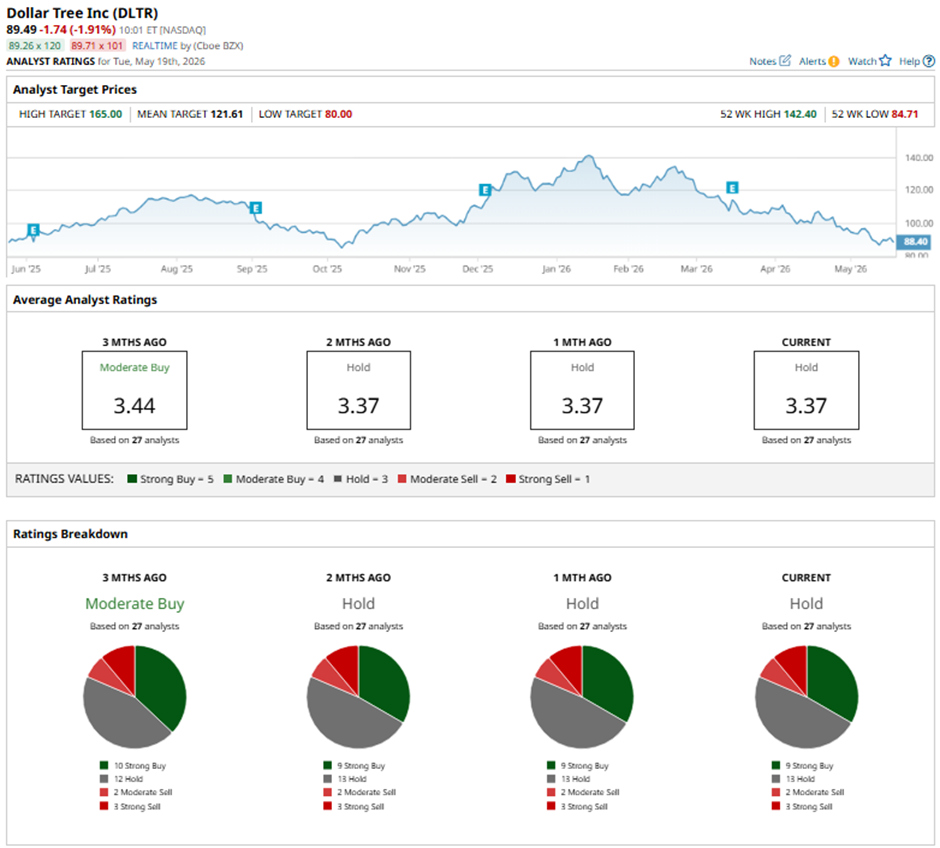

Among the 27 analysts covering the stock, the consensus rating is a “Hold.” That’s based on nine “Strong Buy” ratings, 13 “Holds,” two “Moderate Sells,” and three “Strong Sells.”

On May 18, Evercore ISI reduced its price target on DLTR to $140 while maintaining an “In Line” rating on the shares.

The mean price target of $121.61 represents a 35.9% premium to DLTR’s current price levels. The Street-high price target of $165 suggests a 84.4% potential upside.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/United%20Parcel%20Service%2C%20Inc_%20logo%20on%20truck-by%20100pk%20via%20iStock.jpg)