Pennsylvania-based Hershey Company (HSY) is one of the largest confectionery and snack food companies in North America, best known for its chocolate brands, candies, and salty snacks. The company has a market capitalization of $37.8 billion, and it has built a dominant presence in the U.S. sweets market through a portfolio of widely recognized consumer brands.

Shares of the company have surged 10.9% over the past 52 weeks and 2.8% on a YTD basis. In comparison, the S&P 500 Index ($SPX) has returned 30.3% over the past year and risen 7.2% in 2026.

Narrowing the focus, HSY has outperformed the State Street Consumer Staples Select Sector SPDR ETF’s (XLP) 3.1% rise over the past 52 weeks but has trailed behind the ETF’s 8.1% rally this year.

On Apr. 30, Hershey released its Q1 FY2026 results, delivering consolidated net sales growth 10.6% year over year to $3.10 billion. Its adjusted EPS rose 12.4% to $2.35.

However, investors remained cautious as the company continued to grapple with soaring cocoa costs, softer consumer spending, and intense competition across the confectionery category. Sales volumes declined as increasingly price-sensitive shoppers pulled back on candy purchases in parts of North America. Additionally, management warned that elevated commodity inflation, particularly in cocoa prices, would continue to pressure margins throughout fiscal 2026. As a result, its shares dipped 1.8% following the earnings release.

For the fiscal year ending in December 2026, analysts expect HSY to report a 33.9% year-over-year growth in adjusted EPS to $8.45. The company has a good earnings surprise history. It has surpassed the Street’s bottom-line estimates in each of the past four quarters.

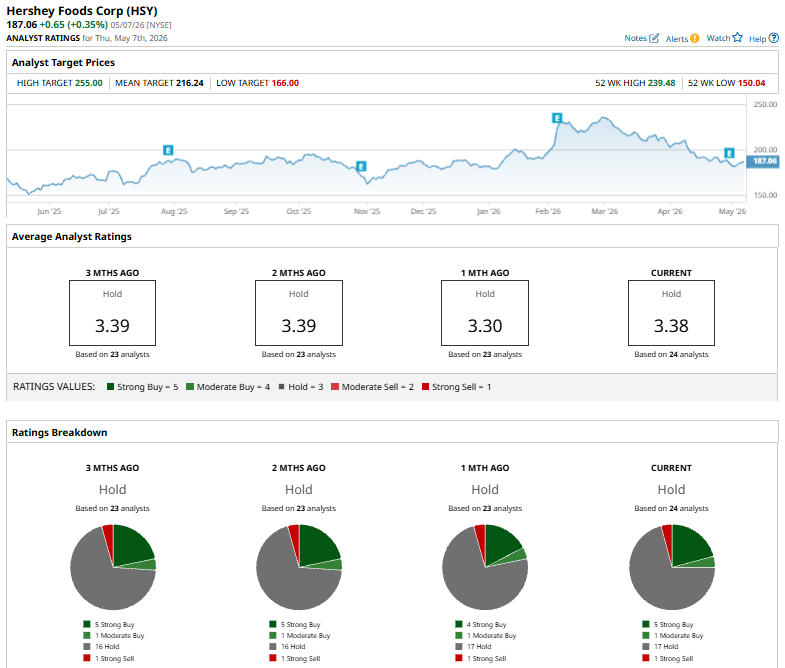

HSY has a consensus “Hold” rating overall. Of the 24 analysts covering the stock, opinions include five “Strong Buys,” one “Moderate Buy,” 17 “Holds,” and one “Strong Sell.”

The configuration is bullish than a month ago when the stock had four “Strong Buy” suggestions.

On May 4, DA Davidson lowered its price target on Hershey to $208 from $230 while maintaining a “Neutral” rating following the company’s Q1 results. The firm cited intense competitive pressure and continued strain on consumers as key concerns weighing on the business.

HSY’s mean price target of $216.24 implies a 15.6% premium over current market prices. Its Street-high target of $255 suggests an 36.3% upside potential from current price levels.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)

/A%20game%20controller%20in%20front%20of%20a%20Roblox%20computer%20screen%20by%20Miguel%20Lagoa%20via%20Shutterstock.jpg)

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)