/Berkshire%20Hathaway%20Inc_%20%20logo%20and%20money%20background-%20by%20photo_gonzo%20via%20Shutterstock.jpg)

Omaha, Nebraska-based Berkshire Hathaway Inc. (BRK.B) offers insurance, freight rail transportation, and utility services. Valued at a market cap of $1 trillion, the company is scheduled to announce its fiscal Q1 earnings for 2026 in the near future.

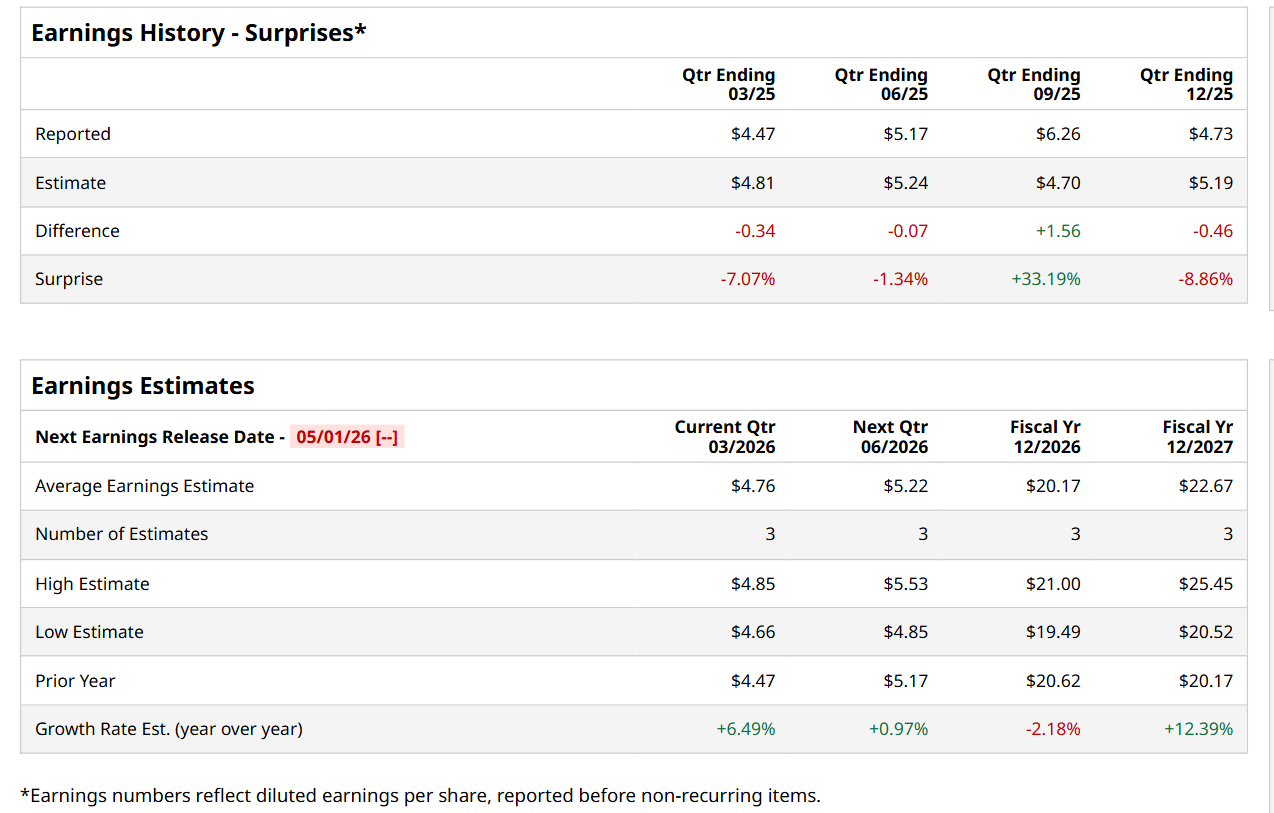

Ahead of this event, analysts expect this insurance company to report a profit of $4.76 per share, up 6.5% from $4.47 per share in the year-ago quarter. The company has missed Wall Street’s bottom-line estimates in three of the last four quarters, while surpassing on another occasion. In Q4 2025, BRK.B’s EPS of $4.73 missed the consensus expectations by 8.9%.

For the current fiscal year, ending in December, analysts expect BRK.B to report a profit of $20.17 per share, down 2.2% from $20.62 per share in fiscal 2025. Nonetheless, its EPS is expected to grow 12.4% year-over-year to $22.67 in fiscal 2027.

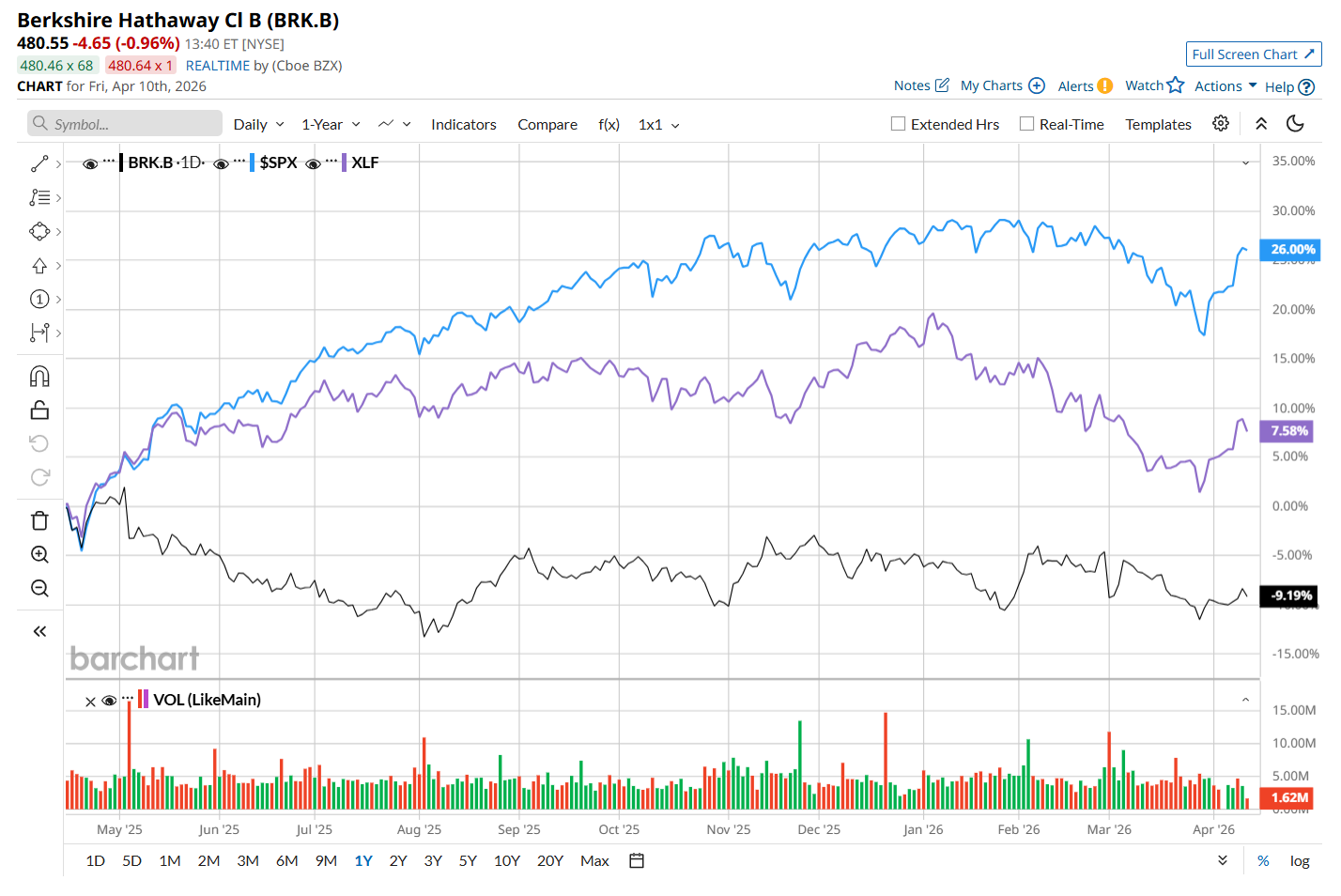

BRK.B has declined 6.7% over the past 52 weeks, trailing both the S&P 500 Index's ($SPX) 25.1% return and the State Street Financial Select Sector SPDR ETF’s (XLF) 10.4% uptick over the same time period.

BRK.B shares have been under pressure primarily due to investor concerns over the leadership transition from Warren Buffett to Greg Abel, which has eroded the so-called “Buffett premium” that historically supported a higher valuation. Additionally, GEICO has faced rising bodily injury claims and higher customer acquisition costs, intensifying concerns about potential margin pressure.

Wall Street analysts are moderately optimistic about BRK.B’s stock, with a "Moderate Buy" rating overall. Among six analysts covering the stock, two recommend "Strong Buy," and four suggest "Hold." The mean price target for BRK.B is $523.50, indicating an 8.9% potential upside from the current levels.

On the date of publication, Neharika Jain did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20concept%20image%20showing%20a%20lightbulb%20with%20planet%20earth%20in%20a%20mossy%20green%20background%20by%20Capt_Pic%20via%20Shutterstock.jpg)

/The%20CrowdStrike%20logo%20on%20an%20office%20building%20by%20bluestork%20via%20Shutterstock.jpg)

/An%20image%20of%20a%20Tesla%20humanoid%20robot%20in%20front%20of%20the%20company%20logo%20Around%20the%20World%20Photos%20via%20Shutterstock.jpg)