/Stanley%20Black%20%26%20Decker%20Inc%20logo%20on%20building-by%20Jevanto%20Productions%20via%20Shutterstock.jpg)

Valued at a market cap of $12.6 billion, Stanley Black & Decker, Inc. (SWK) is a New Britain, Connecticut-based company that manufactures tools and outdoor solutions, providing high-performance equipment and innovative engineered fastening systems for builders, tradespeople, and DIYers.

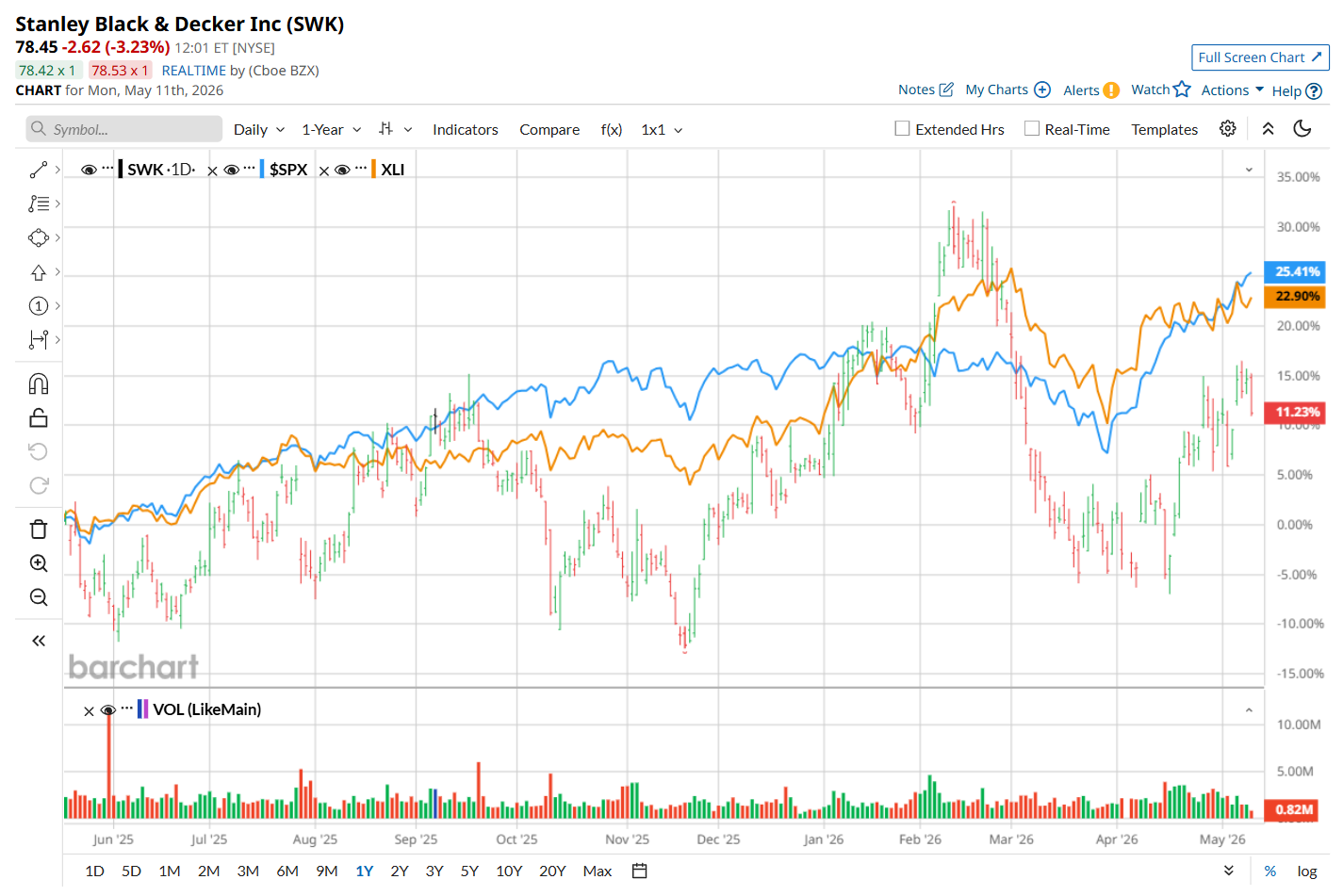

This industrial company has lagged the broader market over the past 52 weeks. Shares of SWK have soared 26.1% over this time frame, while the broader S&P 500 Index ($SPX) has rallied 30.6%. Moreover, on a YTD basis, the stock is up 6.4%, compared to SPX’s 8.1% rise.

Narrowing the focus, SWK has also underperformed the sector-focused Industrial Select Sector SPDR Fund’s (XLI) 28.2% uptick over the past 52 weeks and 12.5% surge on a YTD basis.

On Apr. 29, shares of SWK plunged 3.1% despite posting stronger-than-expected Q1 results. The company’s revenue increased 2.7% year-over-year to $3.85 billion, topping consensus estimates by 2.9%. Moreover, its adjusted EPS of $0.80 handily exceeded analyst estimates of $0.61. Despite the upbeat performance, investor sentiment remained pressured due to concerns surrounding profitability and margin performance. Management noted that the quarter’s revenue growth was supported by a successful outdoor products preseason and solid momentum in the Engineered Fastening segment, although continued volume weakness in North America and elevated cost inflation weighed on operating margins.

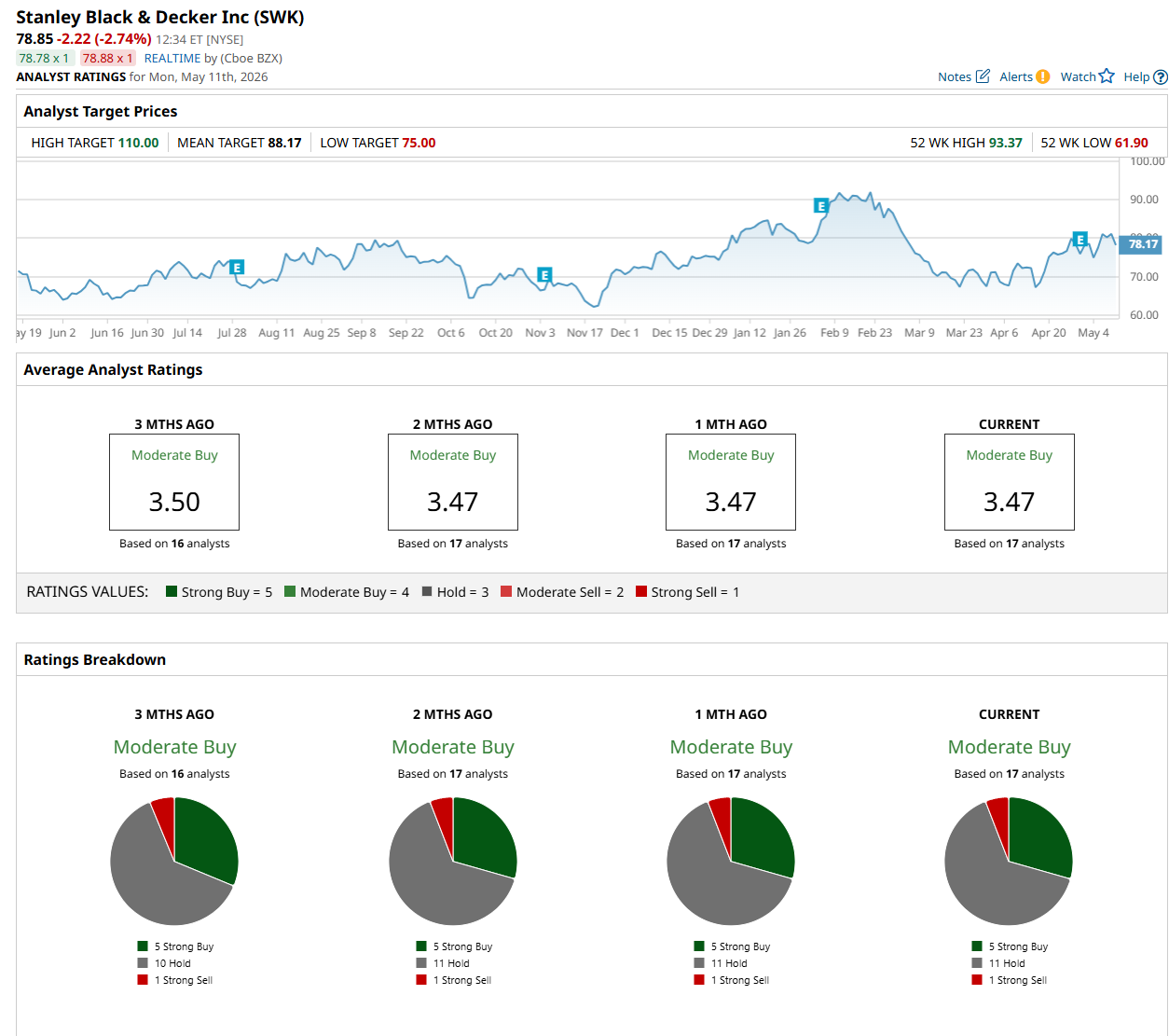

For the current fiscal year, ending in December, analysts expect SWK’s EPS to grow 13.1% year over year to $5.28. The company’s earnings surprise history is promising. It topped the consensus estimates in each of the last four quarters.

Among the 17 analysts covering the stock, the consensus rating is a "Moderate Buy,” which is based on five “Strong Buy,” 11 “Hold,” and one “Strong Sell” rating.

The configuration has remained fairly stable over the past three months.

On May 1, JPMorgan maintained an “Underweight” rating on SWK and raised its price target to $75.

The mean price target of $88.17 suggests an 11.8% premium to its current price levels, while its Street-high price target of $110 implies a 39.5% potential upside.

On the date of publication, Neharika Jain did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Accenture%20plc%20buiding%20with%20logo-by%20JHVEPhoto%20via%20iStock.jpg)