/Apple%20store%20and%20shoppers%20-%20by%20PhillDanze%20via%20iStock.jpg)

Dan Ives at Wedbush Securities has never been shy about picking favorites, and on Friday, May 8 he made sure nobody forgot that Apple (AAPL) sits right at the top of that list alongside NVIDIA Corporation (NVDA) and Tesla (TSLA). The firm sees a significant artificial intelligence (AI)-related catalyst brewing for the consumer electronics giant at Worldwide Developers Conference (WWDC) running from June 8 through June 12.

Wedbush believes Apple is the sleeping tech giant that is about to wake up swinging. The firm pointed to WWDC as the stage where Apple would finally lay out its full AI strategy, starting with a foundational AI consumer platform that brings Alphabet's (GOOG) (GOOGL) Gemini AI model into Apple's hardware ecosystem.

In addition, Wedbush has its eye on incoming CEO John Ternus, who would be taking over from Tim Cook on Sept. 1. Ternus has been inside Apple's walls since 2001 and currently holds the role of senior vice president of hardware engineering, overseeing the iPhone, iPad, Mac, Apple Watch, and AirPods.

The firm believes AI monetization and services growth would add $75 to $100 to Apple's stock price. Wedbush also sees Apple growing into a consumer hub of AI technology, a positioning that could generate an additional $15 billion in annual services revenue over the coming years.

AAPL responded by hitting a fresh 52-week high of $294.76 on May 8. Now, let us see where the stock would go from here.

About Apple Stock

Headquartered in Cupertino, California, Apple has cemented itself as the beating heart of consumer hardware and software. The company's ecosystem covers iPhone, Mac, iPad, wearables, services, custom silicon and more.

At a market cap of $4.31 trillion, Apple keeps its recurring revenue machine well-oiled through a growing services segment that leans on the App Store, iCloud, and Apple Music to do the heavy lifting. The deeper users dig into the ecosystem, the harder it becomes to imagine life outside it, which is precisely the kind of user retention strategy that keeps the revenue story looking good quarter after quarter.

AAPL stock has rewarded its believers quite generously on the price performance front, gaining 47.18% over the last 52 weeks. The past three months added another 6.06% to that tally, and the past month alone threw in an additional 12.17% for good measure.

Valuation is where the stock makes bargain hunters sweat a little. AAPL stock is currently trading at 32.88 times forward adjusted earnings and 9.02 times sales, both figures running well ahead of industry averages and the stock's own five-year historical multiples. The market has been paying a steep cover charge to get into this party for a while now.

Moreover, the consumer electronics giant has grown its dividend for 13 consecutive years, paying out an annual dividend of $1.08 per share at a yield of 0.37%. On April 30, the company declared a cash dividend of $0.27 per share, a 4% bump over the prior amount, payable on May 14 to shareholders of record as of the close of business on May 11.

Apple Surpasses Q2 Earnings

On April 30, Apple dropped its Q2 fiscal year 2026 earnings, wherein revenue climbed 16.6% year-over-year (YOY) to $111.2 billion, comfortably clearing analyst estimates of $109.3 billion. EPS rose 21.8% from the year-ago value to $2.01, beating what analysts had penciled in at $1.94.

The details, as it turns out, are where things get genuinely interesting. iPhone revenue alone grew 21.7% YOY to $57 billion, which is a March record by itself. Services kept pace by hitting an all-time revenue record, growing 16.3% from a year ago to reach $31 billion.

During the quarter, Apple also introduced what it called its strongest product lineup ever, bringing the iPhone 17e and the M4-powered iPad Air into the fold alongside the MacBook Neo, which has been turning heads across markets worldwide.

Operating income rose 21.3% from the prior year's period to $35.9 billion, net income grew 19.4% from the year-ago value to $29.6 billion, and cash and cash equivalents swelled to $45.6 billion on March 28, up from $35.9 billion on Sept. 27, 2025.

Looking forward, analysts expect Q3 fiscal year 2026 EPS to land at $1.86, marking an 18.5% YOY increase. Full-year fiscal 2026 EPS estimates sit at $8.74, pointing to 17.2% annual growth, and fiscal year 2027 estimates take that figure to $9.54, piling on another 9.2% growth on top of that.

What Do Analysts Expect for Apple Stock?

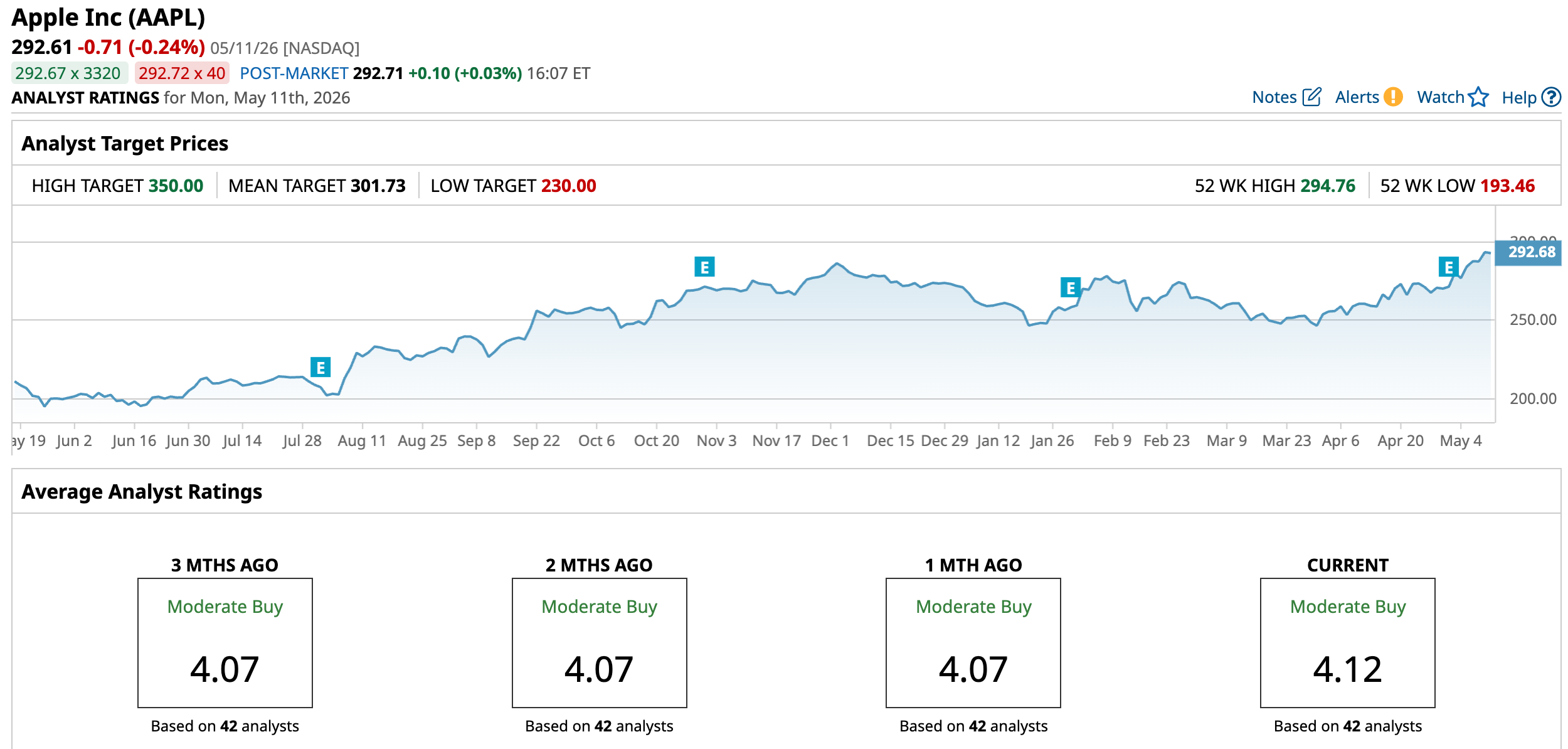

Wall Street analysts are wasting no time in updating their Apple scorecards. Wells Fargo's Aaron Rakers keeps his “Overweight” rating and has nudged his price target to $310 from $300, crediting Apple's solid results and better-than-expected guidance on revenue and gross margin. Not exactly a bold leap, but a vote of confidence, nonetheless.

TD Cowen took a slightly more ambitious swing, raising its price target from $325 to $335 while standing firm on its “Buy” rating.

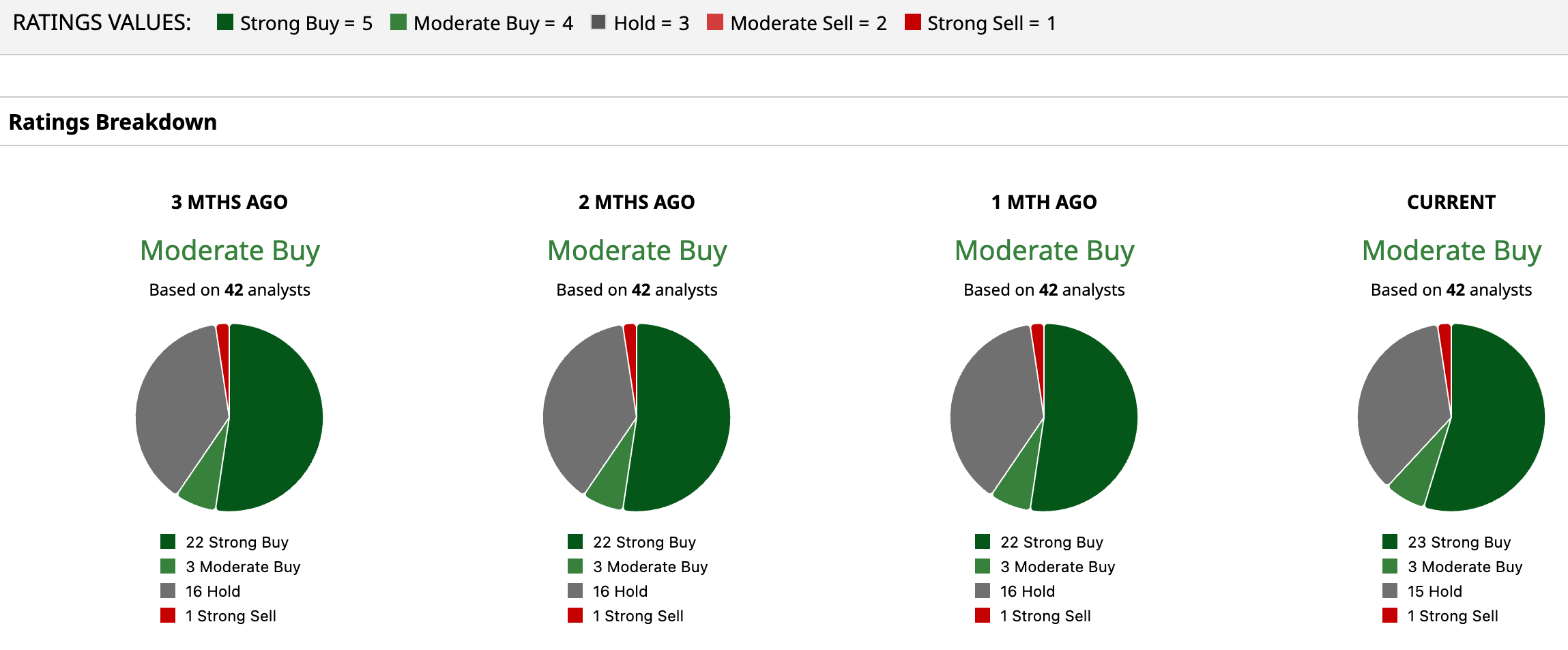

The broader analyst community, all 42 of them, have collectively assigned an overall rating of “Moderate Buy” to AAPL stock. Breaking that down, 23 stamp it a "Strong Buy," three hand it a "Moderate Buy," 15 sit on the fence with a "Hold," and one flags a "Strong Sell."

The average price target of $301.73 already bakes in an upside of 3.12%. Meanwhile, the Street-High target of $350 suggests a gain of 19.6% from current levels.

Finally, Wedbush, which has skipped the cautious lane entirely and jacked its price target to $400 from $350, is holding its “Outperform” rating, with WWDC serving as the moment the firm is betting the whole thesis on.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/AI%20(artificial%20intelligence)/AI%20chip%20by%203Dsss%20via%20Shutterstock.jpg)