Sony Group (SONY) is one of the trickier large-cap tech stocks to size up right now. The company is once again in the spotlight, and this time the story is not just about games, movies, or music. The bigger headline is Sony’s planned joint venture with Taiwan Semiconductor Manufacturing Company (TSM) to develop and produce next-generation image sensors, a move that could help shape the future of physical AI, autonomous driving (AD), robotics, and smart manufacturing.

Sony already leads the global image sensor market, so this partnership is less about catching up and more about defending and extending that dominance for the next decade. For investors, the deal raises an important question: Can Sony turn this strategic move into a lasting stock rebound after a painful selloff?

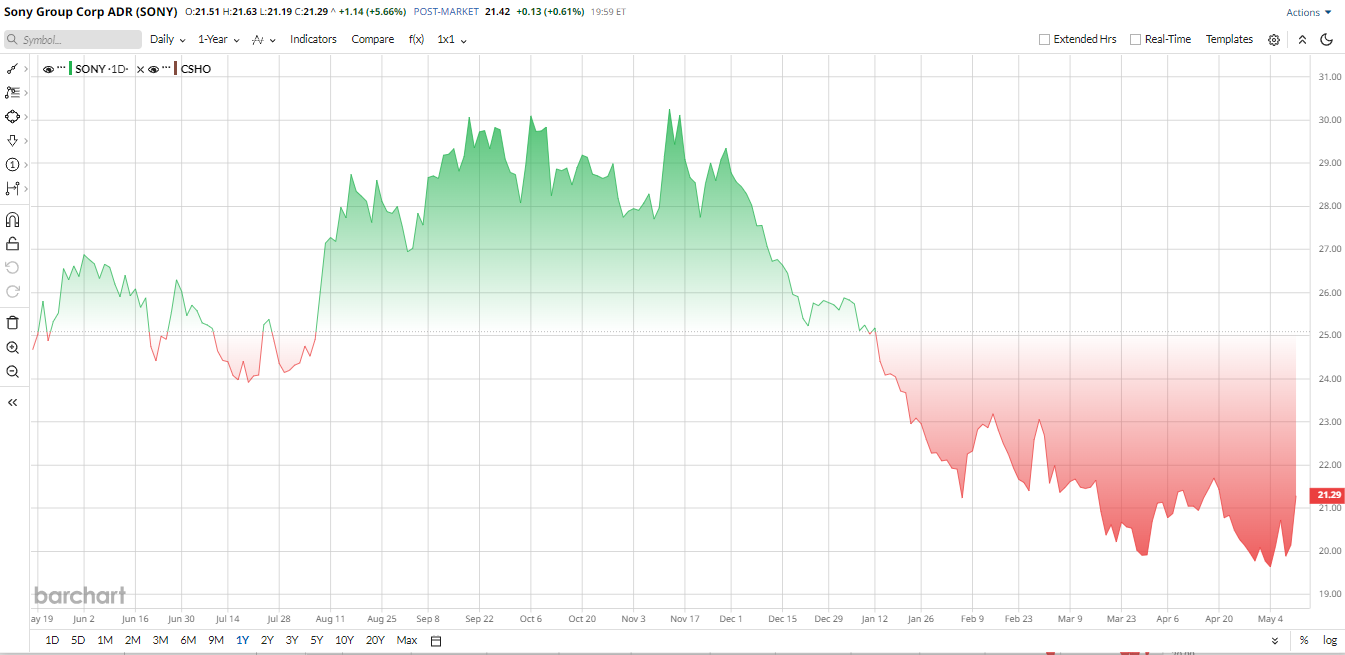

Sony Stock Has Been Down, But the Catalyst List Is Growing

SONY stock has had a rough 2026, down 11% year to date (YTD) after a sharp slide from earlier highs. The pressure has been tied in part to a $765 million Bungie-related impairment charge and lingering concerns that PlayStation hardware demand could stay under pressure.

At the same time, the new Sony-Taiwan Semiconductor plan gives investors something different to focus on. The deal itself is still only a non-binding memorandum of understanding, but the strategic direction is clear. Sony would control the joint venture, which would be located at its new fab in Koshi City, Kumamoto, with Japanese government support of up to ¥60 billion ($380 million). That matters because Sony already dominates image sensors, and this move is about protecting that lead rather than chasing it.

The Valuation Looks Interesting

This is where Sony starts to look appealing to patient investors. SONY stock trades at roughly 16.7 times trailing earnings, about 15.9 times forward earnings, and around 1.5 times sales. That is not screaming cheap, but it is also not a stretched valuation for a company with deep entertainment assets, a strong cash position, and a sensor business that could benefit from a longer hardware upgrade cycle.

Sony's Latest Quarter Was Mixed, But Not Weak

Sony’s latest fiscal 2025 results were mixed. Revenue rose 4% to ¥12.48 trillion ($78.5 billion), while net profit slipped 3% to ¥1.03 trillion ($6.5 billion). Operating profit climbed 13% to ¥1.45 trillion ($9.2 billion), although that still came in below analyst expectations. Sony also ended the year with healthy liquidity and announced a buyback of up to ¥500 billion ($3.2 billion), which tells you management thinks the stock is undervalued.

The guidance was better than the headline profit dip suggests. Sony is guiding for a record net profit of ¥1.16 trillion ($7.3 billion) in fiscal 2026, even as gaming sales are expected to fall 6% to ¥4.42 trillion ($28 billion).

At the same time, gaming profit is forecast to rise 30%, helped by stronger software sales and the absence of last year’s Bungie impairment. Sony also expects the Imaging and Sensing Solutions unit to see operating profit improve even if revenue eases, which is exactly the kind of mix shift bulls want to see.

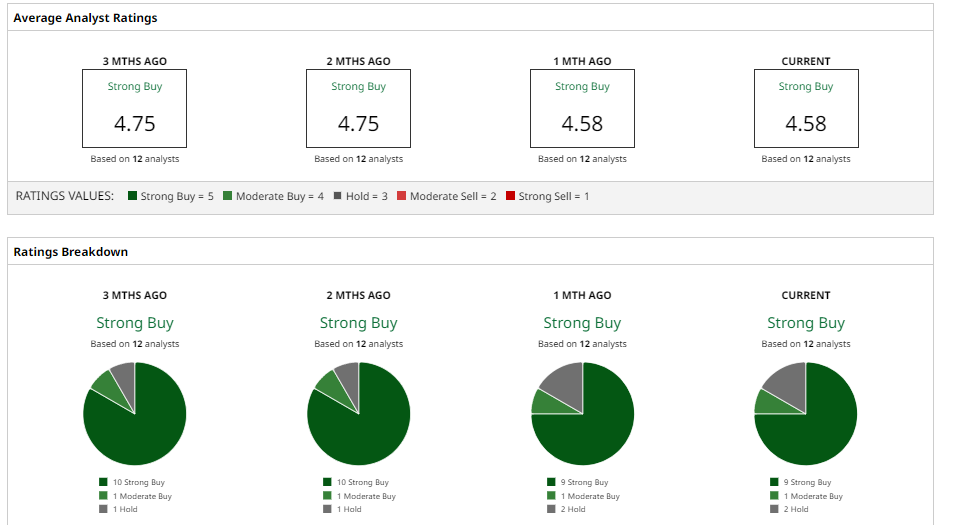

What Do Analysts Think of SONY Stock?

Wall Street is constructive, but not fully aligned on the timing. Bernstein SocGen recently lifted its target to ¥3,500 while keeping a “Market Perform” rating, and TD Cowen cut its target to $29 from $34 while still recommending a “Buy.”

Overall, the consensus is a “Strong Buy” rating as analysts remain optimistic for Sony's comeback after strong earnings. Plus, the mean price target of $29.75 implies potential upside of 31% from current levels.

That is the real Sony debate. The company is not just trying to defend an old business. It is trying to build a better one. If the Taiwan Semiconductor partnership helps Sony extend its image-sensor lead while the content engine keeps throwing off cash, SONY stock could look very different five years from now. For now, the market is still waiting to believe it.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Elon%20Musk%2C%20founder%2C%20CEO%2C%20and%20chief%20engineer%20of%20SpaceX%2C%20CEO%20of%20Tesla%20by%20Frederic%20Legrand%20-%20COMEO%20via%20Shutterstock.jpg)

/2d%20illustration%20of%20Cloud%20computing%20by%20Blackboard%20via%20Shutterstock.jpg)