/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)

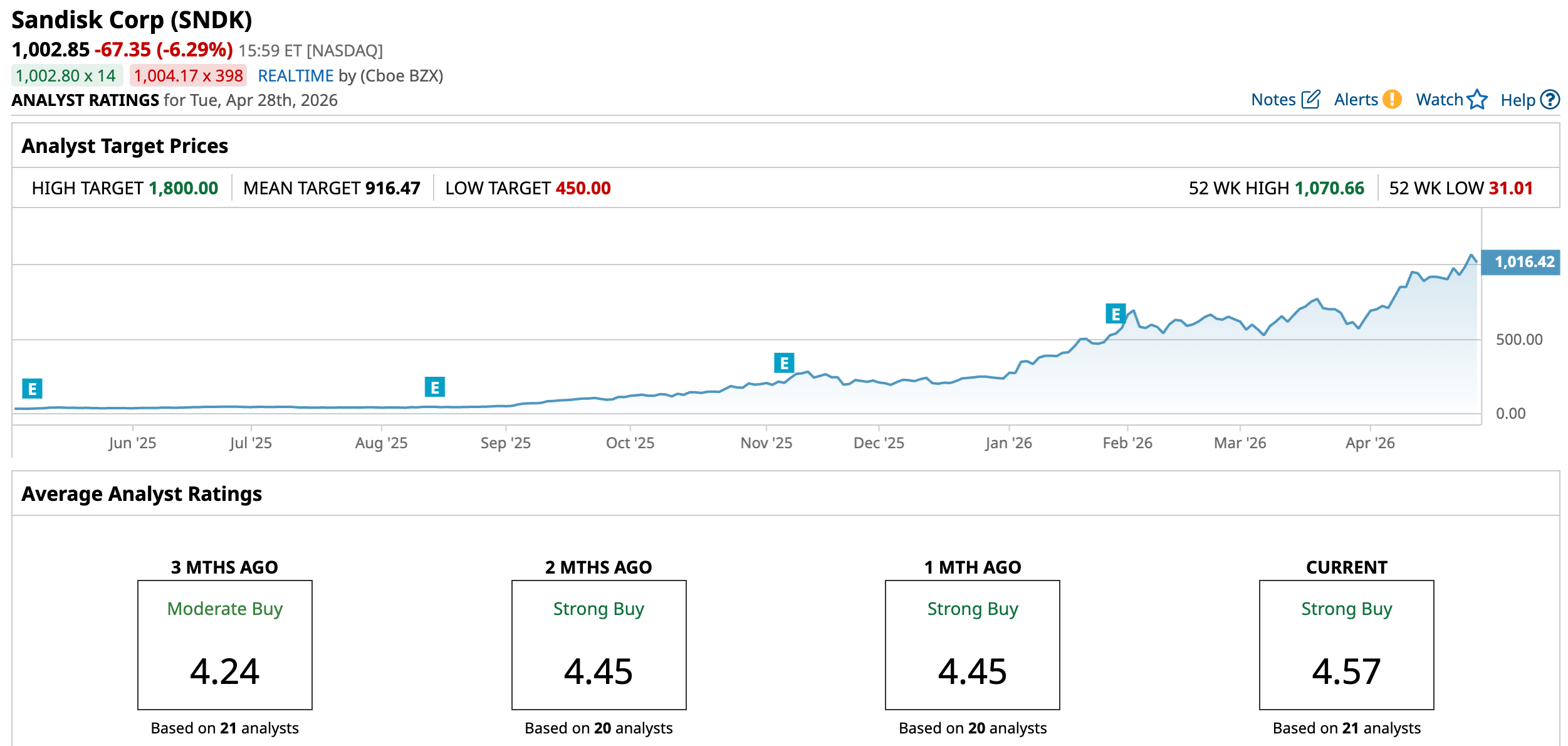

Sandisk (SNDK) stock has extended its explosive rally into 2026, climbing 332.7% year-to-date, as investor sentiment remains optimistic on companies benefitting from the rapid buildout of AI infrastructure. The expansion of AI workloads has significantly increased the demand for high-performance data storage, particularly NAND-based solutions. This durable demand is benefiting Sandisk across its portfolio, including solid-state drives (SSDs), embedded storage, removable media, USB drives, and component-level offerings.

Heading into its Q3 earnings release, scheduled for April 30, Sandisk appears well-positioned to sustain this momentum. Demand dynamics remain favorable. Moreover, a tight NAND supply environment is supporting higher average selling prices, pushing its margins and earnings higher. The expected increase in volume and higher pricing create a constructive operating backdrop for Sandisk that could translate into solid earnings growth in Q3.

Adding to its investment appeal, SNDK stock remains compelling on valuation despite the significant run-up. This indicates further upside potential. Moreover, Sandisk has seen its stock rise following three of its last four quarterly reports, including a 6.9% gain after its Q2 release.

Sandisk to Deliver Massive Growth in Q3

SanDisk’s Q3 will reflect strong operating momentum, supported by solid demand tailwinds from AI infrastructure expansion. The company’s products are seeing broad-based adoption as hyperscalers, enterprise and edge data centers, and OEMs continue to scale storage capacity to support increasingly data-intensive workloads.

In the second quarter, solid product adoption drove a 61% year-over-year (YOY) increase in net revenue. The growth came from higher prices and increased sales volume. On average, the price per gigabyte rose 36%, while total shipments (measured in exabytes) grew by 22%. Together, these figures suggest that demand is strong and supply in the NAND market is tightening.

Looking ahead to the third quarter results, these favorable conditions are likely to continue. Revenue is projected to reach $4.4 billion and $4.8 billion, a sharp increase from $1.70 billion a year ago. The company’s revenue will benefit from accelerating enterprise SSD demand.

Supply conditions are also likely to boost Sandisk’s Q3 numbers. The company expects the NAND market to be even more undersupplied than in the previous quarter, which should help keep prices elevated. Notably, higher pricing has been a key driver of its revenue growth and profit margins.

Sandisk’s data center business is witnessing strong growth. In the second quarter, revenue from this segment rose 76%, while shipments increased 90%. This momentum is expected to carry over into Q3 as cloud providers and enterprises aggressively expand their storage capacity.

The company’s management expects adjusted gross margin to rise to 65%-67% in the third quarter, up from 51.1% in the previous quarter. This reflects stronger pricing.

Thanks to the higher revenue and margins, Sandisk’s earnings are expected to grow significantly. The company has guided for adjusted earnings per share (EPS) of $12 to $14, with analysts estimating $13.4. Notably, SanDisk has exceeded analysts’ EPS expectations by a wide margin in the past three consecutive quarters, and this trend could continue in Q3.

What’s Ahead for Sandisk Stock?

Sandisk’s Q3 will reflect strong AI-driven demand expansion, tightening NAND supply, and strong pricing. While the stock’s significant rally may suggest that much of the optimism is already priced in, its valuation suggests further room to run.

Sandisk stock is trading at a forward price-to-earnings multiple of 25.38 times, which is compelling given its continued strong revenue and earnings growth. Sandisk’s EPS is projected to grow significantly in fiscal 2026. Moreover, analysts expect its bottom line to jump by more than 129% in fiscal 2027, despite tough YOY comparisons.

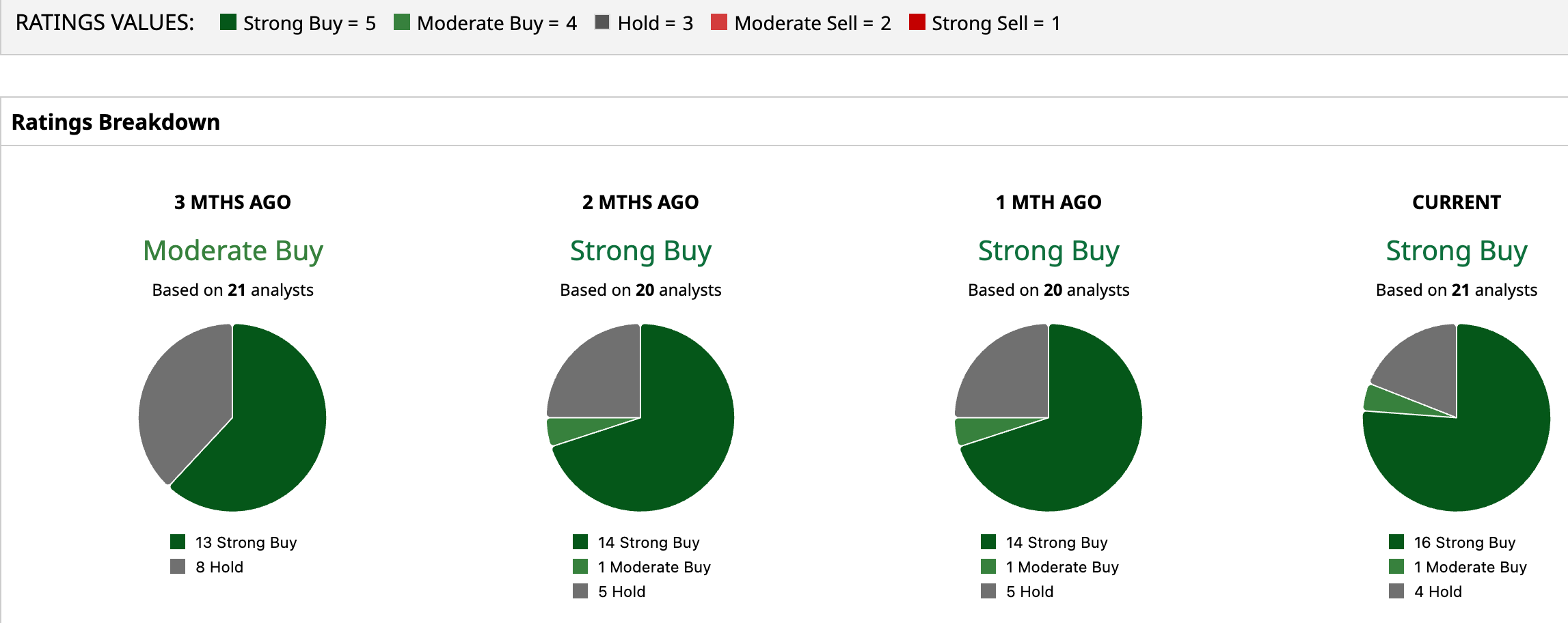

In addition, most analysts continue to recommend a “Strong Buy” on Sandisk stock ahead of the Q3 earnings report, which strengthens its bull case.

On the date of publication, Sneha Nahata did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)