/State%20Street%20Corp_%20HQ%20building-by%20JHVEPhoto%20via%20iStock.jpg)

State Street Corporation (STT), headquartered in Boston, Massachusetts, provides a range of financial products and services to institutional investors worldwide. Valued at $36.8 billion by market cap, the company’s products and services include custody, accounting, administration, daily pricing, international exchange services, cash management, financial asset management, securities lending, and investment advisory services.

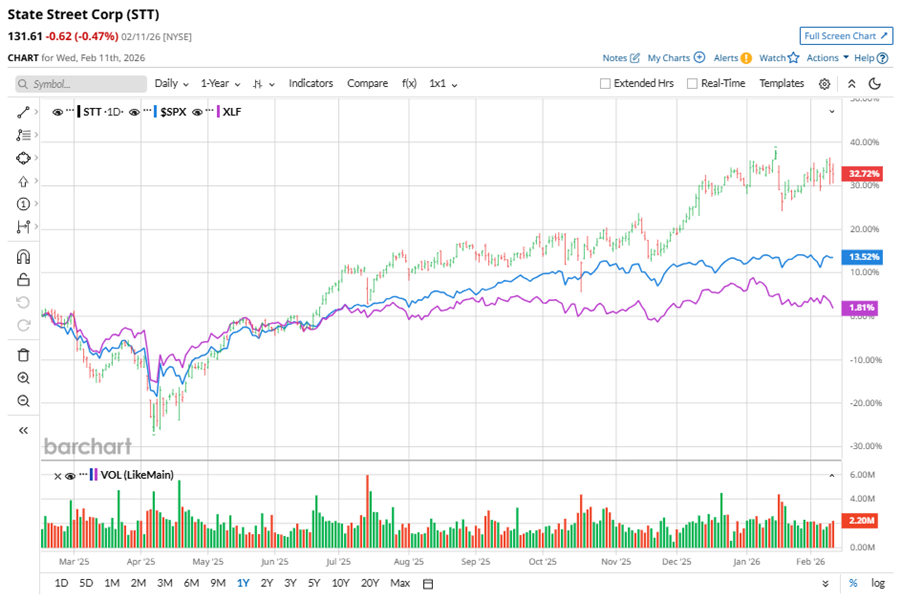

Shares of this financial giant have outperformed the broader market over the past year. STT has gained 33.5% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 14.4%. In 2026, STT stock is up 2%, surpassing the SPX’s 1.4% rise on a YTD basis.

Zooming in further, STT’s outperformance is also apparent compared to Financial Select Sector SPDR Fund’s (XLF). The exchange-traded fund has gained about 2.3% over the past year. Moreover, the stock’s returns on a YTD basis outshine the ETF’s 3.7% losses over the same time frame.

STT's growth was driven by robust fee income from investment services and asset management, alongside operating leverage improvements. The company launched new digital asset platforms and saw double-digit growth in private markets servicing fees, though software and processing fees declined due to a shift to cloud-based solutions. CEO Ron O'Hanley emphasized investments in AI, digital transformation, and private markets expansion will drive medium-term growth, with productivity savings offsetting most cost increases.

On Jan. 16, STT shares closed down more than 6% after reporting its Q4 results. Its revenue stood at $3.7 billion, up 7.5% year over year. The company’s adjusted EPS came in at $2.42, down 1.6% from the year-ago quarter.

For the current fiscal year, ending in December, analysts expect STT’s EPS to grow 12.1% to $11.55 on a diluted basis. The company’s earnings surprise history is impressive. It beat the consensus estimate in each of the last four quarters.

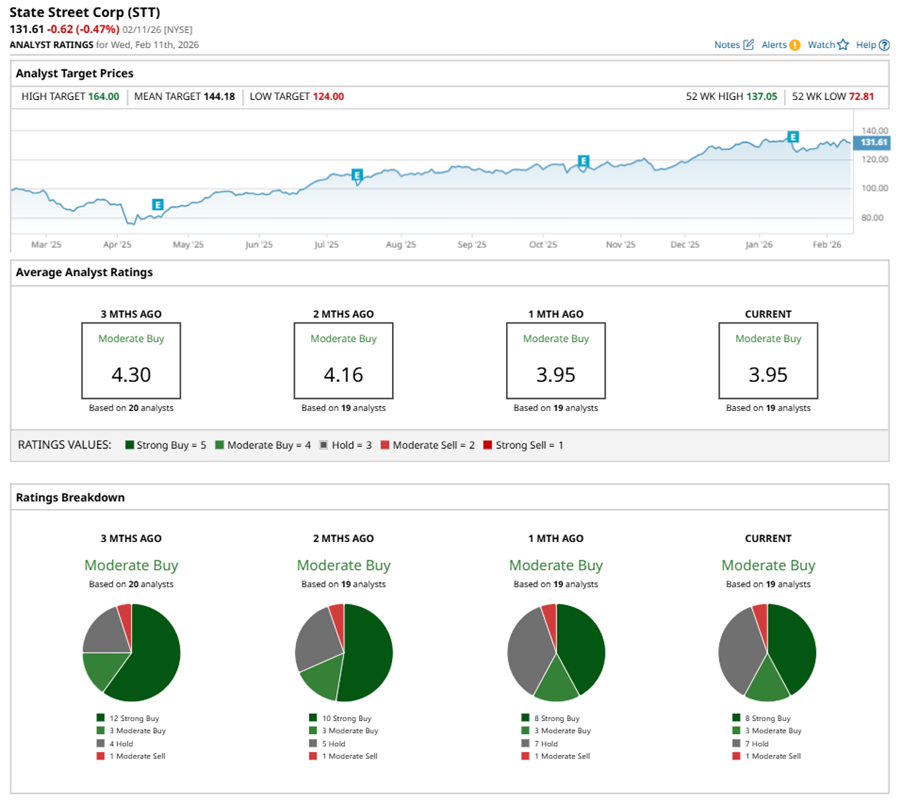

Among the 19 analysts covering STT stock, the consensus is a “Moderate Buy.” That’s based on eight “Strong Buy” ratings, three “Moderate Buys,” seven “Holds,” and one “Moderate Sell.”

This configuration is less bullish than two months ago, with 10 analysts suggesting a “Strong Buy.”

On Jan. 29, Morgan Stanley (MS) analyst Betsy Graseck maintained a “Buy” rating on STT and set a price target of $164, the Street-high price target, implying a potential upside of 24.6% from current levels.

The mean price target of $144.18 represents a 9.6% premium to STT’s current price levels.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/NVIDIA%20Corp%20video%20chip-by%20Antonio%20Bordunovi%20via%20iStock.jpg)

/Space/Rocket%20lift%20off%20by%20Alones%20via%20Shutterstock.jpg)

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)