/Western%20Digital%20Corp_%20logo%20on%20sign-by%20360b%20via%20Shutterstock.jpg)

Western Digital Corporation (WDC), with a market cap of $150 billion, is a leading data storage technology company that designs, manufactures, and sells devices used to store, manage, and access digital data. Its products are widely used across consumer electronics, enterprise data centers, and cloud infrastructure.

Shares of the storage solution specialist have significantly outperformed the broader market over the past year, surging a whooping 889.8% compared to the S&P 500 Index’s ($SPX) 26.6% gain. The stock continues to outshine the market, with a remarkable 156.8% YTD returns versus the SPX's 5.2% increase.

Narrowing the focus, WDC has also surpassed the State Street Technology Select Sector SPDR ETF’s (XLK) 49.6% uptick over the past year and 12.6% rise in 2026.

Western Digital has significantly outpaced the broader market over the past year, driven by its positioning as a key beneficiary of the AI and cloud infrastructure boom. Explosive demand for high-capacity storage from hyperscalers and data centers has fueled sharp growth in both revenue and profitability, pushing the stock dramatically higher. Unlike purely speculative AI plays, WDC’s rally has been supported by tangible fundamentals, strong earnings growth, expanding margins, and rising pricing power in HDDs.

Western Digital delivered a standout fiscal Q3 2026 results on Apr. 30, and its shares popped 5.3%. Revenue rose 45% year over year to $3.34 billion, while adjusted EPS surged 97% to $2.72, with both metrics beating expectations. Profitability improved materially, with non-GAAP gross margins expanding to 50.5% and operating margins to 38.6%, driven by a richer mix of high-capacity drives, disciplined pricing, and cost efficiencies.

For the current fiscal year, ending in June, analysts expect WDC’s earnings per share to rise 91.6% year over year to $8.68. Moreover, the company’s earnings surprise history is solid. It exceeded the consensus estimate in each of the last four quarters.

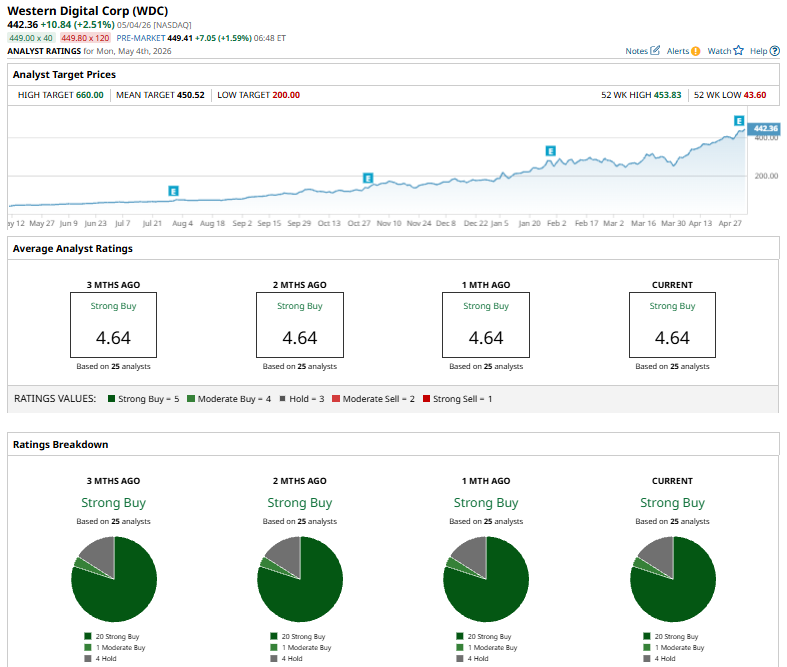

Western Digital’s stock holds a consensus “Strong Buy” rating. Among the 25 analysts covering the stock, 20 rate it as a "Strong Buy," one gives a “Moderate Buy,” and four recommend a "Hold."

On May 1, UBS raised its price target on Western Digital to $375 from $350, while maintaining a “Neutral” rating. The upgrade follows another beat-and-raise quarter, supported by tight HDD supply and improving pricing power.

However, despite strong near-term execution and guidance, UBS remains cautious on the stock. The firm flagged concerns around the sustainability of elevated margins and whether current valuations are justified, particularly as investors debate HDDs’ long-term growth potential versus the more cyclical nature of memory markets.

With a mean price target of $450.52, WDC is expected to soar 1.8% from its current level. Moreover, the Street-high target of $660 suggests a significant upside potential of 49.2%.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/PayPal%20Holdings%20Inc%20sign%20on%20building-%20by%20Sundry%20Photography%20via%20Shutterstock.jpg)

/Microsoft%20Corporation%20logo%20on%20sign-by%20Jean-Luc%20Ichard%20via%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)