/A%20close-up%20shot%20of%20the%20Taiwan%20Semi%20logo%20on%20a%20corporate%20building%20by%20Jack%20Hong%20via%20Shutterstock.jpg)

Taiwan Semiconductor (TSM) is not operating in a quiet market right now. The semiconductor sector has been running hot, helped by strong AI demand and tight chip supply. Nvidia (NVDA) and Advanced Micro Devices (AMD) have already posted big gains, and TSM has been part of that move, too.

The company's latest numbers show why investors are paying attention. Fourth-quarter revenue rose 20% year-over-year (YOY), and TSM's preliminary Q1 revenue came in at about $35.7 billion, up 35% YOY. Following preliminary results, GF Securities reiterated a “Buy” rating on TSM stock and lifted its price target ahead of the upcoming April 16 earnings report.

This move signals strong confidence in Taiwan Semiconductor’s ability to sustain its growth momentum, with analysts expecting AI-driven demand and solid margins to support another strong earnings report.

TSM Still Matters in the AI Boom

On one hand, TSM is simply a chipmaker. On the other hand, it is the world’s largest pure-play foundry, and that gives it a special place in the AI supply chain. The company does not design chips itself. Instead, it manufactures advanced processors for companies like Apple (AAPL), Nvidia, AMD, and Qualcomm (QCOM).

That matters because AI needs a lot of high-end silicon. Data centers, smartphones, and AI servers all depend on Taiwan Semiconductor’s factories. The company’s leadership in advanced nodes, including 2-nanometer chips, gives it a strong position and helps support high margins over time.

Nvidia CEO Jensen Huang praised TSM last year, saying that the company is doing a very good job supporting demand for Blackwell AI GPUs. Moreover, TSM’s Arizona fab recently produced the first Nvidia Blackwell wafer on U.S. soil, marking a major milestone for U.S. chip manufacturing.

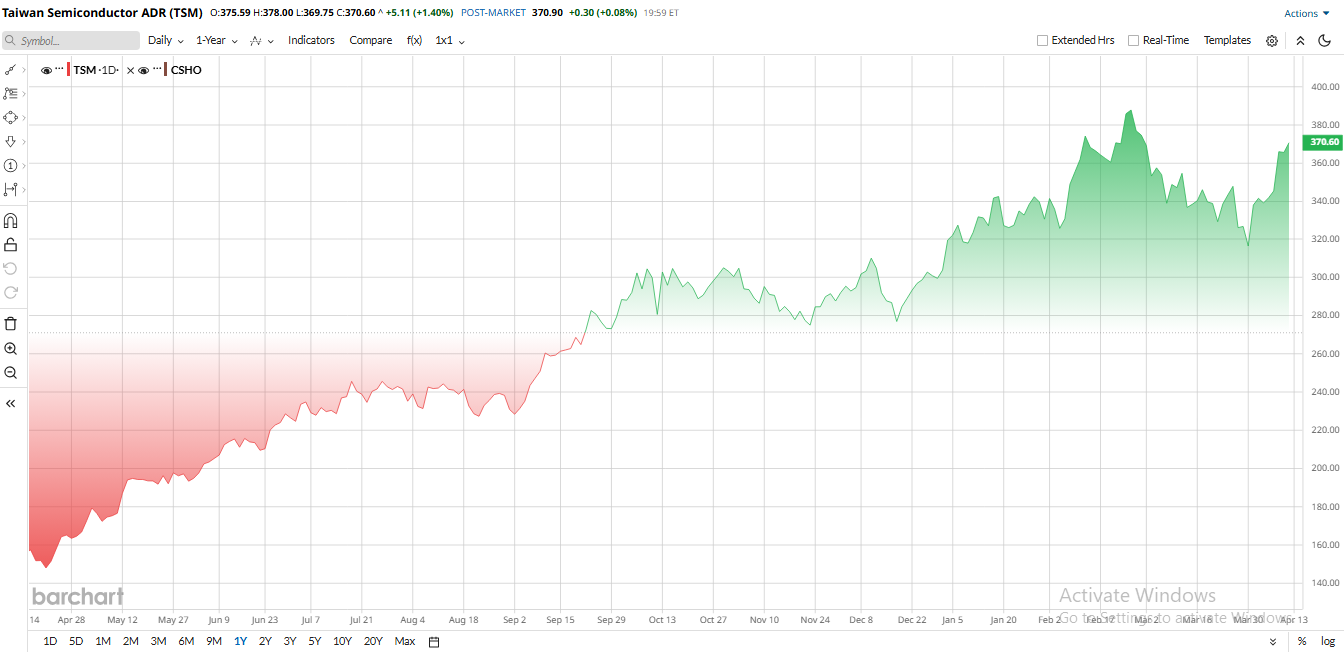

TSM stock has already had a solid run so far in 2026. Shares are up roughly 25% year-to-date (YTD), and up about 143% over the past 52 weeks. The stock has benefited from strong AI chip demand and record sales guidance. While it did pull back a bit from late-February highs, the bigger picture still looks strong.

Even after that run, TSM is not cheap. The stock trades at 34.8 times trailing earnings and around 15.6 times sales. That price-to-earnings (P/E) ratio is below the sector median for semiconductor peers, which sits closer to 46 times. While the market is not treating TSM like a bargain-basement stock, it is also not pricing it like an extreme growth story. For a company with this kind of scale and chip leadership, many investors still see the valuation as reasonable.

Taiwan Semiconductor’s Business Is Still Growing Fast

The latest results show that Taiwan Semiconductor's business is in strong shape. In Q4 2025, revenue reached $33.73 billion, up 20% YOY and coming in above expectations. Net profit rose 35% YOY. In Q3, profit also beat forecasts, climbing about 39% YOY. TSM has a habit of clearing the bar, and the market knows it.

For Q1 2026, analysts expect revenue of about $35.7 billion and EPS of about $3.31. That would mark earnings growth of about 56% YOY. These estimates line up with TSM's own preliminary report, which showed revenue near the high end of management’s guidance.

Margins will be the big focus. Management guided for Q1 gross margin of around 64% at the midpoint, and analysts think the final number could be a bit higher. Strong AI demand, better utilization, and pricing power should help.

The company’s full-year outlook also remains upbeat, with CFO Wendell Huang earlier forecasting about 30% revenue growth in 2026.

Why GF Securities Likes TSM Now

GF Securities turned more bullish ahead of the earnings report as it believes TSM is set up for another beat. The firm raised its price target to NT$2,808 from NT$2,325 and kept a “Buy” rating.

The main reason is AI demand. GF Securities expects TSM to beat its own guidance on both sales and margins. The firm sees Q1 gross margin near 67%, above the company’s 63% to 65% range. Analysts also believe higher utilization at 2nm and 3nm fabs will help earnings.

GF Securities sees sales growth continuing into Q2, with about 6% quarter-over-quarter growth, before a possible slowdown later in the year. Even then, the long-term setup still looks strong because TSM plans to spend heavily on capex in 2026, with spending expected in the $52 billion to $56 billion range. That shows the company is still investing in leadership, not just harvesting current demand.

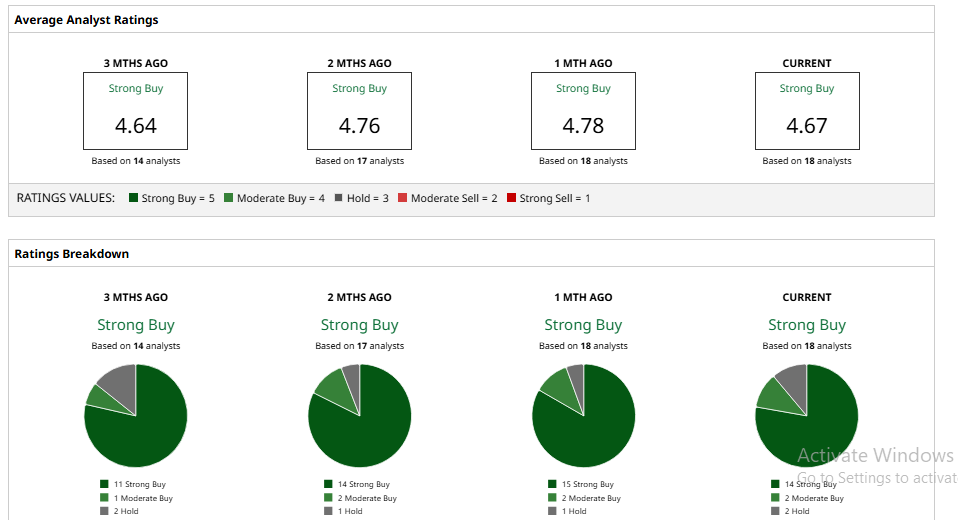

What Do Analysts Think of TSM Stock?

Wall Street is broadly bullish on TSM stock. Out of 18 analysts covering the stock, 14 have a “Strong Buy” rating, two have a “Moderate Buy” rating, and two have a “Hold” rating. The consensus is a “Strong Buy” rating, while the average price target is $421.69, implying potential upside of about 11% from current levels.

GF Securities is not alone. Citigroup also recently raised its target to NT$2,800, citing strong AI chip demand and expecting 2nm to become a huge revenue driver. Morgan Stanley lifted its target as well and kept an “Overweight” rating, saying investors should increase positions as AI demand keeps pushing revenue higher.

Overall, analysts see TSM as one of the clearest beneficiaries of the AI boom. The business is growing, the margins are strong, and the technology lead still looks real. That's why GF Securities thinks now is a good time to buy.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.