/The%20CoreWeave%20logo%20displayed%20on%20a%20smartphone%20screen_%20Image%20by%20Robert%20Way%20via%20Shutterstock_.jpg)

Artificial intelligence (AI) cloud infrastructure provider CoreWeave (CRWV) has once again found itself in the market spotlight, though this time for reasons investors did not welcome. After reporting first-quarter earnings on May 7, shares of the AI infrastructure specialist plunged 11.4% in the following trading session, as Wall Street shifted its focus from explosive growth to mounting concerns beneath the surface.

On paper, the quarter looked transformational. Revenue more than doubled year-over-year (YOY), contracted revenue backlog swelled toward an eye-popping $100 billion, and new agreements with AI powerhouses like Anthropic and Meta (META) further cemented CoreWeave’s rising importance in the AI race. The company continues to position itself as one of the key infrastructure providers powering the next wave of AI development. But investors were not entirely convinced.

Alongside the headline-grabbing growth, CoreWeave delivered weaker-than-expected second-quarter guidance, outlined even higher capital spending plans for fiscal 2026, and posted a bottom line that continued to deteriorate. Those concerns ultimately overshadowed the company’s rapid expansion story and triggered the sharp post-earnings sell-off. Still, the bigger picture remains hard to ignore. Even after the recent decline, CoreWeave stock is still up strongly in 2026, remaining a standout AI performer.

Nevertheless, is the latest pullback simply a temporary setback and potentially an attractive buying opportunity, or an early warning sign for investors?

About CoreWeave Stock

Founded in 2017 and based in New Jersey, CoreWeave has undergone a remarkable transformation, evolving from a small cryptocurrency mining startup into one of the most important players in the rapidly expanding AI economy. Unlike traditional cloud providers that offer broad, generalized services, CoreWeave operates as a GPU-native hyperscaler, with infrastructure specifically designed to support the enormous computing requirements of advanced AI models, machine learning workloads, and complex simulations.

The company combines high-performance computing power with deep technical expertise, enabling customers to accelerate development and manage demanding AI workloads more efficiently. Its platform has earned the trust of major AI labs, fast-growing startups, and large global enterprises seeking scalable AI infrastructure.

A major milestone came in March 2025, when CoreWeave officially debuted on the Nasdaq under the ticker CRWV. A key part of CoreWeave’s appeal is its ability to provide businesses with access to Nvidia’s (NVDA) cutting-edge GPUs without requiring them to invest billions into building their own infrastructure. This allows customers to access enormous computing power on demand while saving both time and capital.

By 2026, CoreWeave had firmly positioned itself at the heart of the AI ecosystem, supported by close partnerships with industry leaders including Nvidia, OpenAI, and Anthropic. With a market capitalization of $50.57 billion, the company has become one of Wall Street’s standout AI success stories, delivering massive gains that continue to capture investor attention.

Even after its sharp post-earnings pullback, CoreWeave stock remains one of the market’s standout AI winners. Shares have surged an impressive 60.17% in 2026, massively outperforming the broader S&P 500 Index ($SPX), which has gained 8.29% over the same period. The longer-term rally looks even more eye-catching, with CRWV skyrocketing 123.28% over the past 52 weeks, leaving the broader market’s 30.97% return far behind and reinforcing CoreWeave’s status as one of Wall Street’s hottest AI-driven momentum plays.

Digging Inside CoreWaves’s Q1 Earnings Report

CoreWeave’s first-quarter 2026 earnings report, released on May 7, painted the picture of a company growing at an extraordinary pace while simultaneously dealing with the enormous financial demands of the AI infrastructure boom. The AI cloud specialist generated quarterly revenue of $2.08 billion, marking a staggering 111.6% YOY jump from $982 million in the prior-year quarter. The explosive growth was driven by relentless demand for specialized AI cloud infrastructure and the successful rollout of additional data center capacity.

Then, revenue comfortably surpassed Wall Street expectations of $1.97 billion, reinforcing CoreWeave’s position as one of the fastest-growing companies in the AI ecosystem. Management described the quarter as the strongest bookings period in the company’s history, with revenue backlog surging to nearly $100 billion. That figure climbed almost 50% sequentially and nearly quadrupled from the same period last year, highlighting the scale of demand pouring into the business.

Further, CoreWeave strengthened its relationships with some of the biggest names in AI during the quarter. The company executed multiple new agreements with Meta, including a massive new $21 billion commitment signed in March. And, it entered into a multi-year agreement with Anthropic to support the development and deployment of the Claude family of AI models, further cementing its importance within the AI infrastructure ecosystem.

Still, beneath the eye-popping growth lies the harsh financial reality of competing in the generative AI infrastructure race. The business remains massively capital-intensive, and profitability pressures continue to mount as CoreWeave aggressively scales its operations. Net loss for the quarter widened sharply to $740 million, compared to a loss of $315 million in the same quarter of 2025. On an adjusted basis, the company posted a loss of $1.12 per share, worse than Wall Street’s expected loss of $0.91 per share.

Moreover, to fund its rapid expansion, CoreWeave continues to lean heavily on external financing as it races against much larger and more profitable cloud competitors. During the first quarter alone, the company raised $8.5 billion in new debt to support data center development. In addition, CoreWeave secured another $2 billion in equity financing tied to the expansion of its partnership with Nvidia.

Nevertheless, the company ended the quarter with a strong liquidity position, reporting more than $3.3 billion in cash, cash equivalents, restricted cash, and marketable securities as of March 31. Looking ahead, management reaffirmed its full-year revenue guidance of $12 billion to $13 billion and maintained adjusted operating income guidance of $900 million to $1.1 billion, citing strong execution and sustained customer demand.

However, investors appeared concerned about the near-term outlook. For the second quarter, CoreWeave projected revenue between $2.45 billion and $2.6 billion, falling short of Wall Street’s consensus estimate of $2.69 billion. For the full year, CoreWeave now expects CapEx to range from $31 billion to $35 billion, slightly raising the lower end of the range from its prior February forecast of $30 billion to $35 billion.

How Are Analysts Viewing CoreWeave Stock?

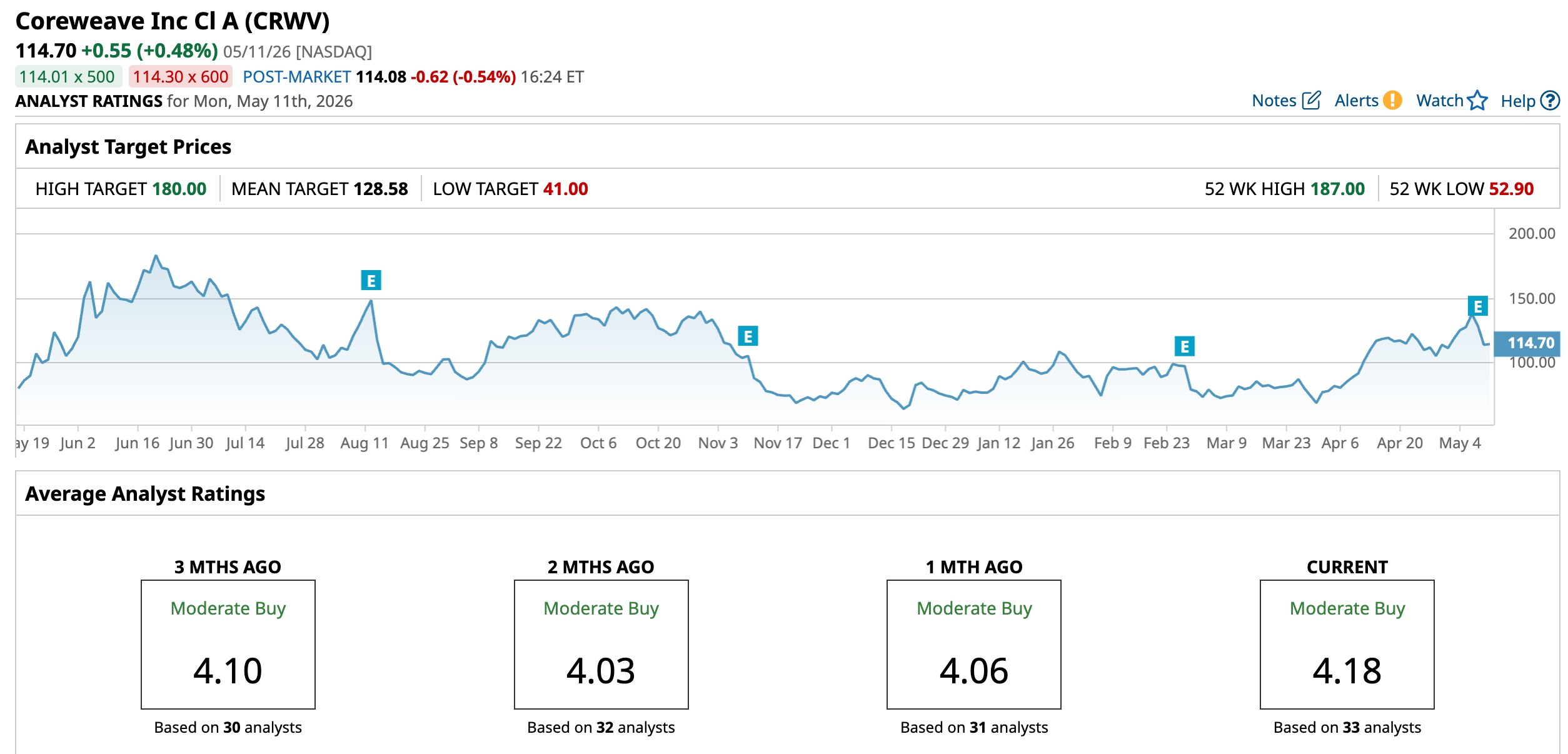

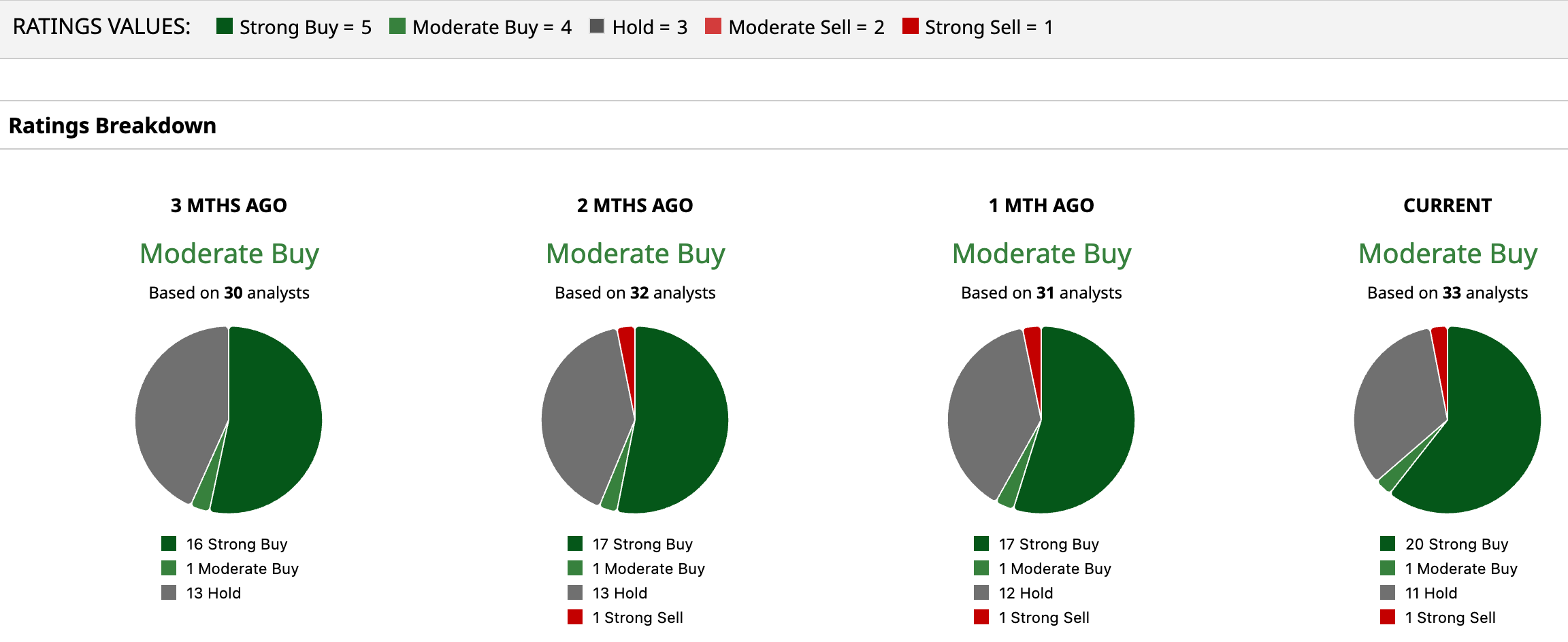

Despite recent volatility, Wall Street continues to see strong long-term potential in CoreWeave. The stock currently holds a consensus “Moderate Buy” rating, with analysts largely leaning bullish on the AI infrastructure leader. Among the 33 analysts covering the stock, 20 rate it a “Strong Buy,” one recommends “Moderate Buy,” 11 remain neutral with “Hold” ratings, and only one analyst stays bearish with a “Strong Sell” call.

Analysts also see meaningful upside ahead. The average price target of $128.58 implies potential gains of 12% from current levels, while the Street-high target of $180 suggests CoreWeave stock could surge as much as 56.9%, underscoring continued confidence in the company’s role at the center of the booming AI revolution.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)