/Emerson%20Electric%20Co_%20sign%20on%20building-by%20SNEHIT%20PHOTO%20via%20Shutterstock.jpg)

With a market cap of $77.2 billion, Emerson Electric Co. (EMR) is a global industrial technology company focused on automation solutions, control systems, and industrial software. The Missouri-based industrial giant provides equipment and digital tools that help businesses improve efficiency, reliability, and performance across complex operations. The company serves a broad range of industries, including energy, chemicals, power, manufacturing, and life sciences, where its systems are often mission-critical.

EMR has surged and soared 25.1% over the past year, slightly trailing the S&P 500 Index’s ($SPX) 26.6% gains. In 2026, EMR climbed 2.1%, compared to the index’s 5.2% rise.

Narrowing the focus, EMR has also lagged behind the State Street Industrial Select Sector SPDR Fund’s (XLI) 27.1% gains over the past year and 10.2% rally in this year.

Emerson Electric has trailed the broader market over the past year primarily due to its cyclical industrial exposure and ongoing portfolio transformation. Demand in key end markets such as energy, manufacturing, and process industries has been uneven, leading to more moderate growth than the strong rally seen in technology and AI-driven stocks. Additionally, Emerson has been in the midst of a strategic shift toward automation and software, including divestitures and acquisitions, which has created near-term uncertainty and integration risk. While this repositioning is aimed at improving long-term growth and margins, it has temporarily weighed on investor sentiment.

For fiscal 2026, which ends in September, analysts expect EMR to deliver an adjusted EPS of $6.50, up 8.3% year over year. Further, the company has a solid earnings surprise history. It has surpassed the Street’s bottom-line estimates in each of the past four quarters.

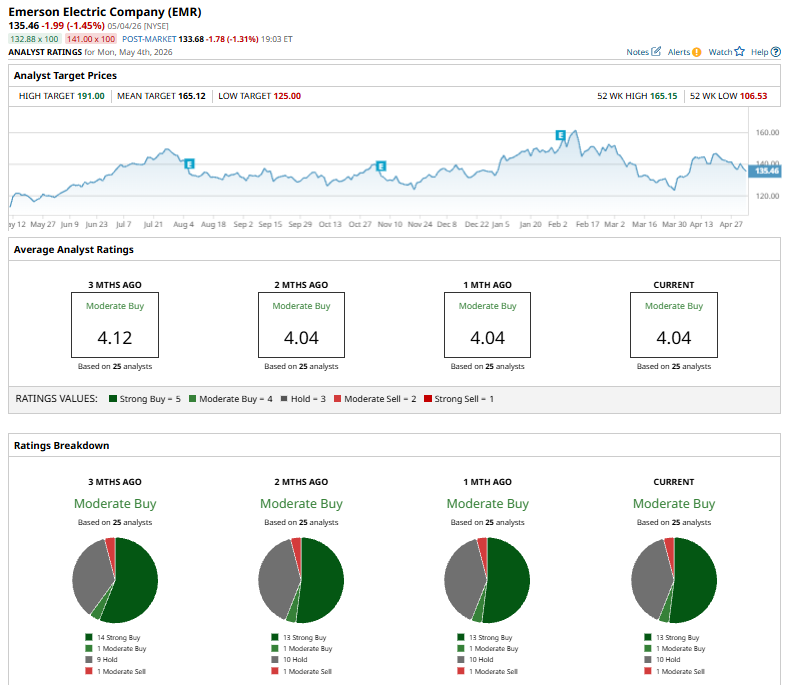

Among the 25 analysts covering the EMR stock, the consensus rating is a “Moderate Buy.” That’s based on 13 “Strong Buys,” one “Moderate Buy,” ten “Holds,” and one “Moderate Sell.”

This configuration is bearish than three months ago, when 14 analysts gave “Strong Buy” recommendations.

On Mar. 31, Jefferies upgraded Emerson to “Buy” from “Hold” and raised its price target to $175 from $160, citing improving fundamentals. The firm expects strong order momentum across key growth segments to drive a pickup in earnings, with growth accelerating from low single digits in early fiscal 2026 to low double digits by late FY2026 and into FY2027.

EMR’s mean price target of $165.12 suggests an 21.9% upside potential. Meanwhile, the Street-high target of $191 represents a notable 41% premium to current price levels.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Western%20Digital%20Corp_%20logo%20on%20sign-by%20360b%20via%20Shutterstock.jpg)

/PayPal%20Holdings%20Inc%20sign%20on%20building-%20by%20Sundry%20Photography%20via%20Shutterstock.jpg)

/Microsoft%20Corporation%20logo%20on%20sign-by%20Jean-Luc%20Ichard%20via%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)