/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)

We’re used to AI breakthroughs in the form of model upgrades or chatbot updates. Alphabet’s (GOOGL) announcement of a next-generation laptop has shifted that debate into a new dimension, moving on from the traditional concept of Gemini as an AI assistant. The unveiling of Googlebook, an AI-first laptop built around Gemini Intelligence, begins a new era of devices that have AI at their core rather than just as a feature.

Googlebook will integrate Android apps, Chrome browsing, and contextual AI assistance directly into the operating system. In other words, AI will power the operating system. If a user is hovering over a date, the operating system can immediately suggest setting up an appointment or scheduling an event. This is just one example of how AI will be a core part of user workflow, moving away from the traditional operating system concept.

What Does Googlebook Mean for Investors?

Alphabet clearly wants AI to be the interface of the operating system. The tech may not be perfect right now, and no one knows how users will react, but Alphabet is early, and that is one of the key takeaways for investors. The move is also about ecosystem control. For instance, Google has always faced a threat from other search engines. In fact, AI chatbots have removed the need for users to go to Google to search for answers. By taking the initiative and controlling the AI that replaces Google search, Alphabet is ensuring that the disruption stays inside the company’s ecosystem.

Microsoft (MSFT) and Apple (AAPL) are the nearest competitors who intend to make similar moves to protect their own ecosystems. Apple is busy integrating Apple Intelligence throughout its iOS and macOS operating systems, while Microsoft is embedding Copilot across Windows and Office products. Whichever company is able to execute this best should dominate the emerging shift in how consumers utilize their personal devices.

About Alphabet Stock

Alphabet is a holding company that offers a broad range of digital products and services through its Google businesses. It runs platforms such as YouTube, Chrome, Google Search, Android, Google Drive, Google Photos, and more. The company also sells devices and subscription services, including YouTube Premium and Google One. It operates through three segments: Google Cloud, Google Services, and Other Bets.

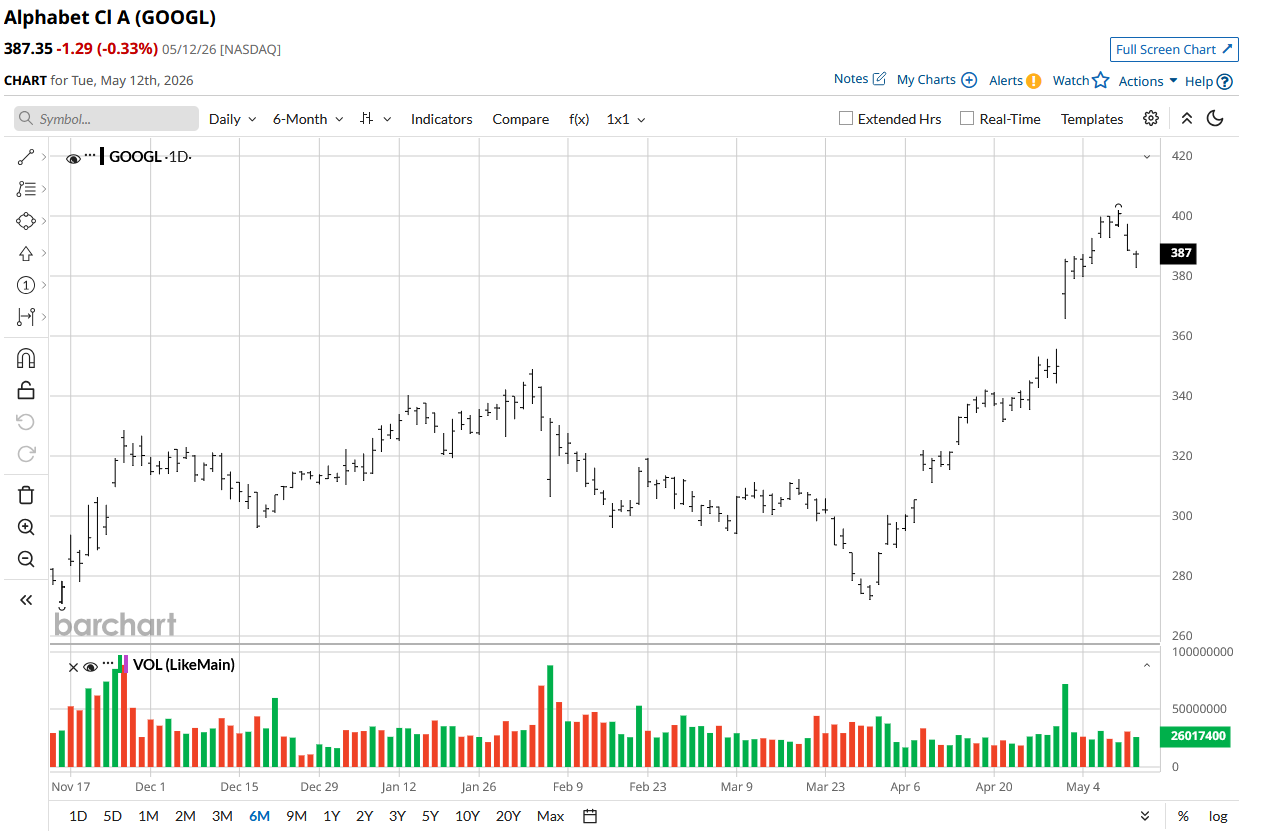

GOOGL stock has delivered an exceptional performance over the past year, more than doubling in value. During the same period, the S&P 500 ($SPX) has gained around 27%, compared to Alphabet’s return of about 142%. This means that GOOGL stock has generated returns over five times higher than the broader index. The outperformance has continued this year as well, with the stock up around 28% year-to-date (YTD) versus the S&P 500's approximately 10% gain.

The company is getting increasing respect from Wall Street thanks to its progress in artificial intelligence. The price-to-earnings (P/E) ratio hovered around 20 times for most of the last five years. The five-year average forward P/E is now 23.4 times, and the stock trades at a forward P/E of 27.1 times. This premium is justified when viewed in the context of the above news. Alphabet intends to be a leader in how AI transforms personal computing. If it is able to pull that off, it will command a higher multiple compared to Microsoft and Apple, which currently have forward P/E ratios of 24.3 times and 33.7 times, respectively.

Alphabet's Solid Earnings

Alphabet reported its first-quarter fiscal 2026 earnings on April 29, posting revenue of $109.9 billion. This was significantly above the consensus estimate of $107 billion. On the earnings front, GAAP EPS for the quarter came in at $5.11, exceeding market expectations of $2.64 per share. Google Cloud segment revenue rose 63% year-over-year (YOY) to $20 billion, while the Google Services segment generated $89.6 billion in revenue, representing 16% YOY growth. Operating income reached $39.7 billion with an operating margin of 36.1%.

TPU hardware sales are expected to start contributing to the top line later this year, with most of the revenue anticipated in 2027. However, these sales may fluctuate from quarter to quarter. Alphabet has also increased its 2026 capital expenditure guidance to between $180 billion and $190 billion, up from the earlier forecast of $175 billion to $185 billion.

What Do Analysts Think About Alphabet Stock?

Recently, analyst sentiment on GOOGL stock has turned more positive, with several analysts raising their price targets. On May 6, DBS analyst Sachin Mittal increased the firm’s price target from $400 to $460 while maintaining a “Buy” rating. On the same day, Mizuho increased its price target from $420 to $460 and reaffirmed an “Outperform” rating.

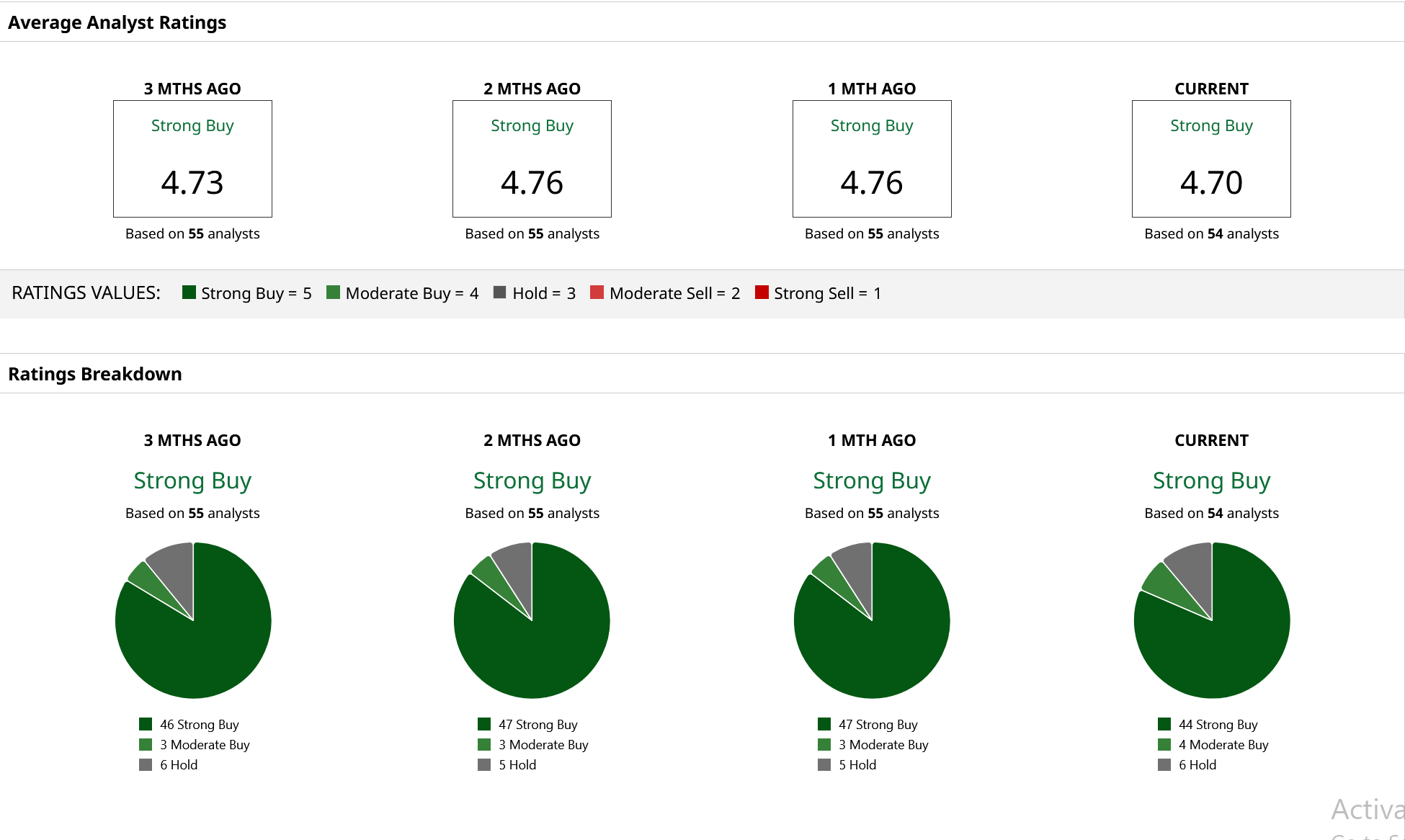

GOOGL stock is currently covered by 54 Wall Street analysts and carries a consensus “Strong Buy” rating. The mean price target of $423.12 reflects potential upside of 5% from current levels. Meanwhile, the highest price target of $515 suggests shares could climb 28% from here.

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)

/A%20game%20controller%20in%20front%20of%20a%20Roblox%20computer%20screen%20by%20Miguel%20Lagoa%20via%20Shutterstock.jpg)

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)

/Nvidia%20logo%20and%20sign%20on%20headquarters%20by%20Michael%20Vi%20via%20Shutterstock.jpg)