/A%20Lucid%20Motors%20vehicle%20parked%20in%20front%20of%20a%20showroom_%20Image%20by%20Michael%20Berlfein%20via%20Shutterstock_.jpg)

That the U.S. electric vehicle (EV) industry is going through a tumultuous period is no secret. Several EV upstarts have gone out of business, and some others might follow suit. Legacy automakers’ EV operations are also struggling, and the Detroit Big 3—who once had ambitious plans for vehicle electrification—have written down their EV assets by over $50 billion over the last few months.

Among startup EV companies, Lucid Group (LCID) has been hitting record lows frequently, reaching its most recent all-time low of $8.11 today, April 15. The stock has fallen in every year since its 2021 listing, and 2026 looks no different, with a drawdown of over 22%.

In my previous article, I had noted that it was perhaps a bit late to sell LCID stock. However, the stock has fallen from those levels also, in part due to the selloff amid the Iran war. However, while the broader markets have recouped their losses amid optimism over the ceasefire, LCID continues to languish. Is it time to give up on LCID, or can the stock rebound? Let's explore.

Lucid Motors Is the Leader in the Luxury EV Sedan Market

While many EV startups have gone bankrupt, two things have helped Lucid stay afloat. The first is that it offers quality products, and its Air sedan was the best-selling luxury EV sedan in the U.S. in 2025. Additionally, the model was in the third position overall after accounting for internal combustion engine (ICE) cars. As a side note, Air should be able to capture more market share in the luxury EV sedan market as Tesla (TSLA) has ended the production of its Model S sedan. Lucid’s Gravity SUV might also see traction, as Tesla has ended production of its luxury Model X SUV as well. Moreover, many of those already driving a Model X/S might consider a Lucid model next since Tesla has exited the luxury EV market—at least for now.

In what was a testimony to Lucid’s prowess, Aston Martin (ARGGY) partnered with the company to buy electric motors and batteries. However, Aston Martin has delayed its EV program amid weak consumer demand and its focus on plug-in hybrids (PHEVs). Meanwhile, Uber (UBER) has doubled down on its partnership with Lucid and will now buy at least 35,000 of its vehicles for its robotaxi fleet, versus the previous commitment of at least 20,000.

The second and perhaps more important aspect for Lucid has been the backing from Saudi Arabia’s Public Investment Fund (PIF). The cash-rich fund has been nothing short of a lifesaver for Lucid, and earlier this week, its affiliate company Ayar Third Investment committed to investing another $550 million into the cash-guzzling EV startup.

Apart from investing directly into Lucid by participating in every stock sale since the 2021 listing. It has also opened a delayed draw term loan credit facility for Lucid and raised its size by $750 million to $2 billion in Q3 2025. Last year, the PIF virtually provided a backstop in Lucid’s convertible bond sale by entering into a privately negotiated prepaid forward transaction.

Uber also increased its investment in Lucid Motors by $200 million and would invest a total of $500 million. Incidentally, Uber has also partnered with Rivian (RIVN), but unlike the Lucid deal, where Nuro will provide autonomous technology in the three-way partnership, Rivian’s cars will be powered by its own autonomous technology.

The cash infusion by PIF and Uber, coupled with a $300 million common stock issuance, would help Lucid raise the much-needed cash as it prepares to launch its midsize platform. However, that platform might not be a magic wand, as the competition in that space might only intensify with several companies looking to launch affordable models. This includes the R2 platform from Rivian and the sub-$30,000 vehicle that Ford (F) is building.

Meanwhile, Lucid is optimistic about competing in the midsize market, and at its Investor Day last month, the company said that the bill of materials (BOM) of its upcoming Lucid Cosmos will be only slightly higher than that of the U.S. EV leader—a reference to the Tesla Model Y—with a weighted average of U.S. and China production. However, Cosmos would have a higher range than what the Model Y is currently offering.

Lucid is also expanding overseas, particularly in Europe, where EV adoption rates are much higher than in the U.S. Also, given Tesla’s sales woes in the region, where many buyers have boycotted the U.S. EV giant over Musk’s politics, Lucid should be able to gain some ground with its formidable portfolio.

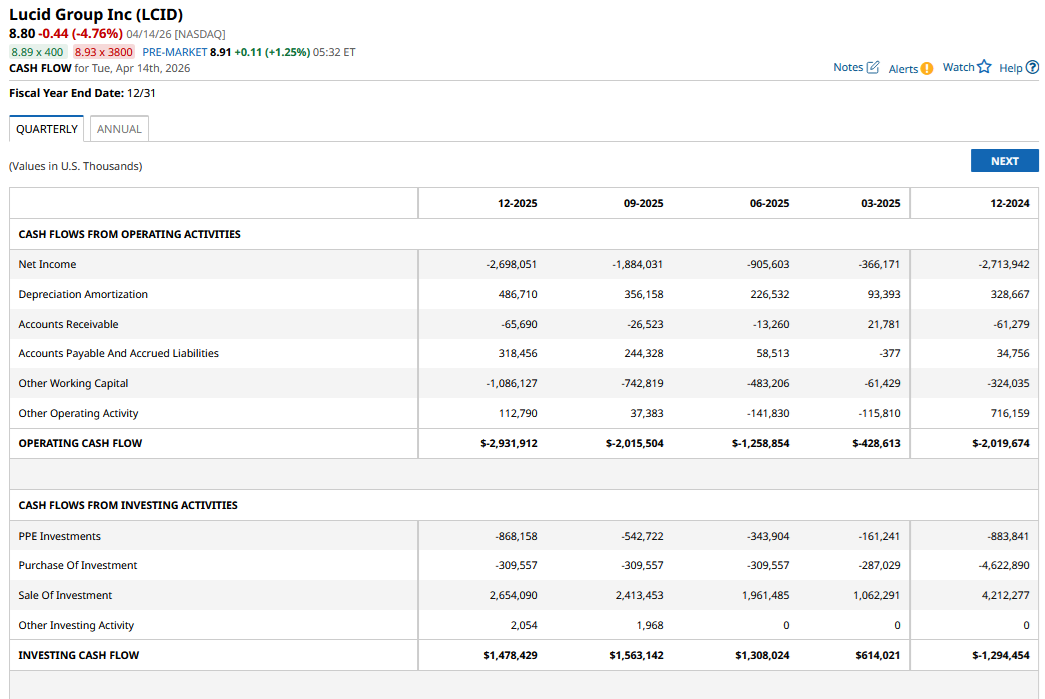

Lucid's Cash Burn Should Come Down

Lucid is also working on autonomous driving and plans to charge buyers between $69 and $199 per month, depending on the level of autonomy. Its capex needs would also come down, and it expects capex as a percentage of revenues to fall to low double digits in 2027 and further to teens in 2028. The company would already have spent much of the growth capex by this year, and it would be more of a maintenance capex going forward.

Over the long term, the company expects to keep its capex below 5% of revenues. The company is targeting to turn free cash flow positive by the end of this decade. However, that guidance, along with many other projections the company has made, would depend on the reception its midsize platform receives.

All said, with a market cap of just about $2 billion and a forward price-to-sales multiple of 1.27x, I believe LCID stock is worth the risk even though it remains a speculative investment.

On the date of publication, Mohit Oberoi had a position in: LCID, TSLA, RIVN, F. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)