/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

The rise in CPU demand has left companies scrambling to book manufacturing capacity, and Advanced Micro Devices (AMD) is no different. The Lisa Su-led chip designer is reported to be close to signing a deal with Samsung (SMSN.L.EB) to manufacture some of its 2nm process chips. The two companies have been working together for months now, with initial reports back in December 2025 stating that Samsung’s 2nm tech could fulfill AMD’s advanced CPU manufacturing requirements.

Previously, Samsung failed to deliver attractive yields on its 3nm process, but it has had considerable success on the 2nm process. On April 30, it was reported that Samsung had reached a $16.5 billion deal with Tesla (TSLA) and is working on inking a similar deal with Apple (AAPL) . If these developments materialize, investors would start worrying about Taiwan Semi’s moat, but there is more to these deals than meets the eye.

Why This Has No Short-Term Impact on Taiwan Semi

There are quite a few reasons why this development shouldn’t worry Taiwan Semi (TSM) investors in the short term. For starters, AMD is seeking extra capacity by partnering with Samsung, and doesn’t intend to replace TSM. The Taiwan-based company’s most important nodes are fully booked as far into the future as 2028, with 100% utilization rates. In fact, the capacity that still hasn’t come online is already booked.

In other words, TSM is becoming a victim of its own success, and with limited capacity to serve the staggering CPU demand, it now sees competitors easily attracting companies that previously wouldn’t even bother with other manufacturers for their manufacturing needs.

That said, TSM still has a near monopoly on all the advanced nodes, and losing some wafer volume to Samsung while its own facilities are completely booked is something that is out of the company’s control anyway.

Where Could Taiwan Semi Possibly Lose?

While there is no short-term headwind for the company resulting from these developments, the question for long-term investors is whether the chipmaker loses pricing power in the long run. This is a reasonable risk, and if Samsung is able to deliver to the expectations of companies like Tesla, Apple, and Advanced Micro Devices, it would signal TSM’s loss of leadership and give a viable alternative to companies when they consider their future supply chains.

The AI compute economy is expanding, and the previous era of Taiwan Semi’s near monopoly may be giving way to a more competitive landscape.

About Taiwan Semi Stock

Taiwan Semiconductor Manufacturing Company is a Taiwan-based semiconductor company that tests, manufactures, sells, and packages integrated circuits and other chip products. The company provides a wide range of wafer fabrication processes and customer and engineering support services. Moreover, it is involved in mask manufacturing, research, chip design and development activities.

Over the past year, Taiwan Semiconductor delivered exceptional gains, surging about 137%. On the other side, the S&P 500 Index posted returns of around 29% during the same period. The stock significantly outperformed the broader index, delivering four times higher returns.

Taiwan Semi April Revenue Declines

The company reported April revenue of NT$410.73 billion or $13.1 billion USD, representing a 1.1% decline from March but a 17.5% increase year-over-year. Revenue for the first four months of 2026 climbed 29.9% compared to the same period last year to NT$1,544.83 billion.

Even though revenue declined, the company is on track to achieve its guided numbers for Q2. The slowdown in revenue suggests the growth pace is normalizing, which makes sense considering the company is operating at full capacity for its advanced nodes, with a significant amount of money going into capital expenditure.

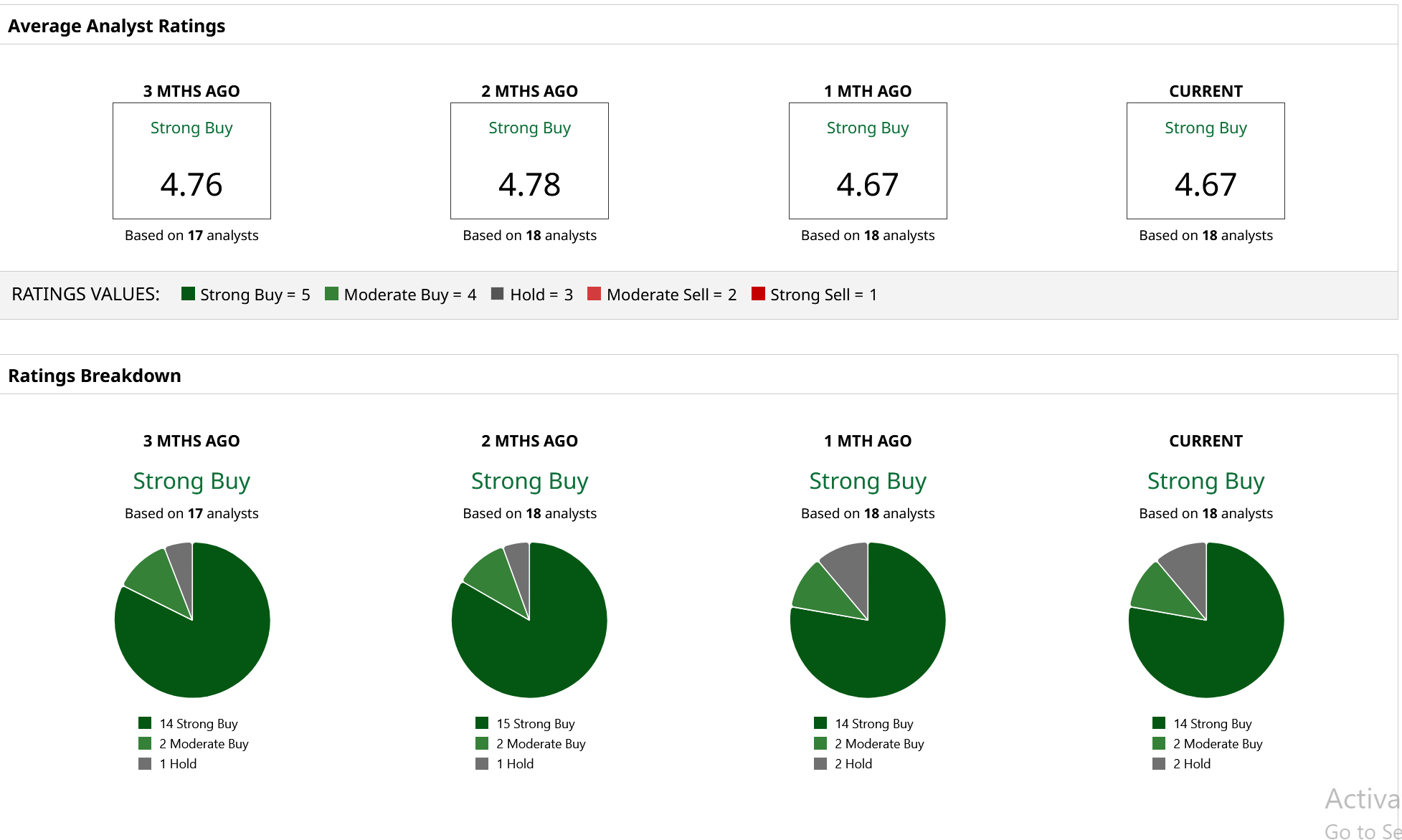

What Are Analysts Saying About Taiwan Semiconductor Stock

Bank of America Securities reaffirmed a Buy rating on Taiwan Semiconductor with a price target of $490 on April 23. A day earlier, Barclays analyst Simon Coles raised the firm’s price target on the stock from $450 to $470 while keeping a “Buy” rating. Needham also increased its price target from $375 to $480 and kept a “Buy” rating on the shares on April 16.

According to 18 Wall Street analysts covering the stock, it holds a consensus “Strong Buy” rating. Based on their estimates, the stock has a mean price target of $444.38, which offers 7% upside from the current levels. However, the highest price target of $550 suggests additional 32% upside from here on.

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20General%20Motors%20corporate%20sign%20by%20lindaparton%20via%20Adobe%20Stock.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Zoetis%20sign%20at%20their%20Canadian%20By%20JHVEPhoto.jpeg)

/Microsoft%20headquarters%20By%20Peter.jpeg)

/A%20SoFi%20logo%20on%20an%20office%20building%20by%20Tada%20Images%20via%20Shutterstock.jpg)