Oklahoma-based Devon Energy Corporation (DVN) is an independent upstream energy company focused on the exploration and production of oil, natural gas, and natural gas liquids across major U.S. shale basins, including the Permian, Anadarko, and Eagle Ford. With a market cap of $31.7 billion, Devon focuses on finding, developing and producing oil, natural gas, and natural gas liquids (NGLs) primarily onshore in the United States across multiple prolific basins such as the Delaware Basin, Eagle Ford, Anadarko Basin, Powder River Basin and Williston Basin.

The energy giant has outperformed the broader market over the past year, soaring 63.2% over the past 52 weeks compared to the S&P 500 Index’s ($SPX) 28.3% surge. In 2026, DVN climbed 39.5%, surpassing the index’s 4.2%.

Zooming in, Devon’s run has been even more impressive, outperforming the iShares U.S. Oil & Gas Exploration & Production ETF’s (IEO) 46.6% rise over the past 52 weeks and 37% rise on a YTD basis.

On Apr. 29, Devon Energy shares rose more than 3% as part of a broad rally across energy stocks, following WTI crude oil's surge over 6% to a three-week high that lifted sentiment across the sector.

For FY2026 ending in December, analysts expect DVN to report a 35.5% year-over-year rise in earnings to $5.31 per share. Moreover, the company has exceeded the Street’s bottom-line estimates in three of the past four quarters, while missing on another occasion.

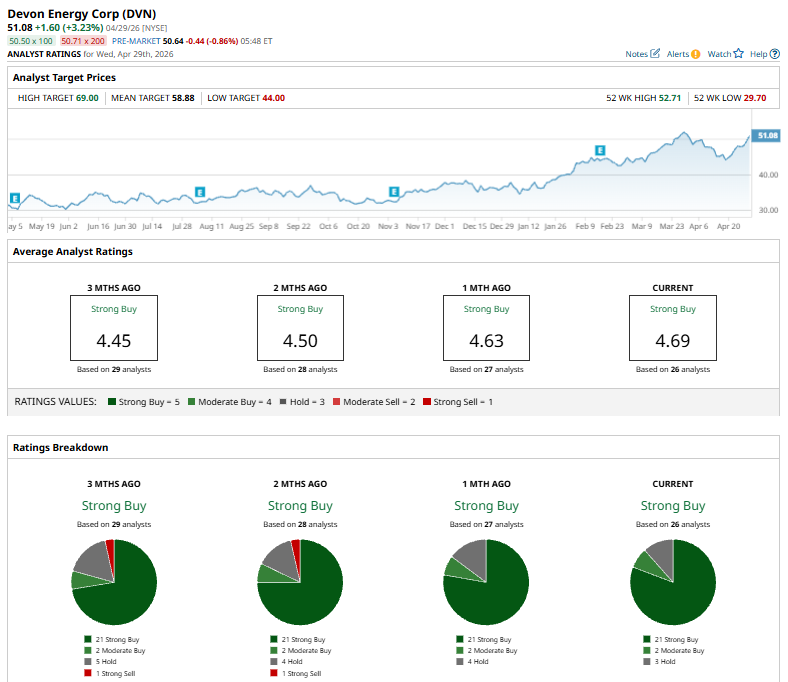

DVN holds a consensus “Strong Buy” rating overall. Among the 26 analysts covering the stock, opinions include 21 “Strong Buys,” two “Moderate Buys,” and three “Holds.”

On April 22, Scotiabank raised its price target on Devon Energy to $46 from $41, while maintaining a “Sector-Perform” rating. The update came as part of a broader revision of estimates across U.S. integrated oil, refining, and large-cap E&P names under coverage. The firm maintains a mixed stance on the sector, projecting earnings above consensus for E&P companies but below expectations for independent refiners. Looking ahead, Scotiabank expects investor focus to shift toward whether recent volatility in oil markets will lead to changes in industry activity levels in 2026 and beyond.

DVN’s mean price target of $58.88 indicates a 15.3% premium to current price levels, while its Street-high target of $69 suggests a staggering 35.1% upside potential.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)