/Dell%20Technologies%20by%20Gustianto%20via%20Shutterstock.jpg)

Dell (DELL) stock is up 66% so far this year and has just encountered an unlikely profit taker: its own Chief Financial Officer. David Kennedy sold 19,500 shares of the company at a weighted average price of $182.53 on April 9. This amounts to approximately 10% of his stake in the company. Even though the stock has gained another 12% since then, the sale has left everyone wondering if it's time to jump ship.

The news comes amid some controversy regarding a possible buyout. There were rumors in the market that Nvidia (NVDA), with its huge cash pile, was planning to take over an unknown company. Dell was touted as the likely candidate because acquiring it would allow Nvidia to own the entire stack from GPUs and CPUs to finished servers and PC hardware. Nvidia denied these rumors, but the stock has been climbing ever since.

Another thing investors need to know about the company is that the AI servers that are driving its growth don’t carry the same margins as its legacy business. While the incoming revenue may look attractive, it isn’t worth the same as the rest of the business when it trickles down to the bottom line. This isn’t a reason to sell the stock, though, so it would be safe to assume that the CFO’s sale was more for personal reasons rather than business issues. Any investor willing to buy the stock can therefore decide without worrying about insider selling.

About DELL Stock

Texas-based Dell Technologies operates as a developer, designer, manufacturer, seller, and marketer of a wide range of comprehensive and integrated solutions, services, and products. It operates in two main business areas: Infrastructure Solutions Group (ISG) and Client Solutions Group (CSG). The company serves governmental agencies, enterprises, educational institutions, small and medium-sized businesses, consumers, and healthcare organizations.

Dell Technologies has significantly outperformed the S&P 500 ($SPX) over the past year. The stock posted a strong upward trend, gaining around 154%, compared to the broader market’s gain of roughly 38% during the same period. This implies that the stock outperformed the S&P 500 by nearly four times. The outperformance has not been limited to the last year and continues into the current year. So far, the stock has surged more than 65%, while the broader market has risen by only 4%.

David Kennedy’s stock sale has come at a time when the company is expected to continue doing well. The firm’s fiscal 2027 revenue from the AI segment is expected to double, with EPS expected to grow by 25%. Going forward, the consensus EPS growth rates for fiscal 2028, 2029, and 2030 are 13.6%, 16.05%, and 19.19%. It's not like DELL stock is trading at a crazy valuation either. The forward P/E of 18.01x is below the S&P 500 average forward P/E of 20.82x and well below the IT sector’s 32.14x. At 1.07%, the dividend yield is indeed a far cry from the five-year average of 1.78%. But insiders don’t normally sell for that reason. Whichever way one looks at it, there is absolutely nothing wrong with the business, and someone entering the stock right now should not let the CFO’s transaction cloud their judgment.

DELL Reports Solid Q4 Earnings

The company reported its fourth-quarter FY 2026 earnings on Feb. 26. For the quarter, revenue came in at $33.4 billion. Performance was driven by the Infrastructure Solutions segment, which delivered revenue of $19.6 billion, representing a 73% increase. The segment recorded $9 billion in AI revenue, $34.1 billion in AI orders, and $9.5 billion in AI server shipments. Moreover, the segment ended the quarter with a backlog of $43 billion. Client Solutions Group generated $13.5 billion in revenue, reflecting 14% growth. Within this, commercial revenue increased 16% to $11.6 billion, while consumer revenue remained unchanged at $1.9 billion.

Based on the guidance, AI revenue for fiscal 2027 is expected to reach $50 billion, reflecting around 100% year-over-year (YoY) growth. Dell Technologies projects full-year revenue between $138 billion and $142 billion, implying 23% growth at the midpoint of $140 billion. For the first quarter, the company expects revenue in the range of $34.7 billion to $35.7 billion, indicating 51% growth at the midpoint of $35.2 billion. ISG is forecasted to grow more than 100%, supported by approximately $13 billion in AI server revenue.

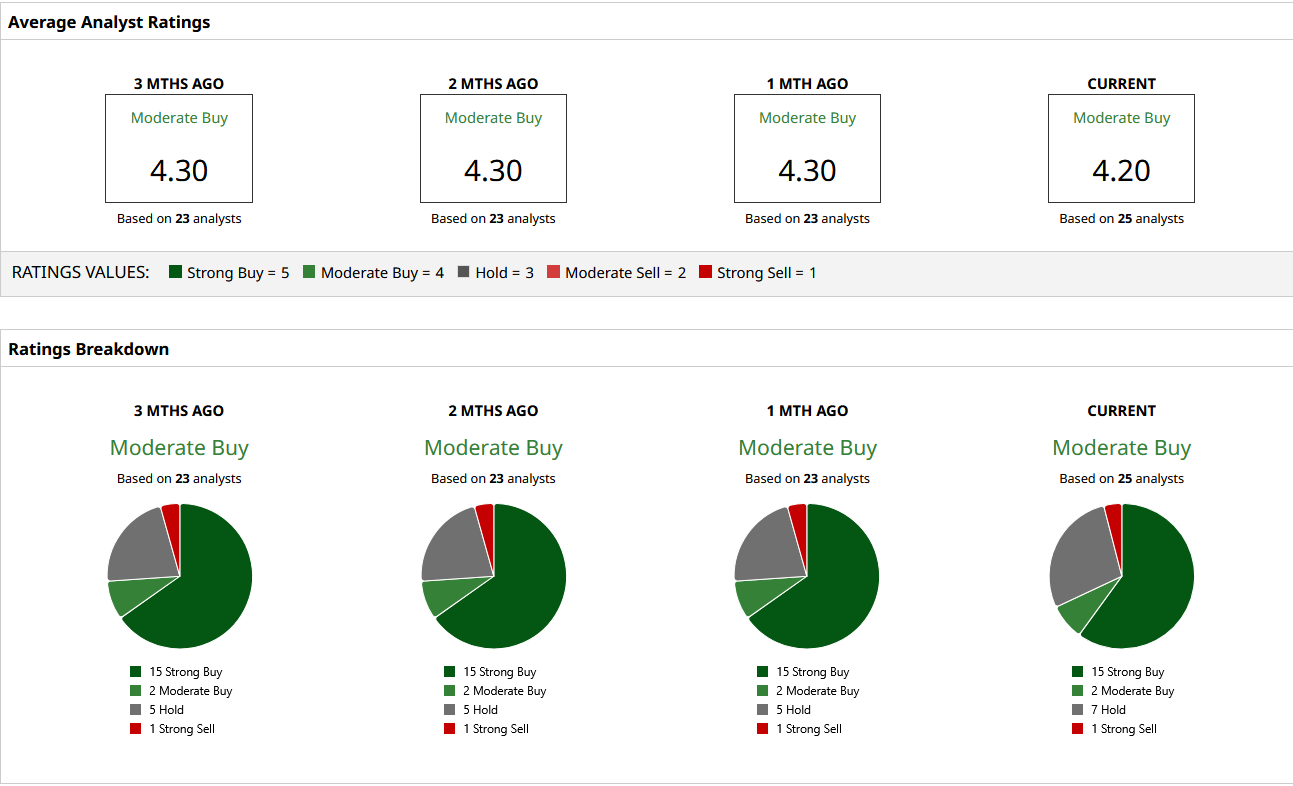

What Analysts Are Saying About DELL Stock

On April 16, JP Morgan analyst Samik Chatterjee increased the firm’s price target on the stock from $165 to $205 while keeping an “Overweight” rating. A day earlier, Goldman Sachs also raised its price target on DELL from $195 to $215 and kept a “Buy” rating. Bullish analyst sentiment further reinforces the company’s growth outlook.

DELL stock carries a consensus “Moderate Buy” rating from 25 Wall Street analysts covering it. Based on their estimates, the mean price target stands at $178, a level that has already been achieved. This reflects sustained investor demand, even during periods of macro uncertainty and the Iran conflict. The highest price target suggests upside potential to around $220, implying roughly 6% upside from current levels.

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)