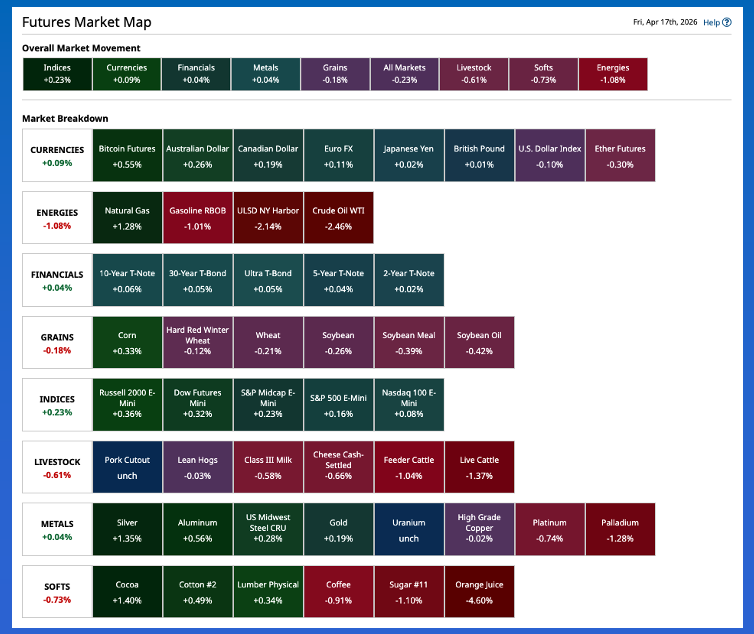

- A look at the Barchart Futures Market Heat Map early Friday morning told us what we've grown accustomed to seeing, the US president said something to lift US stock indexes heading into weekend again.

- Of course, this tends to be followed by contradictory statements as the weekend unfolds, keeping the seemingly endless cycle churning.

- The Energies sector was under pressure, as expected, through Friday's early morning hours.

Friday morning is a clear example of how the news/headline cycle has become predictably repetitive. Do this exercise with me: Look at Friday morning’s Barchart Futures Market Heat Map and the first thing that jumps out at us is the Indices sector (US stock index futures) led the commodity complex higher while Energies were under the most pressure. Considering it is Friday, and the US president tends to say something to rally US stock indexes heading into the weekend (before saying something contradictory during the weekend) we know the headlines will be about the end of his War on Iran, peace talks, or something along those lines[i]. Next, we pull up a financial news website (I used CNBC.com), and find, “Oil falls as (the US president) reiterates Iran War ‘should’ end soon and Israel-Lebanon truce lifts hopes” and “Stock futures tick higher after (the US president) says Iran war ‘should be ending pretty soon’”. As I said, predictably repetitive.

Corn: With most of the overnight attention on the other two Kings of Commodities, Gold (GCM26) up as much as $18.90 (0.4%) and WTI Crude Oil (CLK26) down as much as $4.43 )4.0%), the third member of the royal group, King Corn, didn’t do much. The more heavily traded July issue (ZCN26) posted a 3.5-cent trading range, from down 1.25 cents to up 2.25 cents, on trade volume of 17,000 contracts and was sitting 0.75 cent higher pre-dawn. The most logical explanation (what a dumb thing to say on my part) for the overnight rally, for lack of a better term, is the market closed lower Thursday. Recall July finished 2.75 cents in the red , followed by the National Corn Index coming in 2.5 cents lower for the day meaning national average basis firmed by 0.25 cent. The latest calculation was roughly 45.75 cents under July futures as compared to last Friday’s final figure of 48.0 cents under and the previous 10-year low weekly close for the first week of May at 44.25 cents under July. In other words, at this time when we are losing futures spreads as a fundamental read, national average basis remains weak. New-crop December was up 0.5 cent after rallying as much as 1.5 cents overnight.

Soybeans: Returning to our analysis exercise, given crude oil dropped 4.0% overnight, what do you think happened to diesel fuel? That’s right it fell as well, the spot-month contract losing as much as 17.7 (4.6%) through Friday’s early morning hours and was near its session low at this writing. Without looking at the quote screen, we have a good idea the oilseed sub-sector would be under pressure due to spillover selling from diesel into soybean oil into soybeans. Pulling up the quotes and we see July bean oil (ZLN26) down 0.3 cent (0.5%) while July soybeans (ZSN26) were off 4.0 cents (0.3%). Trade volume was light in both, 8,600 contracts and 11,300 contracts respectively, meaning Watson could be triggered by one of two things before the end of the day: The next round of headlines or reality. A look back at Thursday’s session and July soybeans finished 2.75 cents lower with the National Soybean Index coming in Thursday night 2.75 cents lower for the day meaning national average basis held at 82.25 cents under July futures. Last Friday’s final figure was 83.75 cents under with the previous 10-year low weekly close the first week of May at 73.0 cents under July.

Wheat: And then there’s the wheat sub-sector. After the explosive rally posted by winter markets this week, particularly HRW, it wasn’t overly surprising to see both markets take a bit of a breather overnight through early Friday morning. I’ll say this up front, I’m not reading anything into the red numbers as of this writing. Let’s see how Friday plays out. As for the markets, July HRW (KEN26) was down 1.0 cent after posting a 9.25-cent trading range, from up 4.75 to down 4.5 cents on trade volume of only 5,000 contracts. Over in SRW we see July (ZWN26) also down 1.0 cent after slipping as much as 2.75 cents on trade volume of 7,200 contracts. If I want to pretend weather still plays a role in these historically weather-driven markets, the latest 6-to-10-day forecast for April 22 through 26 continues to call for above normal temperatures and precipitation across the US Plains, Midwest, and Southeast growing areas. As I mentioned yesterday, though, folks in the Southern Plains are having their doubts about these official forecasts and drought reports (e.g. US Drought Monitor). Still, winter wheat spreads continue to cover neutral (HRW) to bearish (SRW) levels of calculated full commercial carry heading into Friday’s session.

[i] I’m not the only one to pick up on this pattern. You can watch a Stocktwits interview on the subject here: (LINK). Also, I will be doing an interview with Michele Steele on Stocktwits next week based on my recent conversation with Barchart's Elizabeth Volk.

On the date of publication, Darin Newsom did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/Abbvie%20Inc%20HQ%20photo-by%20vzphotos%20via%20iStock.jpg)

/A%20close-up%20shot%20of%20a%20Broadcom%20chip%20by%20g0d4ather%20via%20Adobe%20Stock.jpeg)