/Home%20Depot%2C%20Inc_%20location%20by-hapabapa%20via%20iStock.jpg)

Atlanta, Georgia-based The Home Depot, Inc. (HD) operates as a home improvement retailer. Valued at $314.2 billion by market cap, the company offers a wide range of building materials, home improvement, lawn, and garden products, as well as provides DYI ideas, installation, repair, and other services.

Shares of this world's largest home improvement specialty retailer have underperformed the broader market over the past year. HD has declined 10.1% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 31.4%. In 2026, HD stock is down 6.1%, compared to the SPX’s 7.6% rise on a YTD basis.

Narrowing the focus, HD’s underperformance is also apparent compared to iShares U.S. Home Construction ETF (ITB). The exchange-traded fund has gained about 4.8% over the past year. Moreover, the ETF’s 1% dipon a YTD basis outshines the stock’s losses over the same time frame.

HD underperformed due to macro and housing headwinds, partially offset by easing oil prices. While lower oil reduced inflation pressure and lifted retail sentiment, housing turnover stayed near historic lows since 2023, hurting project-related demand. Management noted customer concerns around inflation, job security, and financing costs. In addition, results reflected one fewer operating week and a cautious consumer backdrop.

For fiscal 2026, ending in January, analysts expect HD’s EPS to grow 2.3% to $15.02 on a diluted basis. The company’s earnings surprise history is disappointing. It missed the consensus estimate in three of the last four quarters while beating the forecast on another occasion.

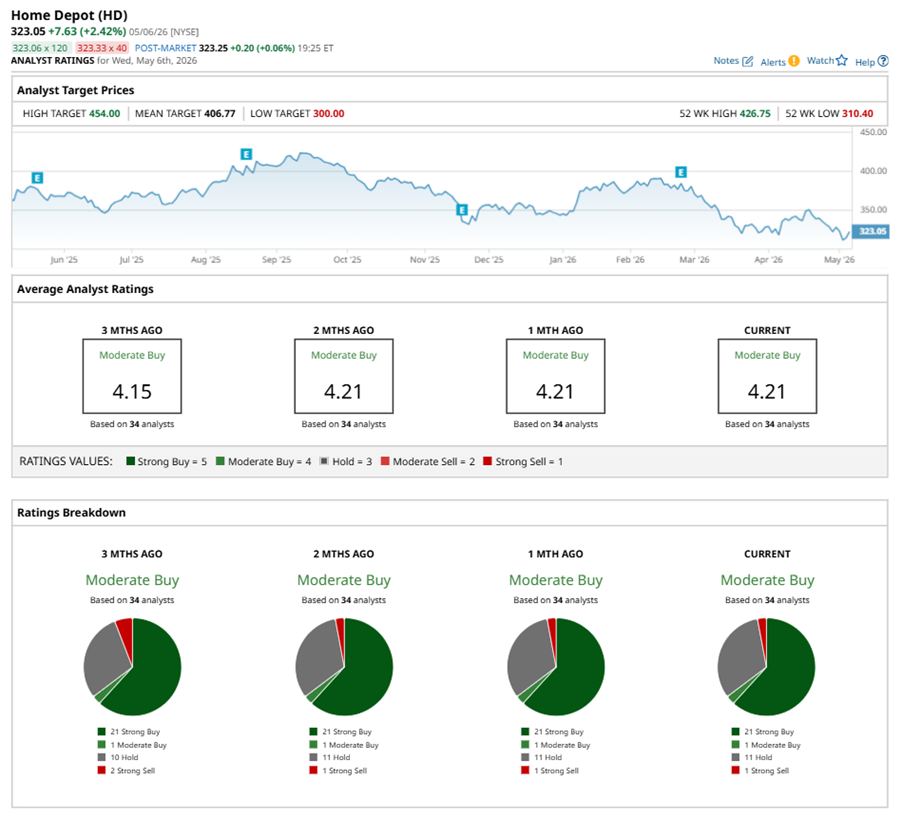

Among the 34 analysts covering HD stock, the consensus is a “Moderate Buy.” That’s based on 21 “Strong Buy” ratings, one “Moderate Buy,” 11 “Holds,” and one “Strong Sell.”

This configuration is less bearish than three months ago, with two analysts suggesting a “Strong Sell.”

On May 5, Bank of America Corporation (BAC) reinstated coverage of HD with a “Buy” rating and $374 price target, implying a potential upside of 15.8% from current levels.

The mean price target of $406.77 represents a 25.9% premium to HD’s current price levels. The Street-high price target of $454 suggests a notable upside potential of 40.5%.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/Green%20hydrogen%20by%20Scharfsinn%20via%20Shutterstock.jpg)

/Abbvie%20Inc%20HQ%20photo-by%20vzphotos%20via%20iStock.jpg)