April 2026 was a good month for dividend investors. Parker Hannifin (PH) raised its quarterly cash dividend 11% to $2.00 per share, marking its 304th straight quarterly dividend, with payment set for June 5, 2026. Johnson & Johnson (JNJ) also kept its streak going, raising its quarterly payout by 3.1% from $1.30 to $1.34 per share for its 64th straight year of dividend growth. Southern Company (SO) did the same, posting its 25th straight annual dividend increase and taking its annualized payout to $3.04 per share. In simple terms, plenty of companies spent April showing investors that dividends still matter.

American Water Works (AWK) was part of that group. On April 29, 2026, the company announced a quarterly cash dividend of $0.8950 per share, up 8.2% from the prior quarter, payable June 2, 2026, to shareholders of record as of May 12, 2026. That increase fits with management’s long-term goal of growing the dividend by 7% to 9% a year.

Still, the stock has not really acted like a winner. AWK has lagged both the S&P 500 ($SPX) and the Dow ($DOWI) over multiple recent periods, even though the company’s core business has stayed fairly steady. So is this dividend hike a sign to buy the dip, or is the market staying cautious for a reason? Let’s find out.

The Numbers Behind American Water Works

American Water Works is the biggest publicly traded water and wastewater utility in the U.S., built around regulated operations that bring in steady, predictable cash flow. Over the past 52 weeks, AWK stock is down 15%, and it’s off 4% year-to-date (YTD).

At today’s price, AWK trades at a forward P/E of 20.90x, above the sector average of 18.81x, so the market is still willing to pay a premium for that stability.

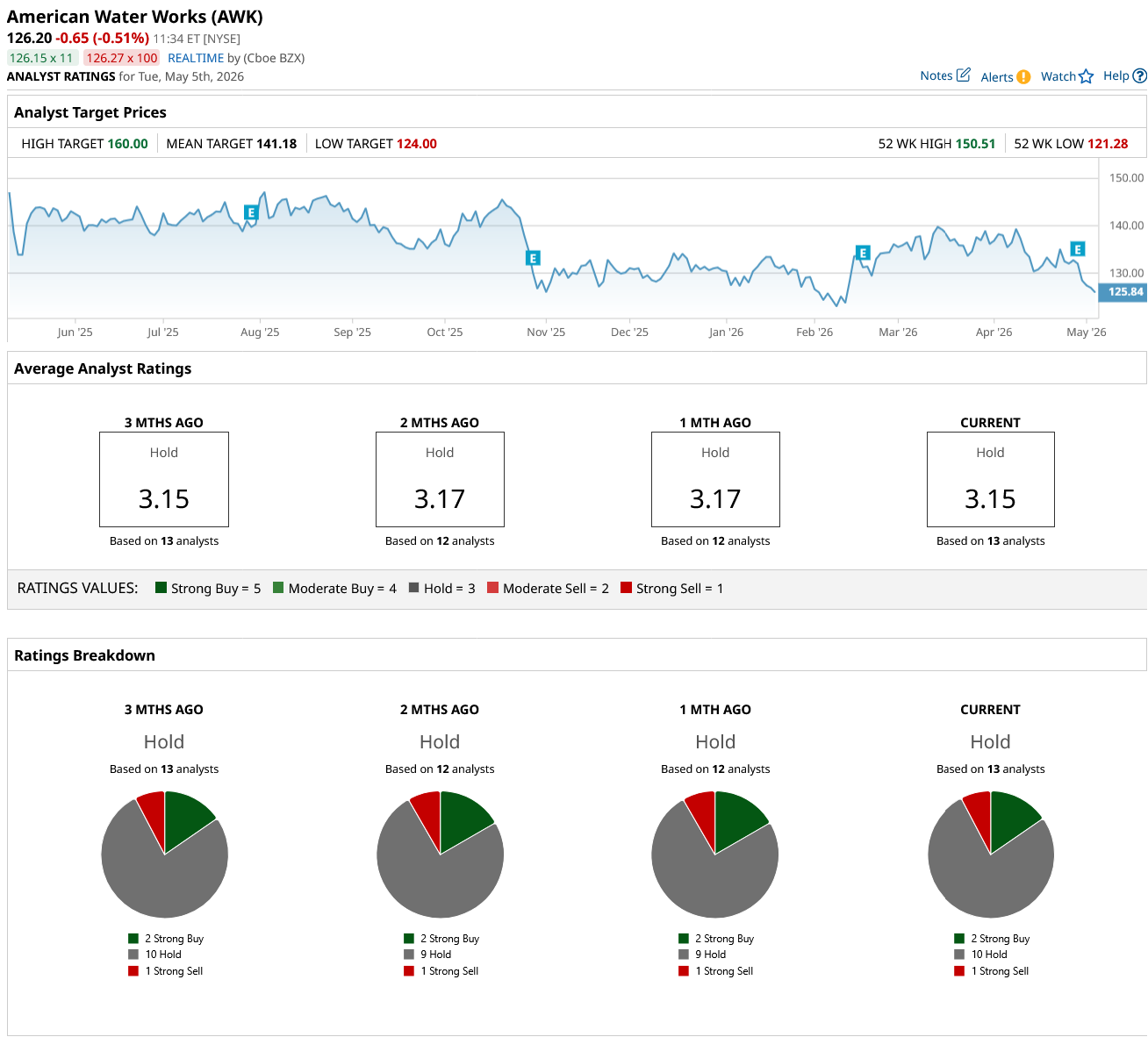

The income side is key. American Water recently raised its dividend by 8%, marking 19 straight years of increases. The stock yields about 2.60%, below the utilities average of 3.75%, but that comes with a reasonable forward payout ratio of 56.83% and regular quarterly checks. The most recent dividend was $0.827, paid on Feb. 10, 2026.

In the first quarter of 2026, GAAP earnings were $1.00 per share, down slightly from $1.05 a year earlier. Adjusted EPS was $1.01, versus $1.02 in the prior-year quarter, after stripping out costs tied to the proposed Essential Utilities merger and interest income from the repaid HOS secured seller note. Management still reaffirmed full-year 2026 EPS guidance of $6.02 to $6.12 and its long-term targets, and it raised $700 million of 5.200% senior notes due 2036 in April to help fund ongoing growth.

The Long-Term Drivers Supporting the Bull Case

American Water Works and Essential Utilities have already won approval from the Kentucky Public Service Commission for their all-stock merger after shareholders signed off in February 2026.

The combined company is expected to serve more than 4.7 million water and wastewater connections and over 740,000 gas customers under the American Water name, with the deal aimed to close by the end of the first quarter of 2027, pending federal and other state approvals. That would noticeably widen American Water’s regulated footprint and customer base, giving it more stable earnings over time.

The growth story is still about infrastructure. In West Virginia, the company is working on a $550,000 project to replace 1,020 feet of aging pipe, part of a larger plan to put more than $134 million to work across the state in 2026. Those kinds of regulated projects support future rate hikes and also help local economies, with studies showing every $1 million spent on water infrastructure can create about 10 jobs.

Funding is another key piece. In Pennsylvania, American Water secured $25.87 million in grants and low-interest loans from PENNVEST for projects including the Griffin Dam rehab. With interest rates starting at just 1%, that money helps keep financing costs down while the company upgrades its systems and improves reliability.

Analysts Weigh AWK’s Next Move

Analysts are looking for earnings of $1.51 for the June 2026 quarter, up from $1.48 a year earlier, and $2.11 for the September 2026 quarter, versus $1.94 in the prior-year period. For the full year, the consensus calls for $6.09 in 2026 earnings, up from $5.64. That translates to estimated year-over-year (YoY) growth rates of 2.03% for the current quarter, 8.76% for the next quarter, and 7.98% for fiscal 2026.

In January 2026, Campanella reiterated his “Sell” rating on AWK and kept a $122 price target, a notably more cautious stance than the broader Street view. Wells Fargo has taken a more measured approach. After lowering its target from $142 to $126 in January, the firm raised it to $131 on April 21, just ahead of the first-quarter report, while maintaining an “Equal Weight” rating.

That broader stance remains cautious. The 13 analysts covering AWK currently rate it a consensus “Hold,” with an average price target of $141.18. Based on current share price levels, that implies a downside of about 11%.

Conclusion

AWK looks more like a steady buy than an obvious bargain right now. The new 8.2% dividend hike, reaffirmed 2026 EPS guidance of $6.02 to $6.12, and long-term dividend growth target of 7% to 9% all support the case that the business is still executing even if the stock has lagged. With analysts sitting at a “Hold” and an implied upside of about 11%, my base case is that shares are more likely to grind modestly higher than stage a sharp rally in the near term, which makes AWK stock look best suited for patient investors who want dependable income and gradual appreciation rather than quick upside.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/AI%20technology%20concept%20by%20NMStudio789%20via%20Shutterstock.jpg)