With a market cap of $39.1 billion, Consolidated Edison, Inc. (ED) is one of the largest regulated utility companies in the United States. Headquartered in New York City, the company provides electricity, natural gas, and steam services to millions of customers through its primary subsidiary, Con Edison of New York.

Shares of this leading utility have underperformed the broader market over the past year. ED has gained 3.3% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 26.6%. In 2026, ED’s stock rose 7.6%, compared to the SPX’s 8.1% rise on a YTD basis.

Narrowing the focus, ED’s underperformance is also apparent compared to the Utilities Select Sector SPDR Fund (XLU). The exchange-traded fund has gained about 13.3% over the past year. However, the ETF’s 5.9% YTD return lags the stock’s gains over the same period.

On Apr. 28, Consolidated Edison reported its Q1 2026 earnings, and its shares rose marginally. Operationally, Con Edison continued to benefit from strong demand trends across its regulated utility business, supported by ongoing electrification and infrastructure investments in its New York service territories. Its adjusted EPS declined 3.5% year over year to $2.18. For FY 2026, Con Edison reaffirmed its non-GAAP EPS to be in the range of $6.00 to $6.20 per share.

For the current fiscal year, ending in December, analysts expect ED’s EPS to grow 6.4% to $6.09 on a diluted basis. The company’s earnings surprise history is mixed. It beat the consensus estimate in three of the last four quarters while missing the forecast on another occasion.

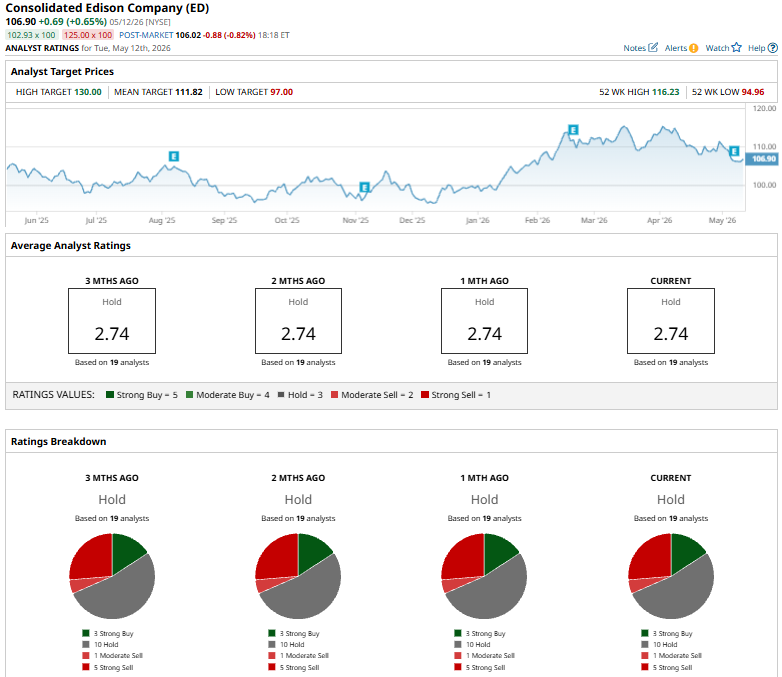

Among the 19 analysts covering ED stock, the consensus is a “Hold.” That’s based on three “Strong Buy” ratings, ten “Holds,” one “Moderate Sell,” and five “Strong Sells.”

On May 11, Barclays analyst Nicholas Campanella reiterated an “Underweight” rating on Consolidated Edison and lowered the price target to $107 from $110.

The mean price target of $111.82 represents a 4.6% premium to ED’s current price levels. The Street-high price target of $130 suggests an upside potential of 21.6%.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Alphabet%20Inc_%20and%20Google%20logos%20by%20IgorGolovinov%20via%20Shutterstock.jpg)

/Technological%20process%20of%20soldering%20chip%20components%20on%20PCB%20board%20by%20I%20Viewfinder%20via%20Adobe%20Stock.jpeg)