/Becton%20Dickinson%20%26%20Co_%20logo%20on%20phone-by%20T_Schneider%20via%20Shutterstock.jpg)

Becton, Dickinson and Company (BDX), abbreviated as BD, is a leading global medical technology firm that develops, manufactures, and distributes medical devices, diagnostics, laboratory systems, and related supplies.

Headquartered in Franklin Lakes, New Jersey, the company operates across multiple business segments to support healthcare delivery, patient safety, and clinical efficiency worldwide. The company has a market capitalization of $39.53 billion.

Over the past 52 weeks, the stock has gained a modest 5.9%, while it is down 6% year-to-date (YTD). The stock had reached a 52-week high of $187.35 on Feb. 24 but is down 23.4% from that level.

On the other hand, the broader S&P 500 Index ($SPX) has gained 25.2% over the past 52 weeks and 8.2% YTD, indicating that the stock has underperformed the broader market over these periods. Next, we compare the stock with its own sector. The State Street Health Care Select Sector SPDR ETF (XLV) has increased 11.2% over the past 52 weeks but dropped 6.3% YTD. Therefore, the stock has underperformed its sector over the past year.

In February, BD spun off its Biosciences & Diagnostic Solutions business with Waters Corporation (WAT). The company is trying to be a pure-play MedTech company. In this effort, over several years, BD has sold off three major non-core assets and executed over 20 targeted, small-scale acquisitions to strengthen the business and bolster its presence in more attractive areas of the healthcare sector. Following this move, BD had to reduce its adjusted EPS projection for fiscal 2026, rattling investors.

For the second quarter of fiscal 2026 (quarter ended Mar. 31), the company reported better-than-expected results. Its revenue increased 5.2% year-over-year (YOY) to $4.71 billion, while its adjusted EPS grew 3.9% annually to $2.90. BD also somewhat raised its FY26 adjusted EPS projected range. However, it is still below pre-spinoff expectations.

Wall Street analysts expect BD’s EPS to decrease 12.4% YOY to $12.61 on a diluted basis for fiscal 2026, followed by a 9.1% improvement to $13.76 in fiscal 2027. The company has topped consensus estimates in all four of the trailing quarters.

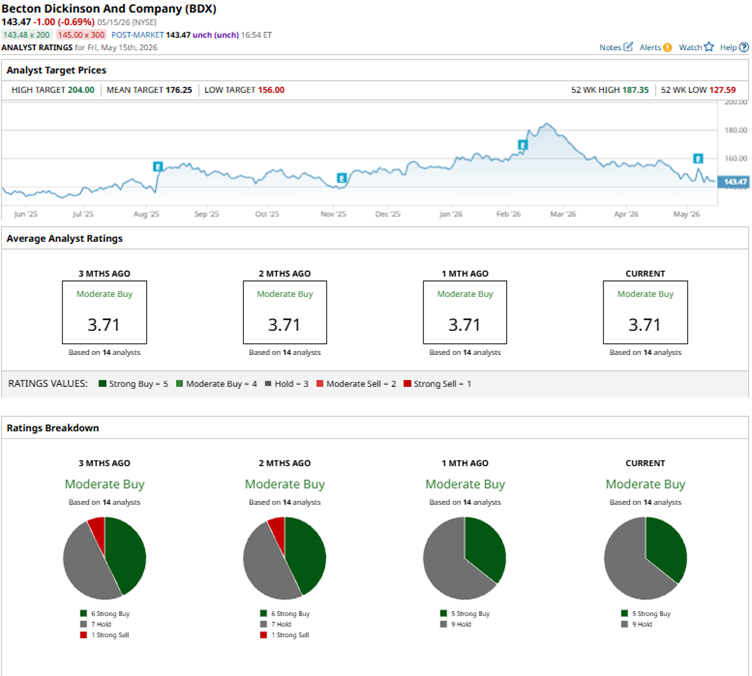

Among the 14 Wall Street analysts covering BD’s stock, the consensus is a “Moderate Buy.” That’s based on five “Strong Buy” ratings and nine “Holds.” The ratings configuration has become less bullish than two months ago, with five “Strong Buy” ratings, down from six.

Recently, analysts at Barclays maintained an “Overweight” rating on the stock and raised the price target from $202 to a Street-high of $204 following the company’s better-than-expected Q2 results. The analysts also believe the company is well-positioned in the current macro environment.

BD’s mean price target of $176.25 indicates a 22.8% upside over current market prices. The Street-high price target of $204 implies a potential upside of 42.2%.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Unitedhealth%20Group%20Inc%20HQ%20photo-by%20jetcityimage%20via%20iStock.jpg)