/Aon%20plc_%20office%20sign-%20by%20JHVEPhoto%20via%20Shutterstock.jpg)

With a market cap of $66.4 billion, Aon plc (AON) is a multinational professional services company specializing in risk, retirement, and health solutions. The Ireland-based company helps businesses identify, manage, and transfer risks while also advising on human capital strategy, insurance brokerage, reinsurance, wealth solutions, and employee benefits.

Shares of this leading professional services firm have underperformed the broader market over the past year. AON has declined 10.5% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 27.3%. In 2026, AON stock is down 10.6%, compared to the SPX’s 9.6% rise on a YTD basis.

Narrowing the focus, AON’s underperformance is also apparent compared to the SPDR S&P Insurance ETF (KIE). The exchange-traded fund has declined 3.2% over the past year and has dipped 6.5% on a YTD basis.

On May 1, Aon released its FY2026 first-quarter results, and its shares gained 1.1% in the following trading session as investors reacted positively to the company’s solid organic growth, expanding margins, and strong cash flow performance. Revenue rose 6.4% year over year to $5.03 billion, supported by 5% organic revenue growth across its Risk Capital and Human Capital businesses. Adjusted EPS increased 14.3% YOY to $6.48, ahead of Wall Street expectations, thanks to continued strength in Commercial Risk and Reinsurance, alongside resilient demand for health and benefits advisory services.

For the current fiscal year, ending in December, analysts expect AON’s EPS to grow 11.7% to $19.07 on a diluted basis. The company’s earnings surprise history is solid. It beat the consensus estimates in each of the last four quarters.

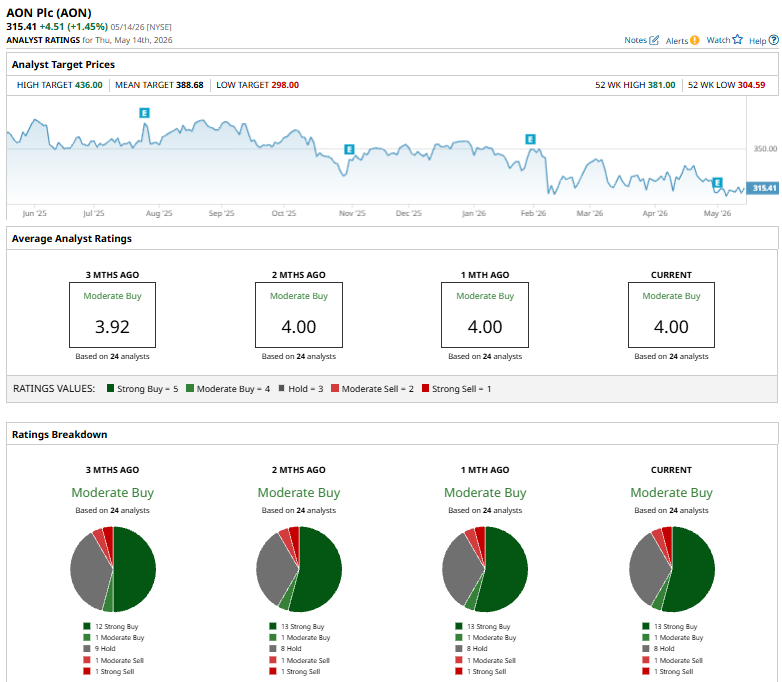

Among the 24 analysts covering AON stock, the consensus is a “Moderate Buy.” That’s based on 13 “Strong Buy” ratings, one “Moderate Buy,” eight “Holds,” one “Moderate Sell,” and one “Strong Sell.”

This configuration is more bullish than three months ago, with 12 analysts suggesting a “Strong Buy.”

On Apr. 13, Mizuho analyst Yaron Kinar trimmed the price target on Aon to $394 from $397 while maintaining an “Outperform” rating on the shares. The revision came as the firm updated estimates and valuation targets across its North American insurance coverage universe. Mizuho said it remains most optimistic on insurance brokers, expects pricing pressures to ease among property and casualty insurers, and views the outlook for life insurers as the most challenging within the sector.

The mean price target of $388.68 represents a 23.2% premium to AON’s current price levels. The Street-high price target of $436 suggests an upside potential of 38.2%.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)

/Palo%20Alto%20Networks%20headquarters%20campus%20exterior%20of%20cybersecurity%20company%20By%20MichaelVi.jpeg)